Next time when a terrorist activity hit any of our cities, I am definitely going to part blame the role of Indian bankers. The yesterday event (sting operation by cobrapost) will definitely catch the attention of these extremist organization and we all know these outfit are searching ways to route or invest unaccounted money in countries like US, Europe and India. I will not be surprised if they start lifting these so call experts in converting “black to white“ to provide them these “specialized” services !!! {check few slides at the end of this post & you may understand why this happen}

Read – Banks are mis-selling or Bankers are mis-selling

Are banks responsible?

After the story broke out, the three banks involved released statements of internal probe and audit and the sentence common in all the three statements issued by banks, was that the bank will continue to work under the regulations and process as laid by the regulator. But does the regulator tell Banks to get involved in converting black money to white?

Well it was not a single bank? Three top private banks are involved. It is not that bankers from Delhi or metro are speaking this language. We hear the same story of “opening the multiple account, deposit cash, we make the DD and invest in Insurance for more than 7 years story”.

Do the bank need more accounts or is it running behind the DD issuance commission? No my friend… the banker is behind only one thing “SELL INSURANCE”. It is not a hidden fact that out of all third party products the bank sells, insurance gets them the highest commission.

And we all know this is JFM (Jan-Feb-March). The closing time for most of the banks and insurance companies. Any big ticket in quarter four means- a handsome commission, a good performance reviews and may be a trip or gift from the insurance company.

So unfortunately it is the BANK who is not mis-selling…. But the BANKER who is mis-selling. But on the next thought the banker is a representative of bank, so bank also has to make an environment so that the employee is unbiased and loyal towards his job and does not spoil the name of the institution. You can check cobrapost shocking videos here.

Must read –Bank locker the games bankers play

The insurance focus of Banks

I have worked with bankers all my life and still have lot of friends in this circle and based on what I see, the banks have a hidden work culture which is promoted by the banks internally to garner insurance revenues. This culture can be visible if you attend the morning briefing of branches. The front desks person who has sold most number of policies is honored and “hip hip hurrayad”. The targets for the day are rolled out. Sometime “Login Day” is announced and people are pushed to get sign ups. The personal bankers are motivated to visit customer’s home after cash hours with the same agenda of getting insurance sales.

They are also made to talk in pleading language like “sir meri naukri chali jayegi” or “uncle appki bachhi hun, please dhyan rakhiyega”. The banks allow or sometime give additional desk to the person of the insurance company in the branches, the sole job of this person is to increase insurance sale by pressure. And all this happens in the name of the “tie up” or “partnership.” I cannot give you a sting, but culture has gone so low that the bankers also decide, will a call from a male employee is sufficient to get an insurance policy or does he requires a plead in a female voice. The bankers who give more revenue from insurance are blue eyed and their career is considered to be relatively safe. If you cannot sell insurance in a private bank, the bank HR makes you leave the organization very soon.

Read – Confession of ex-banker

Do all banks do it? Yes mostly all private banks and now a few public sector banks have also started doing this.

So when they say “we will carry out audit to see if the rules have been violated”… we all know no rules have been violated as there are NO RULES when it comes to insurance sale. The scapegoats will be penalized and bank will continue to promote the same internal culture (sic).

WHY this happen?

In December 2012 I attended Financial Planning conference & got a chance to hear experts from Canada, Australia & Malyasia. I attended one day pre-confrence workshop “Global Best Practice for Financial Planners” by Shawn Brayman from Canada – he is a well know name in Financial Planning profession due to his research & FP software company ‘PlanPlus’. He shared couple of shocking things during the day – sharing couple of presentation slides which will open your eyes.

