Do you want to reduce your capital gain tax liability on Property transaction?

If yes, then this article is for you!

What is Capital Gain?

Profits or gains arising from transfer of a capital asset are called “Capital Gains” and are charged to tax under the head “Capital Gains”.

Image courtesy of iosphere at FreeDigitalPhotos.net

Types of Capital Assets

- Any Property

- Any security

- Jewellery

- Archeological Collections

- Drawings

- Paintings

- Sculptures

- Any form of Art.

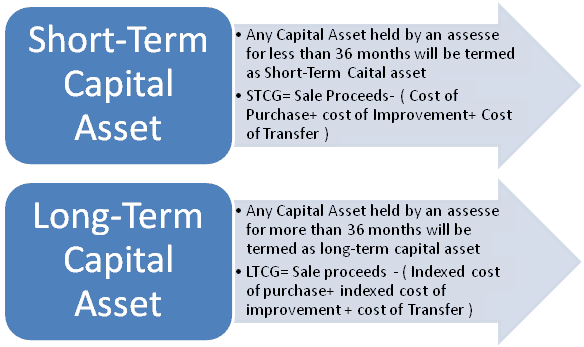

Types of Capital Gains

- Indexed cost means the inflated cost of the asset which is taken out by dividing the index number of year of sale and index number of year of acquisition of the asset.

- LTCG stands for Long-Term Capital Gain and STCG stands for Short-Term Capital Gains.

- Indexed cost also stands for Adjusted for Inflation.

Read: Cost Inflation Index (CII) How it impacts Capital Gain Tax on Real Estate & Mutual Funds

What is Capital Gains tax on sale of property?

The Income Tax Department imposes taxes on capital gains. These taxes are capital gains tax. If a property has been owned by you for less than 3 years and you have sold it, short term Capital Gains tax has to be paid else the terms of Long Term Capital Gains tax have to be applied. Short Term Capital Gains tax is paid as per income tax slab that one falls under. Long Term Capital Gains tax is set at 20%.

How do I save Capital Gains Tax from sale of Property?

- Section 54 : Old Asset : Residential Property, New Asset : Residential Property

Any long term capital gain arising from sale of residential house property shall be exempt to the extent such amount of gain is invested in

- Purchase of residential house during 1 year prior to or 2 years after the date of the transfer of property.

- Construction of residential property within 3 years from the date of transfer.

It may be noted here that with effect from 1st April, 2015, such investment can be made only in one residential property located in India.

If the new property is sold before expiry of 3 years from the date of acquisition/construction, then for the purpose of calculating capital gain for such property, the cost of acquisition shall be reduced by the amount of capital gain exempted earlier.

- Capital Gains Account Scheme:

In case, the new property could not be acquired/constructed before the due date of filing of return for that year, the amount sought to be invested can be deposited in Capital Gains Account with any authorised bank. Generally, most of the public sector banks are authorised under the Capital Gains Account Scheme.

Note that the amount so deposited shall be eligible for exemption as if it has been utilised for purchase/construction of new residential house property, however, if any amount so deposited, remains un-utilised at the end of 3 years from the date of transfer, it shall be chargeable to tax in that year.

- Section 54 EC : Old Asset : Any Asset, New Asset: Specified bonds

If you have sold property but do not wish to invest in another property soon, you can invest in bonds issued by National Highway Authority of India (NHAI) or Rural Electrification Corporation (REC) to save capital gains tax. You can invest up to Rs. 50,00,000 in the bonds within 6 months of date of sale of property. The bonds must not be sold up to 3 years from the date on which property was sold. It has to be noted that you should invest before the returns filing date if you wish to claim exemption in that financial year.

Kindly note, please make use of this benefit before the return filing date. If the amount is not invested, then it is included in the taxable income.

- Section 54F : Old Asset: Any Asset, New Asset : Residential Property

Wondering about how to save your tax if you have any asset other than residential house? There is Section 54F for you. J

Secton 54F : Section 54F states that any gain realizing from the sale of any long-term asset ( Apart from residential asset ) shall be fully exempt if the entire net sales is invested in purchasing of 1 residential house within 2 years or before 1 year from the date of such transfer OR the net consideration is invested in construction of 1 residential within 3 years after the date of such transfer.

