People keep me asking why there are so many different types of mutual funds schemes in India. We have to understand that a mutual fund is just the connecting bridge or a financial intermediary that allows a group of investors to pool their money together with a predetermined investment objective. And due to different investment objectives, there are different types of mutual funds.

Must Read –How Mutual Funds Work?

The mutual fund will have a fund manager (team of experts) who is responsible for investing the gathered money into specific securities (stocks or bonds). When you invest in a mutual fund, you are buying units or portions of the mutual fund and thus on investing becomes a shareholder or unitholder of the fund.

The profits or losses are shared by the investors in proportion to their investments. The mutual funds normally come out with a number of schemes with different investment objectives which are launched from time to time. A mutual fund is required to be registered with the Securities and Exchange Board of India (SEBI) which regulates securities markets before it can collect funds from the public.

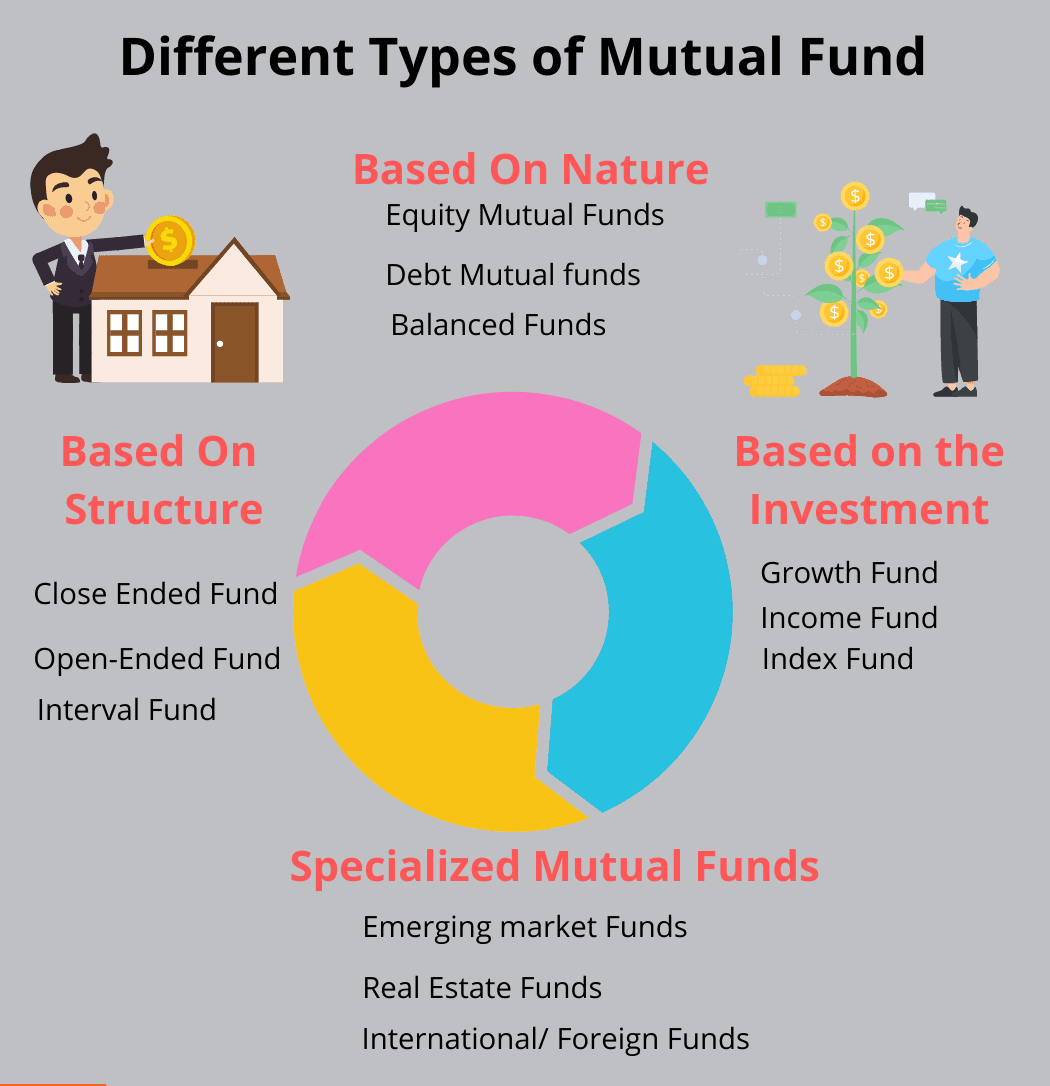

What are the types of Mutual Funds In India

| By Nature | By Structure | By Investment Objective |

| Equity, Debt, Balance | Closed-Ended Funds, Open-Ended, Funds Interval funds | Growth Schemes, Income Schemes, Balanced Schemes, Index Funds |

Let us discuss each of these types in detail:

Read- How Healthy Is Your Mutual Fund Portfolio?