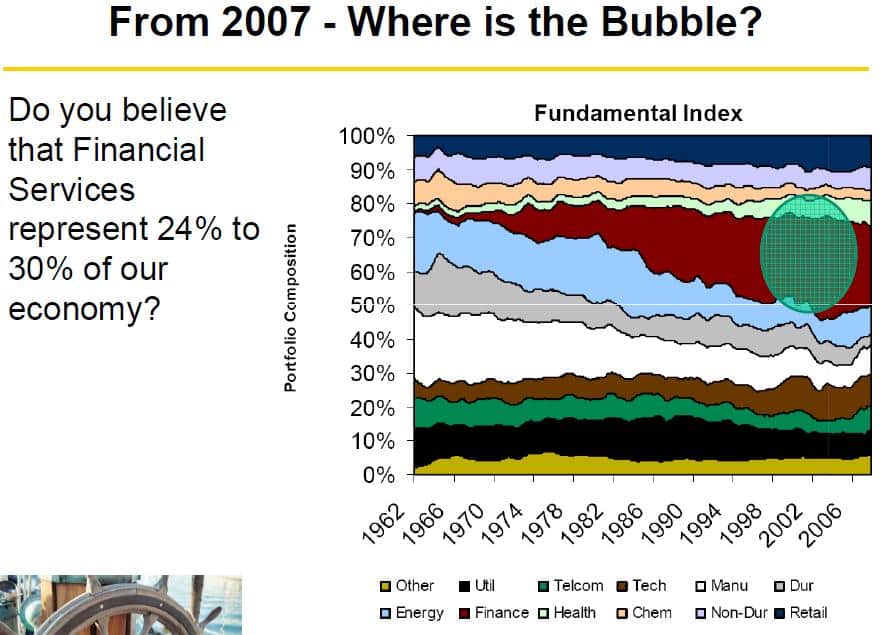

Where is the Bubble? (US)

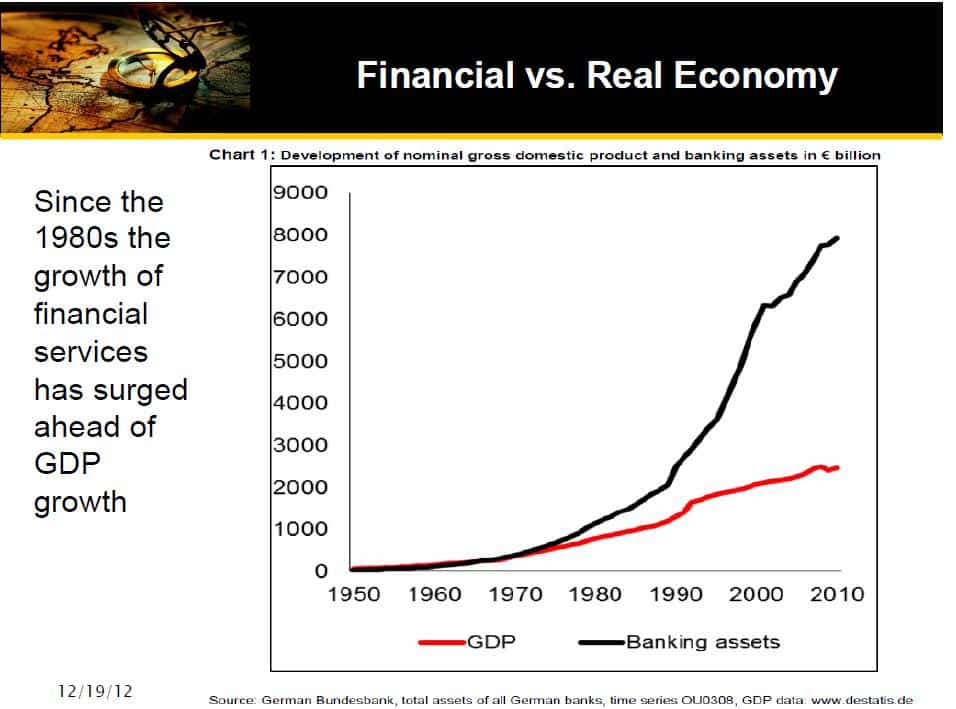

Financial Vs Real Economy (US)