Pro-Rata Exemption: If full consideration is not invested into the aforesaid options, then exemption would work on a pro-rata basis. The formula for the following is:

Amount exempted= Capital Gain X Amount Invested/Net Sale consideration.

Kindly note, at the date of such transfer the assese should be in possession of not more than 1 residential house apart from the house that he is investing his capital gain into.

Read: Mutual Fund Taxation in India

What if you have loss in selling of a property?

Things does not always work out according to the pans. If you end up in loss after selling your property, then that Long Term Capital Loss (LTCL) can be set off from long term capital gain ( LTCG ) arising from sale of any asset ( apart from gains arising from sale of shares, mutual funds etc on which STT has been paid ).

If the capital loss cannot be fully set off in that particular financial year, then it is allowed to be carry forward for 8 years but should be set off under the same head only.

Sir,

If I sale 1st Home (residential) and pay the home loan of 2nd Home (residential), May I claim it under section 54? Which ITR I have to fill? If it is LTCL, in which ITR form, I have to set off the losses? only showing in ITR form during return is enough or I have to declare it else where?

Manirul,

Yes that provision is available but the condition of purchasing a new house have to be fulfilled. This means you should have purchased the house within one year before the selling of your 2nd home or within 2 years after it. if its a construction then too the condition of sec 54 should be met.

I have finalised to sale a open plot which I have got from my father after his death.It had been on my name for last 11 yrs.So what are the options to save the capital gain tax from it.I am not planning for any purchase of residential property in near future.I am keeping the sum for higher education of my kids,which I may require in 2-3 yrs.

Raj K,

If you are not utilizing the proceeds for buying another house then other alternative is investing in capital gains bonds under Sec 54EC. You can invest upto Rs 50 lakh in a financial year and these bonds are for a period of 5-6 years.

However as you have mentioned that you need money after 2-3 years then you may not be able to utilize the tax exemption as any alternative for it will have a lockin of minimum 3 years.

superb article , keep it up !!

as usual a nice article where many needs updating.

Sir,

I have three residential properties on my name.

I will sell one of them then can I invet the long term proceedings arising from sale of one property to buy fourth residentail property.

As per section 54 : “It may be noted here that with effect from 1st April, 2015, such investment can be made only in one residential property in India”

As I have already three properties, Can it be possible to claim long term capital exemption?

Dear Sachin,

No, You can’t claim exemption as Exemption is available only if the taxpayer does not own more than one residential house on the date of transfer of such asset other than the one that he has bought to claim a deduction

Dear Sir,

My father had gifted a property 4 years ago. I had sold that property within a period of 6 month after it was registered in my name. As advised by our consultant, I have opened a capital gain account in a nationalized bank and deposited money in that account, but due to some problem I could not utilized that money to to buy new how. My question is :-

1. Is gifted property by parents attract capital gain or not?

2. If not invested to buy the property then in 3 yrs is this attract tax?

3. Any other alternatives to get the exemption from the tax part

Dear Mr M K,

1. Yes gifted property also attract capital gain tax.

2. Yes If not invested to buy the property then in 2 yrs or construct 3 yrs attract tax.

3. Hence it’s too late so now there is no alternate to get the exemption from the tax part.

I bought a residential property X in 2006-2007 for 22 lacs. I bought another residential property Y in 2012-2013 for 19 lacs. Now I want to sell property X for 170 lacs in 2016-2017 out of which the long term capital gains is 125 lacs so can I invest this amount to buy another residential property to save tax?

Dear Parag,

Yes you can invest this amount to buy another residential property. But you have to buy another property within 1 year to the date of transfer of the property.

