Don’t take me otherwise I don’t have anything against HDFC mutual fund or their star fund manager Prashant Jain.

Plus, most of our clients have exposure to HDFC funds.

So why I am happy with underperformance?

In the last 16 years of my investment career, I have seen Prashant Jain keeping his head cool in all kinds of scenarios.

We also have to understand when you are investing in active funds – the fund manager or AMC has the right to make decisions in our best interest.

Plus we also have to check risk when we are talking about returns. This post can explain – How should you view investment risk.

Disclosure: I worked with HDFC Mutual Fund before starting my financial planning practice in 2009 but this article has no relationship with that.

Note: In this post when you read HDFC (replace that with any mutual fund) or when you read Prashant Jain (replace that with the name of any good fund manager).

But underperformance of funds is impacting my portfolio returns

Recently I got an email from one of our clients that HDFC Top 100 fund that we suggested is not performing and my answer was I’m really happy about that.

He was as confused as you are right now.

Let me ask “why you have given your money to an active Fund Manager?” Let me guess because you want to outperform markets over a long period of time.

But what is a long period of time, 3 months or 6 months or 5-10 years? If your answer is in months you are in the wrong place.

Really Hemant?

You expressed your disagreement in the humblest manner as possible in this situation “Hemant don’t try to be smart; I have seen fund returns on a 5-year basis and they are underperforming their peers.

For your convenience, I am sharing that here.”

(Oops I forgot this is information age)

You’re right but even a one-year performance can make a huge difference in 3 or 5 years performance.

Let me give you an example:

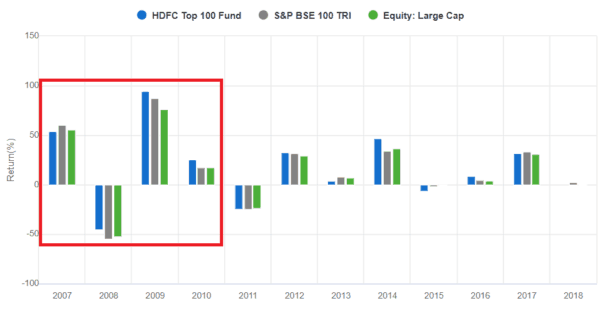

This below fund underperformed its peers till 2018 but just because of a one-year phenomenal performance – long term track record looks much better.

2007 Vs 2008 Vs 2009

I clearly remember at the end of 2007 HDFC funds were underperforming their peers by decent margin & fund advisors and clients were all up in arms against them.

Funds also saw huge redemption pressure because why investors should sit in the train when flight tickets are available at the same price. So, they exited & entered the best (performing) funds of that time.

Then came tsunami of 2008 & markets were down by 50% in less than a year. HDFC Funds fell lesser than its peers & they saved people’s money.

In 2009 when markets went up they outperformed their peers by a huge margin.

Media or many finance professionals do not talk about the importance of “downside protection”.

Must Read: Low Risk – High Return investment

Prashant Jain is managing funds for more than 2 decades and unarguably may be one of the best equity fund managers that we have seen in our lifetime. Let me make a bold statement “not every fund manager has the nerve to avoid peer pressure and pressure from investors – Prashant Jain is a rare breed.”

Bubble in Quality

Recently one of the ex mutual fund managers shared a report & argued that so-called quality stocks are in bubble territory. As I love to research, I checked which AMCs or funds have exposure to those stocks so to my surprise HDFC has one of the least exposure in those companies.

They have zero exposure in 90% of those companies mentioned in the list.

Prashant Jain in one of the interviews “I do not believe in contra investing but I do believe in value investing. And if value investing at a point of time means that you think differently from others then so be it. I have always tried to buy reasonably quality businesses, not always high quality because sometimes they are very expensive and I have always focussed on what you pay for them.