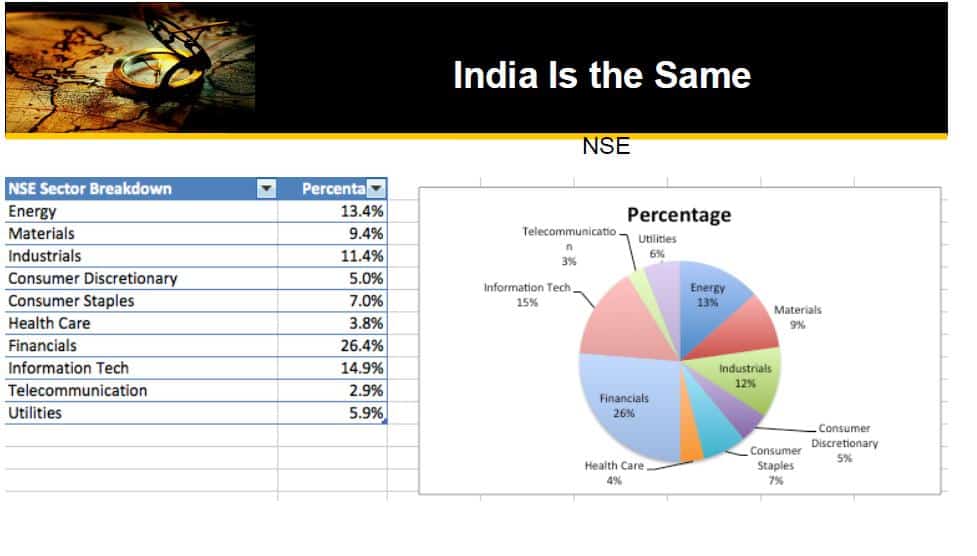

India is the same

Incentives determine advisors behavior (Shawn in Red Tie)

How is that possible

Do share your thoughts and your interactions with banker friends if you have. Also share if you have been a victim of banks demand for insurance. Let’s open few more cases to the world.

Hi Hemant,

Very interesting article. Well I actually dont have an experience of insurance but couple of years back, one of the branch manger of a Nationalised bank offered me an SIP in Tata Mutual fund. Those days I did not have enough knowledge on mutual funds so did not proceed further with that.. 🙂

Hi Manoj,

So you were lucky that they suggested SIP – lot of PSU Banks sold New Fund Offers in 2006-07 as Fixed Deposits 🙁

Very good article. Banks are presuurizing their epmloyees for unetical & illegal practices. Insurance product must be delinked with banks.

Hi Pawan,

In this budged they hinted that now banks can become insurance brokers – so they can sell polices from more than one insurance company – more confusion & problems for clients.

Bank pressure their emp to sell insurance.. If you cannot do that they will throw us.

Hemant!

Hearty congratulations for bring very hotly discussed topic yesterday in all news channels.I am sharing your link to few of my Bankers friends.

Thanks Prakash.

Hello Hemant,

Really nice and eye-opening article this is..

I want to share opinion on “banker-miss selling”

I have worked with private bank earlier for 1 Year.. I actually know what pressure employee has to handle within “JFM” and otherwise also.. Now a days banks are more for selling and very less for core banking services.. many banking products selling and “cross-selling” and irresistible”login-days” are involved other than core operation and services.. and on the top of all that they call it “Financial Planning”. while selling the insurance or MF-SIP product many times under pressured employee miss-sale it. they make customer believe non-existing “benefits” of the product..

I really recommend, banker should think twice before selling the product as it leads to affect credibility of bank. at the end credibility matters the most when it comes to finance..