Based On Nature

Equity mutual funds

These funds invest a maximum part of their corpus into equities holdings. The structure of the fund may vary differently for different schemes and the fund manager’s outlook on different stocks. The Equity Funds are sub-classified depending upon their investment objective, as follows:

- Diversified Equity Funds

- Multi-Cap Fund

- Value Fund

- Dividend Yield Fund

- Mid-Cap Funds

- Small-Cap Funds

- Sector Funds

- Tax Savings Funds (ELSS)

Equity investments are meant for a longer time horizon, thus Equity funds rank high on the risk-return matrix.

Check – 7 Things We All Hate About Mutual Funds

Debt mutual funds

The objective of these Funds is to invest in debt papers. Government authorities, private companies, banks, and financial institutions are some of the major issuers of debt papers. By investing in debt instruments, these funds ensure low risk and provide stable income to the investors. Debt funds are further classified as:

- Gilt Funds

- Income Funds

- Monthly Income Plans – MIP

- Short Term Plans

- Liquid Funds

Balanced Funds / Hybrid funds

As the name suggests they, are a mix of both equity and debt funds. They invest in both equities and fixed income securities, which are in line with a pre-defined investment objective of the scheme. These schemes aim to provide investors with the best of both worlds. The equity part provides growth and the debt part provides stability in returns.

If you want to Know Mutual Fund Investment watch this Video

Money Market Funds

A money market fund is a type of mutual fund that invests in highly liquid, short-term securities. These may include cash, cash equivalents, and high-credit-rating debt-based securities with a short-term maturity. Money market funds are designed to offer investors high liquidity with a very low level of risk. Money market funds are also called money market mutual funds.

Based on the Investment objective

Growth Fund

Growth Schemes are also known as equity schemes. The aim of these schemes is to provide capital appreciation over the medium to long term. These schemes normally invest a major part of their fund in equities and are willing to bear a short-term decline in value for possible future appreciation.

Must Check – Portfolio Safety : Is Your Portfolio Risky?

Income Fund

Income Schemes are also known as debt schemes. The aim of these schemes is to provide regular and steady income to investors. These schemes generally invest in fixed-income securities such as bonds and corporate debentures. Capital appreciation in such schemes may be limited.

Index Fund

Index schemes attempt to replicate the performance of a particular index such as the BSE Sensex or the NSE 50. The portfolio of these schemes will consist of only those stocks that constitute the index. The percentage of each stock to the total holding will be identical to the stock’s index weight age. And hence, the returns from such schemes would be more or less equivalent to those of the Index.

Based On Structure

Close Ended Fund

A close-ended fund or scheme has a stipulated maturity period For eg. 5-7 years. The fund is open for subscription only during a specified period at the time of the launch of the scheme. Investors can invest in the scheme at the time of the initial public issue and thereafter they can buy or sell the units of the scheme on the stock exchanges where the units are listed. In order to provide an exit route to the investors, some close-ended funds give an option of selling back the units to the mutual fund through periodic repurchase at NAV-related prices or they are listed in the secondary market.

Open-Ended Fund

An open-ended mutual fund is the most common type of mutual fund available for investment. An investor can choose to invest or transact in these schemes whenever he likes to. In an open-ended mutual fund, there is no limit to the number of investors, shares, or overall size of the fund, unless the fund manager decides to close the fund to new investors in order to keep it manageable. The value or share price of an open-ended mutual fund is determined at the market close every day and is called the Net Asset Value (NAV).

Interval Fund:

Interval Schemes are that scheme, which combines the features of open-ended and close-ended schemes. The units may be traded on the stock exchange or may be open for sale or redemption during pre-determined intervals at NAV-related prices. FMP or Fixed Maturity Plans are examples of these types of schemes.