It is quite logical that when a good business is passing through a challenging time or when some other businesses are doing extremely well on the stock markets and since most people in life and in stock markets as well are very short term focussed, they want to avoid short term pain and get short term gains. When almost everyone wants to buy certain stocks in the markets, it is obvious that the rest of the spaces tend to become more valuable and if you are seeking value, then you become a contra investor. So contra is an outcome of seeking value but seeking value is the key.”

The Biggest Problem With Your Financial Planning, And How You Can Fix It

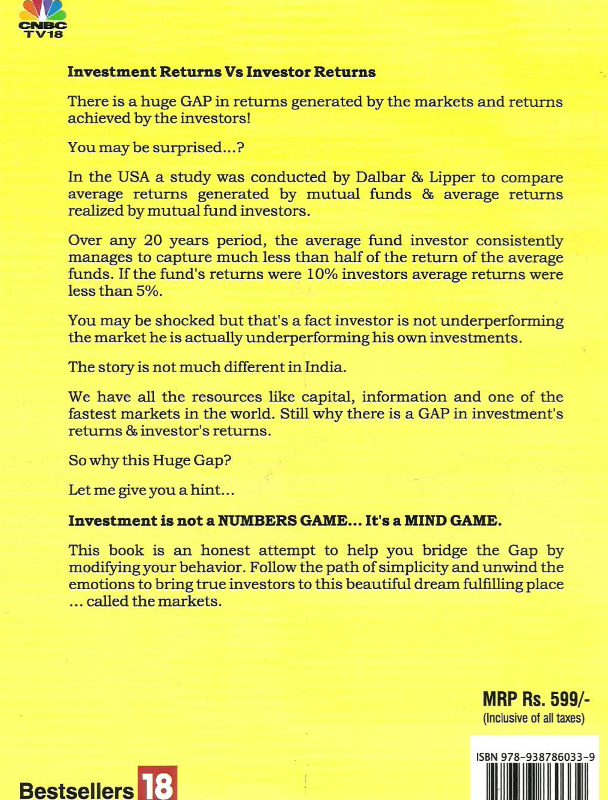

GAP: Investment Returns Vs Investor Returns

This is what I have written on the back cover of my latest book “Modifying Investor Behaviour”. We have got very good feedback – you can check on Amazon.

There are many reasons for this GAP. One of the main reasons is that when funds are generating good returns (hot funds/ best funds/top funds based on recent performance) investors flock in them and when the same fund is not performing for few quarters or 1-2 years they will prefer to exit.

Peter Lynch one of the top fund managers of Fidelity managed a fund from 1977 to 1990 & generated more than 29% returns (this is better performance than Warren Buffett) but you will be shocked investors did not get even 15%. I hope now you know WHY.

What should you do?

Talk to a good financial planner 😉

I always believe that if someone makes a relationship because of your beauty or money he/she will leave when you lose that. Or your employees joining you ONLY for getting a higher salary from their earlier company they will leave you for the same reason in the future.

Similarly, if you have selected your funds only on the basis of performance you will exit those because of short term underperformance. Performance is important but it can’t be the only criteria.

I am not at all claiming that this fund or any other fund will outperform in the future or how history will remember Prashant Jain or any other fund manager. I have no idea how the market will perform in the next few years & which investment strategy will do better.

That’s the reason Asset Allocation & Diversification is important – you should have exposure to 5-6 fund houses. Allow those active fund managers to try their investment styles to generate better returns for you.

It’s time to stop making haphazard decisions about your INVESTMENTS

and instead talk to us about your GOALS.

Financial Planning Service

Just add any question, observation, suggestion or advice in the comment section.

in Indian Stock Markets")

")

Now that expense ratios keep changing every now and then, how do we handle them.

Hi Deepak,

5-10 basis points are fine but if there’s 25-30% you can consider that.

Hi Hemant,

I was really concerned about my mutual fund investments performance but your article make perfect sense.

Thanks Raghu

I can just say a very timely post.

Thanks 🙂

All Asset Classes revert to the mean.