Hi Gargee,

Thanks for sharing your story… but I don’t know why still people have this faith on bankers. Every week we read mis-selling stories by bankers but no action by regulators. Buyer Beware.

when I was insurance our Sm usually say koi co. kharab nhi hoti hain agent or employee co. ko kharab krte h..but fact we all know If he won’t sell the product co. kick back to his employee…

when we talk continue education program..

pharma co. is sponsor and dr. is participatory …. Do you really think they give enlightenment or education to dr.

they give only sales penetration,high commision,incentive…

Let come to the FPSB india. I respect to FPSB org.who have given new definitions to people think about planning rather then investing.

there r 10 to 12 member of FPSB Board ..

There r only one member Honorable suresh sadgopan is financial planner..

other are CEO, MD of Mf house , insurance industry, share broker.

do you thing they will encourage Financial planning profession?

I think H’le sadique and few good planner are spreading financial literacy and financial planning awareness in India.

FPSB Have very little bit effort compare to Mr. saddique and gd planner like u.

Our continue education program is conducted by MF ,insurance,share market,banking industry.

does it really worth?

It was relay Eye opener.

we blame to person but fact is institution indulge in malpractice.

Hi Sadashiv,

We should not expect much from institutions – its on individuals to prove themselves to clients.

Salesman will work one shade above or one shade below regulation bar.

Association & Designation will raise the bar a bit but we as professional should build our own standards, our own ‘best practices’.

Hi Hemant,

Very nice one. Yesterday, I happened to talk to a banker about surrendering the ULIP policies. He was at first trying to pursuade me that those policies are very good and need to give more time for the money to grow. Later, he said, he was short of the target of the year and it would impact his promotion and he pleaded me to provide some reference.

Hi Gayathiri,

This clearly shows the kind of pressure these people are having.

Hi Hemant,

You have very rightly shown the picture. I have been through this several times.

The main focus of these guys is majorly on sales of insurance or on the credit cards.

I have worked with ICICI Prudential for 2 years as an advisor, rightly to say insurance agent.

Usually sales are done considering the commissions agent is going to get. Target completion is the goal of most of the agents. I left it in 2 years because it was not possible to be a success with all those ethics I carried. Some of the agents even get the policy application form filled and signed forcefully, saying that your first commission will be paid by them as a gesture.

Customers become sort of greedy and take the policy.

Only bankers or agents are not to be blamed for this mis-selling, people just take the policy without even checking what they are buying. They usually forget that Insurance is a subject matter of solicitation and its a very important step in financial planning.

Thanks for this article. I’ll share it with all who are in a hurry to save tax and are buying policies just due to 1 reason… tax saving.

Hi Nishi,

Thanks for sharing your story.

“Insurance is a subject matter of solicitation”

The dictionary meaning of Solicitation is “To Ask For”. Hence insurance is a subject that needs to be asked for by the consumers. This implies that the customers have to discuss with an Insurance Advisor regarding suggestions and professional advice suggest the right insurance products and services specially tailored or customized to meet an individual’s requirements. Hence, in short, it must be understood that Insurance Products and Services should not be SOLD but Solicited by the Consumers…… 🙁

Hi Hemanth,

Very good article. The swiftness with which you came up with this article speaks how passionately you are against this mis-selling of insurance by bankers. Kudos to your efforts. We all get cold-calls for investments from different ‘Private Banks’. After researching few of the products they suggested, i realized all their so-called investment plans are nothing but ‘insurance’ in the end. And it isn’t even proper insurance like a term plan — it’s ULIP, Traditional Insurance, Money Back etc etc. Name’s different, but the product never gives guaranteed return more than 4%.

Hi Phani,

Even I keep getting calls from my bankers & I can see the tactics they are using – definitely they can impress any common man.