And there are new categories like ETF & Gold Funds. Hope now you are clear about various types of mutual fund schemes in India.

Dear Hemant,

I fall under 30% bracket. Looking into the recent spurt in FD rates I was prompted for it. However there is a advice from a Banker that instead of FD it would be bettrer to go for Debt fund because the return after 12 months would be subjected to long term capital gains tax @ 10% only. Where as against Bank FD the tax wpould be levied @ 30%. Would like to have your opinion.

regards

Shashank Selot

Dear Shashank,

Your banker has rightly advise you that it is a very good idea for people who are falling in 30% tax slab to invest in debt mutual funds rather than FD. If we assume that you can get 10% return in 1 year from FD & 9% from debt mutual funds – your after tax return in Mutual Fund will be 8.1% but it will be only 7% in case of FDs. But you should be aware that debt funds have Interest Rate Risk – change in interest rate will impact price of bonds. There is negative relation between price of bond & interest rates – if interest rate will increase price of bond will go down & vice versa. This risk can be reduced if you hold bonds till maturity. So only if your horizon is 3-4 year go for income & gilt fund otherwise you should stick to FMPs.

Check types of risk

https://www.retirewise.in/2011/09/types-of-risk.html

Dear Hemant,

Thank you very much for your advise. One more input that I have received is that after April 2011 Indexation is applicable as per (n-1) yrs rule. i.e Indexation will be applicable only if FMP is there for entire fiscal year after the end of fiscal year in which it was generated. i.e If now in Nov I invest in FMP and want to avail Indexation benefit than I will have to remain invested through the end of next fiscal i.e. till march end 2013 i.e in all 17 months. However this 17 months gets reduced to 13 months if the month of investment is March. Has there been any change to this effect ?

warm regards

Shashank Selot

Dear Shashank,

To understand indexation better you can read this article

https://www.retirewise.in/2010/03/fixed-deposit-vs-fixed-maturity-plan.html

Hello Hemant,

A very valid point. To clarify with respect to FMP:

Fixed maturity plans (FMPs) have been very popular with investors because they are more tax efficient than fixed deposits. If the FMP term exceeds one year, the income is treated as long-term capital gains and taxed at a flat 10% or 20% after indexation. In case of fixed deposits, the interest earned is clubbed with the income of the investor and taxed at the normal rate. That is why the 370-day FMP is the most common maturity in this category.

But this is set to change if the Direct Taxes Code (DTC) replaces the Income Tax Act from 1 April 2012. The changes are as follows:

1. The DTC will not make a distinction between long-term and short-term capital gains from debt mutual funds.All gains will be added to the income of the investor and taxed at the normal rate applicable to him. This means if you buy a 370-day FMP today, the gains will be taxed at the same rate as the interest earned on a fixed deposit.

2. As you rightly pointed out-For an investment to qualify for long-term capital gains, the asset has to be held for at least one year from the end of the financial year in which it was bought. So if you invest in an FMP right now, the one-year period will start only from 1 April 2012 and the term should extend till 31 March 2013 for the income to be treated as long term capital gains.

Will DTC kick in from April 2012, no one is sure(atleast I am not)? Secondly this high interest rate scenario will play out for some more so in case of FMPs also it makes sense to lock in for a longer period(assuming you have decided to go with FMP and understand the pros and cons of investing in FMP as explained by Hemant in link mentioned). As of now various there are various FMPs available in the market for more than 370 days. So to be on safe side go for an FMP with a longer duration.

Oops..the reply should be addressed to Shashank. I apologize for my hurry to both Hemant ans Shashank.

Hi Hemant

You have covered most of the funds under three broad categories. I would like to share here two types of funds which have a lot of similarities but are different.

1 Value Funds

Value funds are those funds that invest in relatively undervalued stocks with a potential to unlock value in the long run. They tend to focus more on safety and less on growth. These funds are particularly suitable for investors with a moderate risk profile.

2 Dividend Yield Funds

These are diversified equity mutual funds that mainly invest in high dividend yield stocks. They pursue a strategy of value and growth and tend to be more blended offerings. The tilt towards high dividend yielding stocks acts as a cushion in a falling market.

Hi Anil,

These funds cannot fall under some category – these are more or less a slight different focus provided to diversified equity funds.

