Whether you are in the government sector or private sector, whether a professional or businessman there is one goal for which everyone saves money and that is “Retirement”.

With an increase in the medical facility and the constant increase in life expectancy, it has become more important to save for retirement. An average Indian spends 20 – 25 years of his life in retirement. Still, the majority of the population do not save enough for this major event.

Read:-5 Steps of Happy Retirement

In the government sector, guaranteed retirement benefits are already available for employees in the form of pension and other benefits which are inflation-adjusted, however for an employee in private sector or for a businessman, they have to plan their own retirement with different products available in the market such as Insurance pension plans, Public Provident Fund (PPF), Mutual Funds, etc.

Most of the times when people start thinking about retirement first question which comes into their mind are how much to save for retirement and second- which product to select? To calculate the required retirement corpus is very simple but to select the best out of available products is a very difficult process. Let us first show you how to calculate the required corpus for retirement.

Must Read- 8 Facts about Retirement Planning you may not have known

How much to save for retirement?

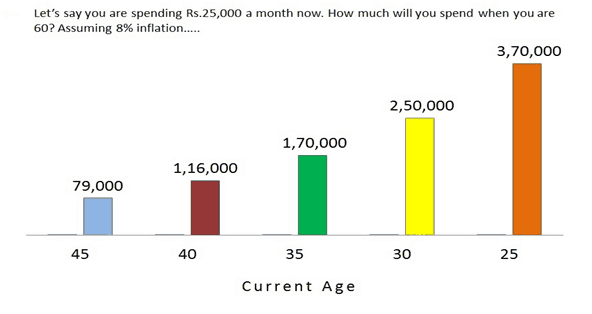

To calculate the value of retirement corpus few inputs are required which are different for every individual like current monthly expenses, age, retirement age, expected rate of return, etc. Suppose Mr. A is 30 years old and his monthly expenses are Rs.25,000, he wants to retire at the age of 60. So considering 8% inflation, his monthly expenses at the age of 60 would be Rs. 2,50,000.

Below image shows how much your expenses would be at the age of 60 as per your current age

Now if we expect Mr. A’s life expectancy to be around 80 years then he would require Rs.2.5Lakh every month for 20 years. With 2% of the Real rate of return, the total corpus required would be Rs.4.9 Cr. Normally the retirement calculators available online do not consider the real rate of return, so you might get a different answer. However, if calculating through excel then you can use a real rate of return.

Must Read:- Is 1 Crore is enough to Retire?

Comparison of Mutual funds, PPF and Insurance Pension Plans:-

| Equity Mutual Funds | Public Provident Fund | Insurance Pension Plan | |

| Liquidity | MF provides the option to redeem on demand, which is extremely beneficial especially during an emergency. | The first redemption is allowed at the end 7th year which is 50% of the balance at the end of 4th year. | One cannot withdraw money from pension plans. The only option is to either surrender the plan after 3 years or take a loan on surrender value. |

| Tax saving | Only Tax saving mutual funds are allowed for deduction under Sec 80C.

Redemption in equity mutual funds after 1 year is taxable @10% on gain excess of Rs.1 lakh. |

Investment in PPF account is allowed for deduction under Sec. 80C and redemption on maturity after 15 years is also tax-free.

However premature redemption would be taxable. |

Premium paid towards pension plans are allowed for deduction under Sec. 80C. On maturity only 1/3 of the accumulated amount is commuted which is tax-free and the rest of the amount is paid out in the form of an annuity and is taxable. |

| Lock-in | ELSS schemes of mutual funds have a lock-in period of 3 years and no withdrawal is allowed. Many other schemes have a different lock-in period, however, withdrawal is allowed with exit load. | There is an initial lock-in period of 15 years and thereafter every 5 years. However one can withdraw money from the end of 7th year. | Lock-in period = term of the policy. However, one can surrender the plan or take a loan on surrender value after 3 years. |

| Expected returns. | As equity mutual funds are market-linked hence no return is guaranteed, however over a long period one can expect a CAGR of 12-15% | Current interest rate is 7.90% | The bonus issued is generally around 4-5% in insurance policies which is in the form of simple interest. |

| Maximum Investment | No limit | Limit of Rs.1.5 lakh per year. | No limit |

| Safety | Since the money is invested in the equity market, the returns are not guaranteed. However, the schemes are approved by SEBI and are monitored under strict guidelines. | Since the scheme is backed by the government, safety is not an issue. | The equity exposure in pension plans is nil. Also, insurance schemes are approved under the guidelines of IRDA. |

| Mode of investment. | Through Cheque, DD, NEFT, and RTGS. | Cash, Cheque, NEFT. | Cash, cheque, NEFT, Credit Card. |

Check:- Best Retirement plan in India

Why choose Mutual Funds over PPF and Insurance Pension Plans: –

In the above example of Mr. A, total retirement corpus required is Rs. 4.9 Cr. Suppose he chose to save this amount through PPF then required saving per month would be Rs. 30,000 approx. For an insurance policy, he would be required to pay a premium of Rs. 60,000 per month. And for the same corpus if he chose Mutual Funds then he would be required to save Rs. 13,000 approx. The reason why mutual funds require less saving is due to its equity exposure. It can beat inflation and can generate a higher rate of return in the long period of 30 years.

Must read – Retirement expectations vs reality

Conclusion

While considering retirement planning one should select a product which invests into equity, suits his risk profile, beats inflation and gives better tax-adjusted returns. Mutual funds are best as they fulfill the required criteria and offer much-required liquidity option with minimum cost.

Also, mutual funds are successful in creating long term wealth and offers better flexibility than PPF and Insurance Policies. Please remember, overexposure into one asset class can harm your portfolio in the long run. So, one should always invest with the proper asset allocation and review the strategies regularly to get maximum benefits.

So what are you doing about your retirement? Please share in the comment section.

")

Thanks for giving advice and sharing your experience with us.

Comments are closed.