This is incidence should prove blessing in disguise because so called experts and regulators were busy touting the role of bankers as impartial advisors on financial planning to their customers. The fact was everyone was a party to earn free commission without any knowledge, service and care for the customer. IRDA, SEBI shoud awkae as early as possible to stop this menace and ban the banks from selling any third party products. There are plenty of reasons for the banks to concentrate on their core business. You ask customer of any bank and you will find he is dissatisfied for some or the other issue with some or the other bank. These banks should be put to task to improve upon these things. Improve their loan disbursing capabilities, recovery of loans, management of funds, curtailing of wasteful expenditure, 10000% improvement in customerservice and forget this easy money. There is no loss to the public and investors. There are many better alternatives available and even if it isnot available it is better not to have it but nobody should be cheated. People blindly believe in what the bank staff says. Public has undue faith in bank staff. They do not challenge them. Poor people, semi urban, rural, small income earners etc. can not even dare to complain and question the bank staff. I am totally against the concept of selling any third product by any bank. For the development of financial product market we should create a different system. We have been doing the same for every such thing like industrial finance, agricultural finance, housing finance, factoring services, merchant banking services, regional rural banks, mahila banks etc. Let there be an organisation selling all the financial products like an agent or the distributor.

Hi DB,

I think this is too much to expect from our armchair regulators – they are bringing Investment Advisor regulation but even that is not foolproof.

Dear Hemantji,

Thank you for the in depth article on Mis-Sellings by banks/bankers.

Banks are believed to be one of the trusted institution. These are the institutions where ones hard-earned money is kept supposing to be the safest place. Their advises and and suggestions are taken to be pure. But if they work unethically by mis-selling their products then there is no reason to take them as safe.

Hi Sk Ray,

Search for case of Suchitra Krishnamoorthy & one bank – you can see bankers are not leaving anyone.

thanks Hemant ji for this eye opener article,

I WANT TO SHARE MY EXPERIENCE WITH YOUR READERS. i regularly experiencing these type of calls from my bankers,and from so many agents of insurance houses with all new plans everytime and now itself.before 5 to 6 years i was also traped by them and invested lot of funds in all these products in which some are doing good (fortunately) and some are very bad and i have to do lot of paper works to get back my money.The agents and represntatives who approached me that time are no more working and they had got job in some other financial institutions.I think these are the common scenerio with all the investors.And when i had accumulated so many kgs. of papers (of mutual fund statements, policies)and found my self unable to deal with my portfolio which is not performing well,then i searched web to get some ideas how to manage my investments.And Finally one day i get one article from tflguide.com and thought that i got what i am serching for…..and that is MR. HEMANT.

now i surrenderd all my investment worries to him and got peace of mind about my investments and retirement.

So Friends,dont search lot of websites and get puzzled.Go for one good financial advisor and use your time to earn more funds …:)

Thanks Arun – you rightly said “The agents and represntatives who approached me that time are no more working and they had got job in some other financial institutions.”

Whenever someone is choosing an advisor – he should check his continuity plan, will he be there when you will need him most.

Hamantji,

Thanks for a nice article, and it was your article that has made me literate in financial matters, appreciate your selfless action, eye opener to many other like me.

Excellent Article. Thank you so much

Lets take any ICICI, HDFC, or AXIS bank branch in your neighbourhood. Usually, its located in the posh colonies/market place/prime location. Rent part of such branches is somewhere around 5 to 6 lakhs per month. Now there is a huge staff from Branch manager/relationship manager/cashier etc; and their monthly salaries again would add up to Rs 12 to 15 lakhs. Next part is electricity bill and other sundry expenses. That means a single branch is running at the cost of Rs 30-50 lakhs or so. So how will the branch generate enough revenue to meet these expenses??

Simplest method for them is to sell INSURANCE and earn commission..By doing core banking, they cannot sustain themselves to run even a single branch in metro cities. There is not enough incentive or funds to be generated by selling MFs/lockers/loans to sustain such high expenses to run a branch..

One single step can kill two birds with a stone..Stop banks from selling insurance immediately; and it will end Mis-selling to about 85% and improve customer satisfaction in core banking..

But is someone out there listening/reading this??