Hello,

As usual very good article for learners. Anyone wants to know about MF in India in a nutshell, must refer this!

Keep going….Thanks!

Sunil

Thanks Sunil.

Good article which covers the basics of Mutual funds. Looking forward to a post which tells what kind of fund suits whom?

Than I have to write a book and in last page I will write – our pet dialogue “It Depends” 😉

Conditions apply here too…We shall wait for the book. When are you planning to bring it out?

Hi Kirti

What kind of fund suits whom?

Growth Funds

These funds are not for investors seeking regular income or needing their money back in the short term.

Ideal for:

Investors in their prime earning years.

Investors seeking growth over the long term.

Income Funds

Ideal for:

Retired people and others with a need for capital stability and regular income.

Investors who need some income to supplement their earnings.

Balanced Funds

Ideal for:

Investors looking for a combination of income and moderate growth.

Liquid Funds

Ideal for:

Individual investors as a means to park their surplus funds for short periods or awaiting a more favourable investment alternative.

Thanks a lot Anil for the guidelines. There are some 5000+ Mutual Funds in the market and different people give different opinions. For example:

I want to invest for long term. What is long term-3 years, 5 years or more?

If I decide to invest in Equity funds then should I go for Diversified Equity Fund or Midcap fund or ELSS fund or a balanced fund?

Hi Kirti

As far as investment in mutual funds is concerned it is not possible for any one to cover all possible situations and all types of investors. Hence only broad guidelines can be given. It is no surprise that different people give different opinions based on their own experience and understanding.

As per Hemant the definition of long term is more than five years. I know there are many advisers who consider even three years as long term. Some investors have recently pointed out that there have been periods in some stock markets where even during a period as long as ten years the markets have not gone anywhere. Moreover, we know that during last three years our market has not given much to equity investors. Hence I feel that it is better to keep investment horizon of more than ten years when we plan for our long term goals.

On the question of selecting funds also different advisers have different opinions. For example as per Value Research, first time investors should start their investments via SIP route only in balanced funds. They do not favour lump sum investments. They are against investments in sector funds. They have some model portfolios for different types of investors. They do not include balanced funds in growth portfolios.

I think for any investor proper asset allocation at different life stages is very important. Moreover investment in mutual funds is a dynamic process which has to take care of different situations.

I think core and satellite approach works best when constructing portfolio. Core to provide stability of large cap and large and midcap funds and satellite to give potential of high growth of multicap, mid and small cap and sector, thematic and gold funds.

How much to have in core and satellite is again a function of risk appetite of the investor.

Hello Anil,

Thanks a lot for a detailed,great,quick reply. I totally agree with you- long term should not be 3 or 5 years. 10 years is apt. And core and satellite approach seems to work best.

I follow valueresearchonline.com and am familiar with the approach you mentioned. Catch is mutual funds have now become like flavor of the season…taking example few years back SBI Contra Fund, Reliance Growth Fund were recommended by almost everyone.Now we are asked to drop them. SBI Contra Fund was in my core reportorial.

Just as we have rules for entry we should have rules to exit. I literally had to fight with my agent to get my investment back from SBI Contra.

Hi kirti

Yes, you are absolutely right. Rules for exit also do exist. One important rule is that investment in mutual funds is a dynamic process. Once you have selected funds for your portfolio and you have started investing regularly and systematically you can not afford to sit tight on your portfolio thinking that your job is over. For a mutual fund investor his job is never over. He has to keep a constant track of all the funds in his portfolio and to at least review his portfolio once a year.

During the review the performance of the funds has to be evaluated by comparing the returns with the index and peers. If a fund performs consistently poorly based on this criteria then a call to exit has to be taken.

When we are investing in equity mutual funds to meet our long term goals we have to slowly move out of the equity mutual funds to debt funds when we approach our goal. This has also to be done systematically and regularly over a period of time to avoid market risks. Normally an exit from a fund should be made only when either the money is needed or a better investment opportunity exists.

Hi Kirti

Recently I have come across comments of one Money Guru which I would like to share here.

There is only empirical data to define long term. Data says, your probability of making positive returns is very high if you invest for at least five years. This study has been done across geographies. There could be market phases where point to point returns even in the long term may be negative. In recent times owing to the large variability in returns, it has been found that tactical views matter too. If you overlay your strategic call with asset class-linked tactical view, it can enhance your returns over a period of time.

nice article for my type of beginers……….thanks hemant;-)

🙂

Hi Hemant

Here I am sharing information about two types of funds.