I have sold my house in may2016 for Rs.17lacs which was purchased on 05/01/2005 for Rs.6.25lacs & paid furthur 3lacs for repairing,furniture & fittings.At present I am living at mumbai in a house owned by my son & daughter in law.Can I pay this amount to my son for purchase of a portion of his house for payment of his housing loan from SBI to save capital gain tax or invest in 54EC gapital gain a/c for 3yrs.& pay him later

Dear Mr N K

Yes you can do this. If u have deposited that amount in capital gain a/c for maximum 2 years if u are buying and 3 years if u are constructing house.

Suppose I have two house properties. Say first is self occupies and second is given on rent. Suppose I sell the second house property after 36 months after purchase. Can I avail long term capital gain tax exemption? I understand long term capital gain tax exemption is available only for the first house.

Dear Stany,

You can’t avail tax exemption. You can buy another property or capital gain bonds to avail tax exemption.

Hi Sir,

I am Chinnappa P B . Selling my house in my name of 18 year old ( expecting 2 Crs) & wants to invest in a good commercial property with in 2 years where the tenants will occupy for at least 5 to 10 years. Request your inputs on the following.

1. Can I deposit the sale proceeds amount dividing 50000 each in mine , wife & 2 sons name of bank S B a/c to save OR reduce the I T on interest.

2. Capital Gain bank A/c scheme 1988.

Property in my name sold & can I deposit the sale proceeds amount in 4 name of a/c to save OR reduce the I T on interest.

3. Do you suggest getting the property Registered jointly with my wife name before sale of property to save OR reduce the I T on interest.

4. Finally I am 54 years & left the job. The income from property is the only means of my living. My 2 sons are studying in final year graduations.

Suggest me if any other options best for me to invest where the value of money not depreciated over next 10 years & passed on to my sons later.

I am obliged for your valuable inputs & suggestions Thank you & warm Regards

Chinnappa P B

Dear Mr Chinnappa,

the only option that u can exempt from LTCG Tax is to buy a residential property or by investing that sale proceeds in a specific category of bonds that can exempt u from LTCG Tax.You should also consult to a good financial adviser before taking such decision.

Hello Sir,

I am selling one residential property in Feb2017 for 62Lacs which i purchased in 2005 for 13Lacs.

I have purchased another property in 2012 for Rs. 63Lacs. I have home loan of approx 40Lacs on this second property.

1. Hope I can repay home loan using amount i am getting from 1st property selling.

2, My issue here is – this 2nd home is small in size (in city) and i am planning to sale this 2nd home as well in next 3-4 month and planning to purchase new property

How the capital gain tax will calculated in all this scenario. Kindly suggest.

Regards

Sir,

I am having a residential property acquired in 2011-12 and held in my name only. Now I want to sell it and invest in another house where I will be first holder, my wife will be second holder and my son will be third holder. I will be investing whole of the capital gain in new property. Other holders will not be investing at all or may be small amount.

Kindly tell whether it is permissible to have new property in joint name to get capital gain exemption.

thanks..

Dear Mr Garg,

Yes you can buy new property in joint name & there will be no capital gain tax. I think it’s 54F but still, suggest you consult with CA.

Dear Sir /Madam,

Thanks for your valuable article on how to save capital gain tax on sale of land.

I purchased a piece of vacant land in urban area in 2005 through registered sale deed. The registration value of the land was Rs 2 lakhs.

I requested the authorized valuer of IT Department to make present valuation of the land. He has reported that the valuation of the land is Rs 40 lakhs as on March 2017 due to its nearness to State Highway and construction of a number of houses near the said plot.

If the said land is sold now for Rs 40 lakhs, kindly enlighten if the value of land will be taken as Rs 2 lakhs and indexed or it will be taken as Rs 40 lakhs for calculating the long term capital gain tax. If possible kindly quote the relevant rule/ section of ITAct/Rules, if any, according to which valuation made by the registered valuer of IT Department is acceptable / not acceptable to IT Department.