Real Estate may go up 50% in one year but over a 15-20-30 year period the cagr will be 7% to 8%. In addition you should be 2% to 3% in rental returns. Cumulative returns will be 10% to 12%

Equities may go up 25% in one year but over a 10-15 year period the cagr will be 10% to 12% especially after including dividends

Within Equities there may be a deviation for a period of time with large cap growth stocks enjoying dramatic increase due to herd instinct for safety. This is particularly true when there is a lack of trust in financial markets. When auditors have been negligent or complicit in fraud. When rating agencies have been negligent or complicit in fraud. Suddenly corporate governance cannot be taken for granted.

Eventually sanity will return and we will see a reversion to the mean when mid-cap and small cap value stocks should find their rightful place in the sun.

Hi Rau,

Thanks for sharing your views – hope this will help other readers to understand “revert to the mean concept” & also having the right expectations.

Timely post explaining why we should consider downside protection for any investment.

Thanks for appreciating 🙂

u always write truth

Thanks Anil.

Good insightful article.. Please send me the guide, thank you

Good insightful article.. Please send me the guide, thank you.

Good article for current market conditions. But missing some info like “when market performing good we need to wait and when market at bad condition need to add more instead coming out” of that particular fund. Since before investing we will do some study, simultaneously we need to give some time to market and to fund manager for better growth together.

Thanks Ranjith for sharing your views.

There is so many funds and reports of performance of each fund. How to select right fund and what should be right strategy to monitor the performance of the fund. Can you provide some inputs on these aspects?

Hi Ajit,

Hope you got some idea from the secret guide 😉

Unbiased advice.

Thanks

Thanks Satyaprakash 🙂

Good read but HDFC AMC Fundwise evaluation would be more interesting

Hi Satish,

The idea was not to lose patience if you are investing in active funds.

Good article..

Thanks 🙂

I am following your articles since last 8 years, I have been a regular reader since then but out of all your articles I find this article the most disappointing one. You have always been an advocate of having diversity but you said your investors to invest in maximum 2-3 funds. Yes that was in 2011-12. In 2019, now you yourself have increased it to 5-6 fund houses? Your suggestion of increase in number of funds is due to the uncertainty of market that you have talked about at the end of your article.

Hi Manoj,

I thank you for being one of the most active readers on the blog 🙂

Coming to the point that you have raised – I don’t remember if I ever said a maximum of 2-3 funds or fund houses in any blog post. It may be possible that someone asked a specific question about his situation (maybe very small amount to invest on a monthly basis or just talking about investing in ELSS) – in that case, I may have suggested lesser funds.

Bw we have completed 10 years in Financial Planning practice & from day one we are suggesting our clients have exposure in 5-6 fund houses.

Good article for current market conditions. But missing some info like “when market performing good we need to wait and when market at bad condition need to add more instead coming out” of that particular fund. Since before investing we will do some study, simultaneously we need to give some time to market and to fund manager for better growth together

Thanks Rajith.

Units of good mutual funds are Assets. When investors mindset changes to accumulation of these assets for achieving long term goals, then they will surely enjoy underperformance during polarised market conditions. Choice is between short term notional gain or long term real gain. Choice is between making money or creating wealth. Your timely article is helpful to understand this in simple way.

Thanks a ton, Andrew – I am sure your views will help others 🙂

Good article

Thanks

All those cursing and regretting investments in MF should read this hard hitting article.Any one selecting a MF based on current rating of a Scheme which is based on last 1 year performance will join the band of cursors after a year. If you stay within the Top 4 or 5 Fund houses and choose to wait for 3 to 5 years with a target of not more than 10 to 12 % post tax -5 year CAGR , you are doing well. Why bother about temporary slides .

Stay close to Prashant Jain Types – Invest and forget it.

Thanks a ton – Ravindran 🙂

Good article. But I still do have a question in what is the right amount time to move away from a fund? After how much time of underperformance (1 year-2 year) or what other factors should the investors consider before making the switch?