1 Capital Protection Oriented Funds

These are funds that endeavour to protect the capital as the primary objective by investing in high quality fixed income securities and generate capital appreciation by investing in equity / equity related instruments as a secondary objective.

2 Quanta Funds

These funds select securities based on quantitative analysis. The managers of such funds build computer based models to determine whether or not an investment is attractive. In a pure Quanta Fund the final decision to buy or sell is made by the model. However, there is a middle ground where the fund manager will use human judgment in addition to a quantitative model.

Yup Anil these funds should get some place in the categories – let me see. Thanks for sharing.

Hi Mr.Hemant,

I have investments in quite a few funds both SIP and lump sum. but there is one fund where I am stuck . actually i had invested in principal pnb tax savings fund and couldn’t keep track due to some problems. the value has eroded now. any suggestions ?

Hi Rashi,

If 3 years is not completed – you can’t to anything. If completed & you feel this fund is not good for your portfolio – you can exit & invest in some better fund.

Hi Hemant jee,

can you suggest 1-2 good liquid funds, want to park money in a non-equity instrument.

Hi Rashi,

Liquid fund should only be selected if your horizon is less that 3 months – you can check HDFC Cash Management Fund.

Hi Hemant

I would like to share here an interesting piece which I have recently read on

how different types of investors are reacting to the current volatility and which asset class they prefer the most.

For the first time or relatively new investor, there is some scepticism about risky assets and more interest in fixed income and gold. In this group, risk appetite has been quite subdued.

The investors who have gone through this kind of volatility in equities before, have learnt from experience and are holding steady; they are drawing from their earlier reactions and are not panicking.

The informed investors are looking for opportunities in all asset classes in this situation and investing.

Dear Hemant Sir

I am new to invest in mutual fund. Which is the best mutual fund for best return.

please help me

Hi Rajesh

Please read the post – Best Mutual Fund For SIP.

Hi Hemant

One category of funds mentioned is balanced funds. But it is a misnomer. From the name one gets the impression that this category maintains a balance of debt and equity which is not correct. The correct name for this category will be hybrid. Under hybrid we can have equity oriented or debt oriented funds. Then there is another category which has many features of balanced funds and goes by the name of dynamic fund.

Dynamic funds are specifically designed to switch seamlessly between equity and debt, depending on the market conditions. The fund manager of this scheme shifts between the asset classes based on their attractiveness as indicated by certain valuation metrics. Hence, in a rising market scenario, these funds will invest a larger portion of the corpus in equities and hold a lesser amount in debt and cash. In the case of a falling market, the scheme will allocate more money to debt and, perhaps, hold more cash, while slashing the exposure to equities.

Rightly mentioned Anilji. That’s why even if people decide to invest in Mutual funds with 5000+ schemes and so many varieties one end up getting confused and just go with their financial adviser or agent.

Balanced fund had 65% in equity and as you rightly pointed out they are actually not balanced.

Hi Hemant ,

Hemant am serving in Air Force, presently posted to delhi area. Had gone throught your majority of blog/ articles on investment viz a viz financial know hows. Really am impressed by your grass root level information which any novice could absorb easily, also had recommended your advice to my elder bro who is working in surat diary age 35, having 35K pm income and had already overinsured himself with as many as 7 policies with majority of them having money back plans. Your articles on insurance was an eye opener for him. Also please include more information if possible on defence personnel investment apart from your previous article.

Best wishes ,

Akshay Dave

Hi Akshay,

Thanks for your kind words – actually information at TFL is not specific to any segment. This is a general personal finance information so that it can be used by everyone – there is lot to write but very limited time.

Hi Hemant/Anil,

Another useful article.. My question to you is, say when we are investing for a period of 15 years in mutual fund growth option, is it important to switch our portfolio to debt funds say after 13 years where we are nearing our goals..What should be the exact strategy? If we stay in the growth option for exactly 15 years and the 15th year brings downfall to markets then we might have to wait another 3 years to coverup..So is it necessary to switch to debt funds as we near our goals? Is there a debt option in diversified equity funds or we have to switch to a pure debt fund?