Yours Faithfully,

S Patel

Hi S Patel,

There will be 20% tax on the gain from sale of property & to find out the acceptable value of IT department contact your CA. The purchase price will be considered Rs 2 Lakh but you will get indexation benefit.

sir i have purchased flat in nagpur in july 2014 for 35000 rs AND I HAVE PADI 2.63 LAKH FOR STAMP DUTY AND THEN I HAVE DONE FURNITURE COSTING 12 LAKH RS (BUT NO BILLS AVAILBLE ) AND NOW I AM GOING TO SALE THIS PROPERTY FOR 70 LAKH RS , HOW MUCH TAX WILL I HAVE TO PAY?

Hi Dr Sunil,

Please consult a CA.

sir, i sold my property in march 2017 and deposited 33lakhs in NHAI in august this year as i was not sure about buying any residential property. its been only 3months but now i have decided to buy a property,can i get my deposit back from nhai ?

Hi Inder,

I am afraid – you will not get that amount.

Dear Sir,

I’m going to sell a residential building which I purchased in 2009.

Even I hold one more residential flat on my name.

I’m getting capital gains of 18 lakh, and I’m going to buy a new flat with full sale deed consideration, do I need to pay capital gains tax, or it is exempted under section 54.

My tax consultant says exemptions don’t apply when I have more then residential property.

Please advise me. Thanks in advance.

Regards,

Anil Kumar Akula

Dear Mr Anil,

Yes your tax consultant is saying right.

If you have only one residential property that you are going to sell than there is no need to pay tax on capital gains if u r buying another residential property from the sale proceeds.

Hi Sir,

I am selling a property which is in my name and now I want to buy a property in my wife’s name utilizing that capital gain.Can I show that as a re-investment in a property, thought am buying it in my wife’s name? And my second question is should I open a capital gain account to receive the amount arising out of the sell of my property or savings account will do as am buying the new property immediately say within next 1 month.Please help. Thanks.

Dear Dillip,

Yes you can get exempted from LTCG tax If u want to buy property on your wife’s name and that property must not be transferred to someone else name for next three years.

No there is no need to open any Capital gain a/c if u are buying property within 6 months of sale proceeds.

Sir, my mother has brought a vacant land in Bangalore in 1995. All most 22 years land.

Now we have sold the land for Rs. 30,00,000/- to one of the purchaser on 12th Sept 2017. My mother age is approx 55 – 60 years. Please inform whether we need to pay income tax. if my mother divides the amount equally to my sister and their daughters whether we need to pay tax or it will treat as gift. Also please inform how to exempt tax.

We are very poor and trying to sell land for my sister daughters marriage of 2 siblings.

if we gift the amount for them equally whether it is exempted from income tax. Please help us.

Dear Mr Deepu,

Yes your mother have to pay long term capital tax on the property.

Dear Sir,

My query is,

I have purchased house in January,2018 and Going to sell my existing house in May,2018.

In the above case Financial Years are different.

I am not sure that “Purchase of residential house during 1 year prior to” is applicable within same financial year or It is Up to Full 1 Year irrespective of financial year.

Please clarify. Thanks in advance.

Dear Mr. Hemant Beniwalji,

Your article and replies are exhaustive and highly informative but I need to know my query as it is not covered above threads. I have a property in Delhi. I am intending to sale a part of it and build a house on the rest of the area (by demolishing the old structure fully).

The plot was bought in 1971 & the house was built in 1985 (no proofs/receipts of expenses on construction is available with me now). My queries are:

1. How will the LTCG be affected and will I get any benefits for this construction?

2. What proof does the IT dept need for the new construction part(as the same builder will do both i.e. buy, register his part and construct new for the same amount, no money being given or taken)?

I hope you will resolve my issue and advise as early as possible since your all advice are quite exhaustive and prompt in guiding in resolving LTCG issue. If possible kindly email the response or inform when the reply is put on your blog. I am a senior citizen, if that is relevant. Thanks.

With best regards,

Dr. Goswamy

Dear Dr. Goswamy,

Please consult a CA.

Sir,

My query is,

I have purchased house in January,2018 and Going to sell my existing house in May,2018.

In the above case Financial Years are different.

