Is debt mutual fund risk-free? asked a prospect recently. It is a misconception that debt instruments are risk-free.

All investments carry an element of risk. It is important not only to understand the advantages but also the risks of investing in debt mutual funds.

Many people are not comfortable investing in equity and equity-related products due to volatility and risk of returns and therefore invest in debt. Fixed deposits, GOI bonds, Certificates of Deposits, PPF, Debt Mutual Funds, etc. are debt instruments.

Check – How Healthy Is Your Mutual Fund Portfolio?

Debt Mutual Fund Risk

Let us look at the key risk in debt mutual funds –

Credit Risk in Debt Mutual Funds

Risk of Default – Sometimes, bond issuers can default in payment. This will result in a loss. Even if you have invested in debt mutual funds that have invested in bonds and there is a default in payment, your investment will lose value. Even reduce in rating will impact your NAV.

What can you do – Check the credit rating of the securities that your mutual fund invest in. Check the quality of the portfolio and fund management of the mutual fund scheme that you invest in.

Lower ratings mean higher return but with risk – if you don’t want to take this risk, invest in securities with high credit ratings (AA+ and above). Keep a watch on rerating of securities and payment defaults of loans etc. by the organizations issuing the bonds as this can mean there are issues.

If you want to take credit risk – there’s a specific category with the Name of “Credit Risk Mutual Funds”. That doesn’t mean that all other debt funds don’t have credit risk.

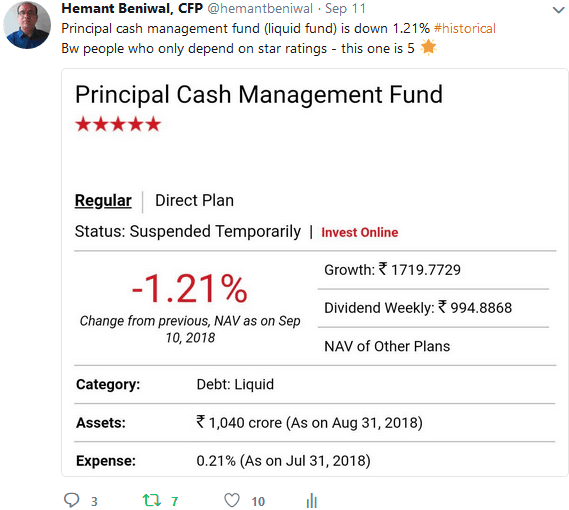

For example – Few days back IL&FS was downgraded & that had a huge impact on funds with exposure to this company. Even the safest categories like liquid funds & ultra short-term funds gave negative returns.

I think it’s very important to understand the risk in debt mutual funds before investing.

You can connect with me on Twitter

Interest Rate Risk in Debt Mutal Funds

Risk of Movement in Interest Rates – Interest rate movement affects debt portfolio. If the interest rate goes up, your returns will be lower. Suppose you invest in a 5-year bond that gives 6.5% interest per annum and 2 years down the line, interest rates move up to 8%. You are stuck with that investment with a lower rate of return.

If interest rates go higher, the value of your bonds will go down. So if you have invested in a mutual fund scheme that has investments in these bonds, then the NAV value of the MF scheme will go down resulting in erosion of the value of your assets. If the interest rate goes down funds with a longer duration can generate better returns.

Must Read – Low Risk High Return Investment – is it possible?

What can you do – Keep a lookout for interest rate movements and invest accordingly.

OR accept the interest rate risk invest in long-term funds with the expectation of higher returns in the long term but with volatility.

OR Invest in dynamic asset allocation funds that do not have restrictions on investments and fund managers can adjust the asset allocation based on market conditions.

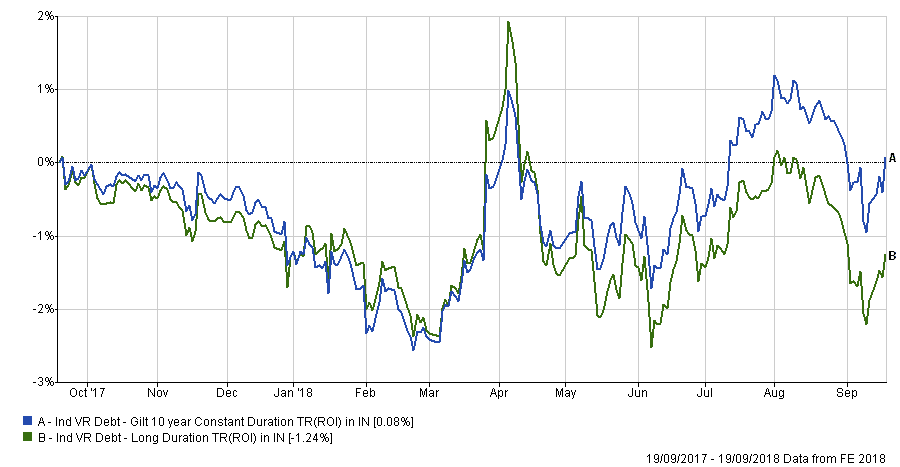

Example – in last 1-year interest rates in India are rising so you can see volatility in long-term debt funds. You can see between April & June such funds lost 4% – and in 1 year there’s no return in these funds.