Hi Manoj

Yes, you are right. Two to three years before reaching your goal you must start shifting your funds from equity funds to debt funds in a systematic manner. You can consider pure debt funds or debt oriented hybrid funds. Bank fixed deposits can also be a safe option.

Adding my two cents:

Yes it is recommended that we switch from equity once we reach a goal or are near our goal. (Time limit of goal does not matter-it can be 3 years or 15 years). Rational being we should have the money when we need it and equity is volatile. It should not be that we wait till last moment and the market crashes. The purpose of investing in equity will then be defeated.

Now we must not forget that this is a thumb rule. Incase the market is rising we can wait assuming we understand the risk involved..and have control on our greed.

How do we take out the money?

There are various ways: a) Lump sump: Redeem the entire amount and invest in a assured debt option such as FDs b) Systematic Withdrawl plan: where you can redeem units systematically c) Systematic Transfer Plan : where you can transfer to debt fund of the same fund house.

There is no black and white answer as to which one to choose : As Hemant says It depends . Yes it depends on your risk profile, your comfort level with risk, your investment style.

Hi Kirti

For meeting short term goals investment in equity mutual funds is not desirable.

For long term goals of around 15 years review your portfolio after around 12 years. If you have accumulated the corpus needed, it makes sense to curb your greed and withdraw a substantial portion and put it in safe instrument like bank fixed deposit. The remaining amount can be withdrawn systematically over a period of three years.

Sir, i have joined u a few days back and started receiving ur posts. To read ur articles i looked back at my investments and their health. Very knowledgeable articles one over the other from u.

Thank you very much.

Thanks Jayant 🙂

every day a new scam inflation is too high also recession in economy do you still think some body should invest in market my monthly income is 35k god i’m investing 15k pm in mf through sip now a days i’m very much worried i’m 32 years old can take risk also pl suggest what should i do mf or ppf and fd. . . .ans please

Hi Sushil

In financial planning asset allocation is the most important thing. Have proper diversification to spread your risk. Don’t put all your eggs in one basket. Typically your asset allocation can be 30% in debt instruments like PPF and Bank Fixed Deposits, 60% in a portfolio of diversified equity mutual funds and 10% in gold.

Don’t worry. You will ultimately benefit in the long run by remaining invested in mutual funds through SIP route. Only by your remaining invested in equity mutual funds now can you hope to get inflation beating returns later on. Don’t panic.

Hi,

I have doubt about tax calculation on Mutual fund redemption.

Used this question for Post.I think that this will solve my confusion.

Regards,

Shailesh

Hi Shailesh,

I am writing an article based on your comment.

HI! Hemant,

These are my invesment details of SIP started from Jan-2011

1)Reliance Regular Savings Fund – Equity Option (G)–>500/-(started from jan-2011)

2)HDFC Prudence Fund –>4000/-(started from jun-2011)

3)HDFC Top 200 –>1500/-(started from may-2011)

Request your suggestion on the above portfolio.My view is on coming next 5 year..

Regards,

Anirban Goswami

Hi Anirban

Please read the post- Best Mutual Fund For SIP.

Hi Anirban,

Replace HDFC Prudence with one mid cap & another debt fund. Yes, I am saying you should stop SIP in your best performing fund.

HDFC Prudence works on asset allocation model with 65% in equity – my suggestion is you should develop your own asset allocation after considering your risk appetite.

Hi,

Can u please explain tax implications on equity mutual funds & whats the weightage that’s to be given for taxation while selecting a fund??

Regards

Harika

Hi Harika,

Taxation is a very important think while selecting an investment instrument – mutual funds are very tax efficient. I am writing a post on the same.

Dear Hemant Sir,

please tell me about the investment in NAV guaranteed plan

Thanking you

Hi Manik,

IRDA is planning to ban such products – I hope you got your answer.

Dear Hemant,

Can you help to 30,000/Month investment for sip. what will be my fund. My favour is lik thsis hdfctop200,hdfc equity,idfc premere equity,icici dynamic ,icici discovery and dspblackrocktop100.

Please write me your optionds.

regards

logan

Hi Logan,

You should check this

https://www.retirewise.in/2013/01/best-mutual-funds-to-invest-in-2013-india-top-schemes.html

please give me a suggestion about that in which category, I have added the Exchange Traded Fund (ETF) and why?

How to start a SIP and where

Comments are closed.