Mr. Dhawal completely agree your view….your comments remind me about co-operative society…My native place is situated Semi urban area….people saving ratio is huge.. Five year ago here were only 5 to 6 co operative society ..now only Sirohi city there are 35 co-operative society ..I haven,t count village co. operative. society…the only reason is in India there is no regulator who regulate property price and their rent rates. the huge fd collection goes into property portion and rest little bit amount by loan. they give 14% to 15% return to customer..MY

Nobody are aware of DIGC. They think RBI give to licence so our money is hundred % safe ….. Real estate unorganized sector is also responsible this mis selling and malpractice.

We can crack it if financial let racy would be compulsory education in english…like Europe country .. god knows when will it be?

As you said in your article ““we will carry out audit to see if the rules have been violated”… we all know no rules have been violated as there are NO RULES”, RBI has cleared the 3 banks involved.

Hi Hemant,

SBI launch below term Insurance.

SBI Life – Suraksha Plus (UIN 111N051V01)

Savings Bank Account Holders’ Scheme

Now i am think to bought it.

what you think? is this ok?

Here is as follows:

1. birla sun life via dcb bank: Sold a policy in which processing charges are 40% for five years premium. Bought somewhere in ~2009. The guy was in contact with us since 2005 when he worked at hdfc bank near us.

2. kotak : something similar. Bought in 2007 maturity is on 2017, paid up period is first three years. Garantee of return date of maturity is 103% of amount invested. Current value -15%.

3.icici prudential: Same shit.

4. hdfc: Same shit 40% processing charges for the first year premium.

5. bajaj allianz : Same shit.

6. tata and reliance insurance: Same @#$%^ Shit !!!

All the shit we bought thinking that the poor man will earn something but when we discovered it, it was like the poor man looted us. Some people want to earn money and some wants dignity, this is a choice that only we can make !!!!

Moral: The culture of this industry has become that they successfully take the money from you thinking that they have earned it. This is the kind of money with which they feed and raise their kids with, this shout goes not only to the agents but the top level bankers who has structured this system !!!

You better donate your money if you are not buying LIC’s insurance.

Very well presented article and describes the situation in real terms. The Banks have gone one step ahead and insist on Insurance in lieu of FDs whenever the customer is in need of a locker. If some one makes a study of the lockers allotted in the past 4 years you would find more than 50% of the lockers were allotted on the basis of Dud Insurance policies where the Bank/ or its associate has made a fabulous earning.

Hemant …….. Heartfully appreciate all your efforts. Last few weeks, I have gone through many of your posts on various topics.

I have circulated and strongly recommended to my group of friends also to go through these valuable and useful posts.

Regarding Insurance, I had one query — My parents has taken a policy “ING LIFE PLUS” in the year 2007 with out any knowledge considering the words of agent/insurance advisor to reach his target of sales.

Do you have any idea of this, whether is it a good policy to pay further or Since the grace period of 5 years is completed — Can we close the same and take some other policy.

Thanks

Amar

IN 2010 WHEN I WENT TO CITI BANK ATHENS BRANCH TO DEPOSIT ONLY 1000 EURO IN MY ACCOUNT(GREECE),THEY TOLD ME THAT YOU CAN DEPOSIT IN ANOTHER BETTER METHOD.BUT THEY DID NOT SAY ABOUT INSURANCE POLICY.THEY TOLD ME TO SIGN HERE AND THERE .I COULD NOT READ GREEK LANGUAGE I KEPT THE PAPERS SAFELY.FROM MY ACCOUNT THEY TAKE THEIR PREMIUM BUT I WAS WAITING FOR 3 YEARS TO TAKE BACK MY MONEY AS THEY TOLD.BUT AT LAST I UNDERSTOOD THAT I LOST 3000 EURO .I APPROACHED SO MANY ADVOCATES.THEY ASKED ME;DID YOU SIGN THE PAPERS?THEN WE CANNOT DO ANYTHING.I AM DESPERATED AND VERY SAD.HOW I HAVE BEEN CHEATED BY MY BANK EMPLOYEE.

Hi Civi,

Sorry to hear that – its a huge loss but bankers don’t care about clients. 🙁

Comments are closed.