Investment risk is not totally straightforward. There is an inherent risk in financial markets, but what happens outside the markets in your everyday life can impact how you view risk too.

Your professional stability, family matters, and wellbeing, among different variables, will affect your resistance for risk. When contemplating your Financial Plan, you ought to comprehend not just the risk attributes of different investments and financial markets, but the risks in your personal life as well.

Check – Low-Risk High Return – Is it possible?

Investment Risk & Return

The profits you receive on your investments are always related to risk. If you take a little risks then you should expect little return and large risk-taking “should” be rewarded with large returns. (really – must check the chart in next part)

Views on risk can vary. Some see risk as simply losing money and others see risk as volatility. Volatility as a financial measure refers to the doubt about the size of the changes in a security or asset’s value.

A higher volatility means that values can potentially be spread out over a larger range and the price of the security can change dramatically over a short time period either positively or negatively.

A lower volatility means that a security’s value does not swing dramatically, but changes at a steadier pace. The measure of volatility requires a period of time, be it minutes, days, weeks, or years. In general, the longer the time period, the lower the level of volatility.

Read – 5 Things you should know about Risk & Your investments

An Eye-Opening Risk Chart

How many times you have seen the below graph which gives the impression that “riskier assets produce higher returns”. But if risky investments could be counted on to produce high returns, they wouldn’t be risky. 🙂

With higher risks come higher rewards. That’s one of the most basic rules of investing.

However, it’s also one of the most misinterpreted rules.

“We hear it all the time: ‘Riskier investments produce higher returns‘ and ‘If you want to make more money, take more risks,'” Howard Marks. “Both of these formulations are terrible.”

Marks believes investors deserve a more complete explanation of the risk-return relationship.

“There’s another, better way to describe this relationship: ‘Investments that seem riskier have to appear likely to deliver higher returns, or else people won’t make them,'” Marks writes. “This makes perfect sense. If the market is rational, the price of a seemingly risky asset will be set low enough that the reward for holding it seems adequate to compensate for the risk present. But note the word “appear.” We’re talking about investors’ opinions regarding the future returns, not facts. Risky investments are – by definition – far from certain to deliver on their promise of high returns.”

Howard Marks shared a brilliant risk-return chart – See below.

As you move to the right, increasing the risk:

- the expected return increases (as with the traditional graphic),

- the range of possible outcomes becomes wider,

- and the less-good outcomes become worse and ultimately become negative.

The straight line going from the bottom right to the upper left is how most people envision the risks-return dynamic.

However, it’s the curves and vertical lines at each point that every investor better be comfortable with. While the point represents what is expected to happen, the curve represents the range of outcomes the will actually happen.

“This is the essence of investment risk,” Marks writes. “Riskier investments are ones where the investor is less secure regarding the eventual outcome and faces the possibility of faring worse than those who stick to safer investments, and even of losing money. These investments are undertaken because the expected return is higher. But things may happen other than that which is hoped for. Some of the possibilities are superior to the expected return, but others are decidedly unattractive.”

A brilliant way to explain the relationship between risk & return.

Equity Risk Vs Debt Risk

Of the two major asset classes, equities for which returns are dependent on dividends and earnings growth, have a higher long-term expected return because there is greater volatility to these returns.

Fixed income (debt/bonds) which pay interest periodically and their principal at maturity provide lower returns and are generally less volatile than equities.

Must Read – Risks in Mutual Funds that you may not know

Your Risk Profile

Risk and risk tolerance are tough to interpret and almost impossible to quantify.

Although tools are available for risks profiling – when trying to pin down your risk tolerance, you should think about the following concepts:

- People tend to be more optimistic about stocks after the market goes up and more pessimistic after the market goes down.

- Too much weight is given to recent market information and too little weight is given to long-term fundamentals.

- Overconfidence leads to excessive trading and ultimately underperformance.

- Your actual tolerance for risk is typically less than your stated tolerance for risk.

- What is the maximum value your current portfolio has lost in the past? Can you tolerate such a loss when your portfolio will be 5 times in size?

Volatility will scare you

Volatility can cause you to abandon a well-thought-out investment plan at very inopportune times. When considering your own risk tolerance, you should be aware of how widely investment performance can vary even within a single year.

Consider 2008, the year when large-cap stocks fell over 50% within a few months. Mid-caps were down by 70-80% – even Mutual Funds were down in the same range.

In gauging your risk tolerance, you should reflect on your feelings and actions during bear markets or think about how you would react during your current portfolio’s worst periods of past performance.

Check – Effect of holding period on your returns

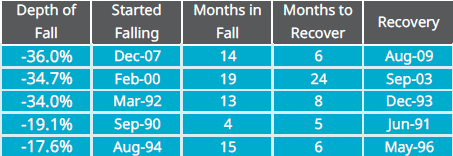

Maximum Fall in a 70% equity & 30% debt portfolio in India between 1988 to 2018. (Check below table)

The above portfolio was rebalanced every year.

35% fall in a 70:30 portfolio means that equity was down by more than 50% in this period – assuming debt was generating a normal return in this period. Are you ready for this?

Although staying with your Financial Plan when it loses money can be extremely frustrating at times, you can’t predict the sudden shifts in market returns.

Missing out on large market recoveries or even a few days of gains can severely hurt the returns of your portfolio.

Hope you got a new perspective about risk. Please add your views & questions in the comment section.

")

An excellent article. For the first time Ihave understood risk.Pl do keep sharing such articles.

Do you conduct workshop for increasing financial literacy of investors? If so pl share details

Thank Deepak for appreciating.

Right now we are not conducting any workshops.

Your post has changed my perception of a risk. Viewing risk as a volatility makes more sense than viewing it just as loss of money. Do keep sharing such articles which explain crucial and important points of finance subjects in such an easy and simple language.

Thanks for sharing your views.

Amazing post, very helpful. Thanks.

its really very amazing bog site with so much helpful information. thank you very much for writing here for us.

Putting your investment in wrong business can cost you the whole investment. Before investing your money understand all factors involved with that business.

I think no one should invest with an approach like higher risk will give you higher returns. Taking higher risks just for the sake of higher expectations may lead to such a loss that a person will never come back to investments. This is not easy as the risk related to investments depends on several aspects including the country’s economic performance, or trading problems around the world. You should only take risks about an investment when you have thought ahead of the time and think that this investment is worth for long term.

Thanks

Comments are closed.