The announcements on tax on long-term capital gains and income distributed by equity oriented Mutual funds in the budget are still echoing. Equity or Mutual Fund investors are asking the same filmy question – God why us?

But my question is – Is 10% LTCG on Equity so bad?

LTCG Tax

There were some rumors that there will be a proposal to tax long term capital gains and the rumors turned out to be true! It has been announced that there will be a tax of 10% on long term capital gains over Rs. 1,00,000. Gains earned up to January 31, 2018 will be exempt. The long-term is defined as 1 year. If you have purchased shares last year and sell it in 2018, the gains the stock made till 31st January, 2018 will also be exempt from tax and only the difference in price from date of sale and price on 31st January, 2018 will be taxed. For more details, you can read FAQs shared by govt.

Why?

Some experts believe that corporate sector will be more affected by this than individual investors. This will help in generating more income for the government. The tax is an attempt to reduce fiscal deficit & support social programs.

Moreover, this will help curb fraud in cases where a lot of income is converted into investments and taken back in the form of long-term capital gains.

For You

Individual investors who are into long term investments are there for the growth potential and the tax may not make much of a difference to them in long term.

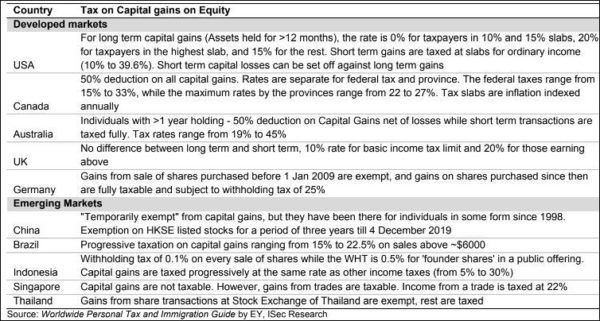

Most countries tax capital gains & much higher than 10%. Now that India has proposed to levy taxes, there are only 5 countries that do not levy tax on capital gains. US, China, Germany, South Korea, Brazil all charge tax on capital gains. So the argument that foreign investors will stay away because of tax may not be a strong one. If India continues with a strong economic growth rate and remains politically stable, global investors would not shy away from investing.

Indian’s love tax saving – they can invest in even suboptimal products to save that. That’s purely your choice…

Equity Capital Gain Tax – World

BUT

But this could also set a trend where the tax rate keeps getting increased. That will not be beneficial to the common man. There is already a lot of tax on equity transactions – Service Tax, Securities Transaction Tax, GST, SEBI charges and Stamp charges. Now there will be additional tax on the income earned. Cont……

Focus on things that are under our control…

Dividend Distribution Tax

Equity Oriented Mutual Funds will have to pay a dividend distribution tax of 10% post this budget. This is to bring parity across growth funds and dividend funds. If they haven’t introduced this – we all would have shifted to dividend options : )

Now what?

Long Term Capital Gain & Dividend Distribution Tax means the amount to be distributed to investors or growth after tax will be less. But that does not mean that you stop investing in equity mutual funds as they still have the potential to give good returns in the long run.

The total amount in your hands or the value of your investment will be lesser than it was in the previous years and that can be handled by reviewing the financial plan.

Tax saving should be part of your investment planning, not vice versa.

My view till this point is 10% is reasonable & you should stick to your existing investment strategy.

Please share your views in the comment section.

")

Thanks Hemant for this article. I was eagerly waiting for it. 🙂

I just want to ask your opinion on ELSS mutual fund investment. As ELSS is long term investment so it will attract LTCG. Can you please advise if dividend option in ELSS will also have 10% tax on dividend even if annual dividend amount is less than 1 lakh INR ? Please advise.

Hi Ashish,

Dividend has no relation with Rs 1 Lakh limit so even if there’s Rs 1000 dividend it will be taxed. I can be wrong but my view is – you will hardly see dividends from equity MF in future.

Well, the government is definitely going to come after your money, no matter where you invest.

You can not escape 2 things, 1. Death and 2. Taxes

SO accept this reality and live with it.

Equities are going to out perform other asset classes despite this tax.

Agree Mohit.

What are the ways to minimize the LTCG tax if there are any or plan in such a manner that the impact is the least? Are there any such options? Like book gains < 1 Lac in the current FY and then reinvest in the next FY?

Hi Hemant, What tool we can use to calculate the LTCG taxes?

long-term capital gains and income distributed by equity oriented Mutual funds in the budget are still echoing. thanks for sharing.

hi hemanth,

wanted to know..whether for long term wealth creation will ULIP or MF(equity)?

thanks,

Yogindra

Hi Yogendra,

I think still MF is a better option due to transparency & flexibility.

Thanks for sharing this information…

Comments are closed.