Read – 9 risks in mutual fund investment

Liquidity Risk in Debt Funds

Risk of Illiquidity – The market for bonds is not active. You or even the fund manager may not always find buyers in the secondary market when you want to sell your bonds. This can affect your liquidity position.

Other debt investments like PF, Fixed Deposit, etc. can be liquidated but you have to pay a penalty. Equity and equity-based instruments are more liquid in nature in comparison to debt investments.

What can you do – Maintain a diversified investment portfolio. Ensure you have emergency cash.

You can invest in debt mutual funds as they can be sold off easily – even if mutual funds are stuck in illiquid positions they will not say no to investor redemption. This may impact the NAV, returns & portfolio quality but still, you will get your amount except in some emergency situations.

Check one risk that will apply to all debt investments………

Check – why debt will always give negative return [with Calculation]

Risk of Inflation –

Debt instruments have a fixed rates of interest as returns. They are also on the lower side. Inflation, on the other hand, grows steadily at a compounded rate. Inflation eats into your returns. If it is greater than the interest rate you get (after tax), you will have a negative real rate of return. For example, inflation is 5% interest earned on an FD is 6% (if you are in the highest tax bracket – after tax you will get less than 4.5%) – then your returns are in the negative zone.

What can you do –

As an investor, you should have an asset allocation plan based on your age, risk tolerance and risk capacity levels. You should not invest only in debt instruments but in other assets as well. Even within debt instruments, you can invest in different types such as FMPs, Government Bonds, Debt Mutual Funds and Certificates of Deposits. Avoid prioritizing or investing a large sum in bonds of high-risk companies and new financial institutions. You can get the advice of a professional financial planner to invest such that you get the maximize your returns and minimize your risks.

Hope now onwards you will not ask – is mutual fund investment risk-free? Please feel free to ask questions regarding debt mutual fund risk in the comment section.

I have not shared one major Risk in this post – if you can guess that in the comment section (with why you think that’s a risk), I will share our secret weapon to reduce that risk with you. Even if your answer will be different from mine or same as everyone else you will get that from my side 🙂

Great Info. Thank You For Telling Us The Risk About Dept Mutual Fund

Welcome 🙂

Except a single investment ,PPF,PRACTICALLY all debt instruments are tax inefficient as compared to equity investments.

That is a risk.

Thanks for Sharing your views Rajnikant 🙂

Hi Hemant, great read mate. Re quiz: is it reinvestment risk?

Hi Mihir,

Yes, reinvestment is one of the major risks in all debt investments.

WHAT IS THE SAFE AND SOUND OPTION FOR INVESTMENT -EQUITY, DEBT ,OR BALANCED FUNDS.AS YOU HAVE GIVEN YOUR VERY GOOD ADVICE ABOUT RISK IN DEBT.THEN OPTIONS ARE EQUITY OR BALANCED FUNDS .PLS GUIDE TO INVEST PROPERLY.REGARDS .

Hi, Hemant !! It is the re-investment risk, I believe.

Very useful article .it provides the solution to combat the risk involved.

Thanks Mr Om

I read your blog and it is always helpful. Your tips on investing are excellent.

I am investing in these 40,000 schemes from 2015. I am 27 yrs. old I want to accumulate wealth when I am 50 and goal is around 2 crore.

I have done a lot of research before investing it. All are direct plans. I just want to evaluate my portfolio and need you help to understand your views.

Kotak Emerging Equity Scheme – Mid Cap – 5,000

Reliance small cap – Small Cap – 5,000

Parag parikh long term equity – multi cap – 5,000

SBI bluechip – large cap – 15,000

Aditya birla sunlife front line equity – large cap – 10,000

Great article not sure why advisors don’t talk about this.

Hi Pradeep,

It’s not easy to handle objections if the will talk about risk 😉

Nice article. Thanks

thanks 🙂

Hi sir,

Thanks for writing an awesome blog post this article is really helpful for me to thank you so much, sir

Thanks for appreciating 🙂

I have always admired your site, Thanks for the great tips and work .

Thanks for appreciating 🙂

Hi Hemant, I guess at the end of the article you were talking about risk profiling in terms of planning your portfolio? Please correct me if I’m wrong.

Hi Deepak,

Investments should be backed with investors’ risk profile.

Very informative article. Look forward to more such reads.

Thanks Prabhkaran 🙂

Re-investment risk

Comments are closed.