Hi Chirag,

I will suggest you check the 5 points that I have shared. If questions are specific about underperformance – it should be atleast 2 cycles, One Up & one Down.

I think that the secret guide that I shared with you will help. 🙂

Yes. The wait is needed if we have done the right analysis while doing fund selection

Thanks for sharing your views.

Right article at the correct time. People would be wondering why market is going up but my fund returns are not going up proportionately

Thanks Rahul 🙂

Good insights

What about the poor quality stocks in his portfolio like SBI , canara bank who have an history of surviving on and burning tax payers money given as doles by the government

Hi Ujjwal,

I don’t want to comment on specific stocks but fund managers don’t have compulsion to buy “poor quality stocks” so there may be a reason why the hold them.

Nice refresher to be cool, calm and logical in these times when only few stocks or MFs are performing and giving returns but not many are talking about the risks these stocks/MFs hold. Equity investments is a long term game and not for the faint hearted. Asset allocation is the key to attaining wealth and have portfolio stability at the same time and keep your heart beat in check.

I am an avid reader of your blogs, posts..they are different from the lot…Thanks again.

Thanks Tohid – you made my day 🙂

The present scenario in the equity markets is very dicey.Many of the blue chips are at record highs. many midcaps & small caps have taken a severe beating in values. The problems in the NBFC sector have increased specially after the collapse of ILFS. Many mutual funds having exposure to the NBFC sector have also been badly affected. What is the way forward for individual investors?

Dear Haridas,

I can understand your concern nut equity markets are always like this.

I will suggest you read this https://www.retirewise.in/2018-was-good-for-the-equity-investors-will-2019-be-better/

Nice analysis. You rock Sir!!

Thank You 🙂

Good Article

Hi Hemant,

I am following TFL from last few years, I can confidently say it’s the best financial site.

Thanks a ton 🙂

Sorry sir still did not understand why you are happy.

Hi Krishan,

I am happy that a fund manager is not mimicking the index & ready to take career risk.

Nice article but how to select a good fund in current scenario.

Thanks Hemant for nice analysis.

Mr. Prashant Jain and Mr. Sunil Singhania (now left Reliance MF so ex Fund Manager) are best money managers in country. They understand our domestic equity markets most efficient way.

The current market behavior is very weird and irrational. Most of the benchmarks (excluding nifty 50 and. Sensex 30) are underperforming. It implies the companies (bse 500) are not performing well which also can be seen in macro data. So unless the economy starts to kickoff, market will miss the multiplier impact. So fund value will also not be multi folded.

Hi Bikram,

Thanks for sharing your views.

Thank you for sharing about this article,. Wish you always beautiful and good luck in the following article

Nice article. I have been investing in HDFC funds for 10 years now and one of the reason is Prashant Jain.

Thanks Mitesh 🙂

Dear Hemant

I was studying turnover ratios of few mutual funds. Few Hdfc funds turnover ratio is below 9% and Index fund turnover ratio is above 16%. I am bit confused why active fund managers turnover ratio is below 10% which is reflected in their performance. What is your take on this?

Do you agree with value style investing in most of the HDFC funds?

Dear Hemant

I was studying turnover ratios of few mutual funds. Few Hdfc funds turnover ratio is below 9% and Index fund turnover ratio is above 16%. I am bit confused why active fund managers turnover ratio is below 10% which is reflected in their performance. What is your take on this?

Do you agree with value style investing in most of the HDFC funds?

Thank you for sharing this great article, all the content inside is very suitable for everyone, the accompanying image is also a lot of quality. Hopefully the next article will be better to be useful to everyone.

Hi, I think your site is so cute! I’d like you to know that I nominated you for a Award!

The story heading is why hdfc mutual fund is doing bad. But you never said why it is doing bad. please explain in simple terms. I lost more than 12 laks is hdfc mutual fund. Now i am at risk that i cannot sell or hold

please guide me

Hi Govind,

I mentioned that these are active funds so you have to be more patient.

Comments are closed.