I am not sure that “Purchase of residential house during 1 year prior to” is applicable within same financial year or It is Up to Full 1 Year irrespective of financial year.

Please clarify. Thanks in advance.

Residential plot bought in 2009 a @22 lakh. Now want to sell same @ 85 lakh & use this fund for buying either a Residential plot or agricultural plot.

Will it make me exempted from LTCG TAX.

Dear Mr A M,

Yes u can get exempted from LTCG TAX if u buy a residential property from the sale proceeds but that must be the only residential on your name.

Dear sir,

I am having one old house constructed in a rural village in the year2010, i purchased one aptment on April2017 with home lone and EMI payable from my pension. After selling of land property i purchased another apattment inDecember2017. Now i am need to purchase another Apartment. Can i purchase sir, pl guide me.

Dear Mr Seshavadhani,

As u said u are paying EMIs from your pension that means u are a Retired Person and Retirement means financial freedom. I think during Retirement 1 House is enough for you and if u want to invest your additional money than there are many options available for that. Consult any Retirement Planner before taking such investment decision.

Dear Sir, Please reply to my query

My query is,

I have purchased house in January,2018 and Going to sell my existing house in May,2018.

In the above case Financial Years are different.

I am not sure that “Purchase of residential house during 1 year prior to” is applicable within same financial year or It is Up to Full 1 Year irrespective of financial year.

Please clarify. Thanks in advance.

Dear Mr Swapnil,

Yes you can get exempted from capital gain tax because “Purchase of residential house during 1 year prior to” is applicable within the 1 calendar year from the date of sale.

Dear Sir ,

Thanks so much for your valuable article ,

My Father bought some land in 1990 in 2 Lakh and build the House on that (approx 40 Lakh invested in construction)

Now he is selling that in approx 1.8 Cr.

Question is

1- During Capital gain calculation amount spent in construction (apprx 40 lakh) will be also considered?

2- Since it is approx amount we are thinking we spent in construction, what is way to prove yes we spent apprx 40 Lakh that time in construction(Incase IT dept ask proof) ?

3- Suppose capital gain is 80 Lakh is it possible he can invest 50 Lkah in one financial year for any capital saving bond and rest 30 Lakh in another financial year , any loophole in this ?(I am aware that he need to invest all money within 6 month of sale, so if he sales in dec month so he will be investing 50 lakh in dec 2018 and 30 lakh in april 2019, is there any issue in this ?)

4- is there any rule form govt. that maximum a person can invest any certain amount of money in capital gain saving Bonds example life time limit is 1 Cr. or so on ?(Note I am aware each financial year limit is 50 lakh i am asking for max limit a person can invest in his/her life time? )

5- after 3 year when this bond will mature and my father withdraw money, will that money will be taxable at that time or only interest earned is taxable ?

Please suggest sir

Thanks so much

-AP

Dear AP,

Please Consult a CA.

Hi

I sold residential property in sep2016 for 20 lac. I dont file IT return since my income is below 2 lacs. how can i save LTCG on this. Please need your advice. Thanks

Dear Sir,

Please consult a CA for better advice.

Sir.

I have purchased a flat in three names myself my wife and my son. when I am selling the flat the selling amount have to be shared by three persons. And hence the Long term capital gains is to be calculated only on my share of the selling price?

Can I purchase father’s own house by capital gain

Hi Sir,

Can the capital gain from seling of a house be invested in buying a residential plot? or I have to buy a house against a house?

Looking for some expert advise.

You have to buy a house.

We have sold a land parcel on 21st January 2018 and planning to buy a flat by March 2019 as waiting for completion certificate from PMC. Calculated Capital Gains amount is 32 laks. We have parked this amount in the Capital Gains account in Nationalised bank.

Can we save a long term Capital Gains tax if we buy the flat by end of this financial year for around 60 laks ( Including the registration and stamp duty taxes) . Or we have to do the agreement before 21st January 2020 only ?

Dear Abhay,

As per my knowledge, you have to buy the flat before 21st January 2020.

Comments are closed.