Steven R. Covey was one of the most respected business writers, he passed away this year (16

th July 2012) but

he left a treasure of wisdom that will drive mankind in the right direction for generations to come. He wrote a self-help book

“The 7 Habits of Highly Effective People” in 1989 which features in the list of “The 25 Most Influential Business Management Books” by Time Magazine. This book gave birth to cult of business management books – just imagine the numbers, 2.5 crore copies in 38 languages are sold till date. The 7 habits that he highlighted can amalgamate into any field. Bill Clinton once invited Covey to help him connect the 7 habits to his presidency.

Let’s try to place these habits in finance field & achieve success in our financial lives.

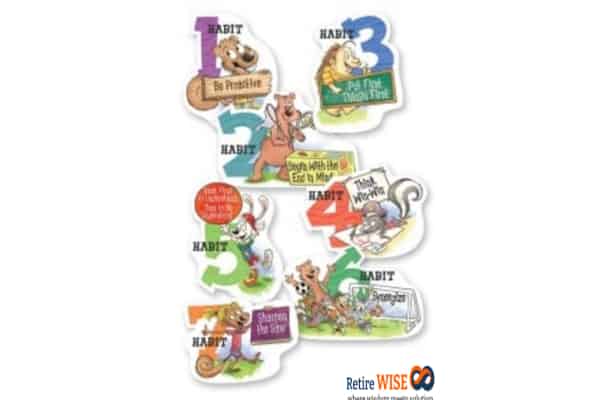

7 Habits are divided in 3 parts

I. Independence or Self Mastery

The first 3 habits talks about moving from Dependence to Independence

II. Interdependence

Next 3 habits will be interdependence or where we can work with others

III. Self-Renewal

The final habit relates to self-upgrading

")

Awesome explanation, keep up the good job of sharing knowledge:)

Thanks Akash.

Really very interesting to read the article and 7steps are very real in common life to be followed but many of them cannot do as it is difficult when it comes in practical life so people success in financial plannings are less. I cannot understand about synergy, could you please explain in detail.

Hi Vandhana,

Synergy is when 2 brains are applied on the same thing – outcome can be much better than 1+1.

Amazing post Hemant …

The way you enlighten your reader is exclusive and supportive to their financial lives…

Wish u n everyone Happy New Year ahead …

Thanks Satya & I reciprocate the same.

Lovely message, quite useful…its like a gift on Christmas 🙂

I’ve read Stephen R.Covey’s book 7 habits of highly effective people. Also I’ve read material wherein people have used the 7 principles to explain different subjects. Though I never came accross any article on this subject.

Great way to explain the 7 principles.

Could you help me understand the last point in a better way ? I understand that we should work on our skills time to time but which skills, what knowledge should be enhanced regarding finances ? Do you mean its enough if we keep a check on what planning we have already done and to see that we stand by it in any circumstances ? Or something else… please elaborate

Thanks.

Hi Nishi,

Yes we have to keep learning new things – even in any professional course requirement is continuous education.

very nice.

Thank you Hemanth. What is synergies?

Typo

These are real gems.

Thanks Anil 🙂

What a great chart this is! I especially love the point about being proactive and it is something where I lack quite a bit as well.

Many times others give me ideas that I feel I should have thought on my own, and have executed on as well. I think all of us should block some time every day to just sit and think without any distractions and focus on ideas to improve, just improve anything, any aspect of our life, or someone else’s life.

Thanks a ton Manshu – What I like about you is that you have no hesitation in sharing your weaknesses – I think this is a strength.

Hope that you will take some proactive decisions next year 🙂

excellent article, Hemant !!! great New Year gift to all your readers. I liked the 4th habit- ” think win-win” — clients need to understand that financial planners don’t work on charity basis, so better to have clear expectations upfront. Once the client understand that it is in his own interest to have a fee-based planner, rather than the so-called “free services Planner” , half the battle is won. Also about the “synergy” habit, I am not so sure–this will work in cases where the spouse is also interested/ financially literate, in many cases the spouse has no interest whatsoever , so this may not work out. In such cases, the “synergy” aspect would result from discussing with good friends/tfl website before investing.

Thanks Shreedhar – even if spouse is not fin lit she should be involved at some level – may be deciding goals because its not about my dreams its about OUR dreams. Happy New Year 🙂

of course, on this count I totally agree with you– not only should the spouse be involved in goal-setting, but should also be aware abt the investments made. What I meant was that the spouse might not be interested in knowing about the asset allocation and the road map to achieve the goal.

Some husbands don’t even consider talking them with spouse. They are just too old fashioned to think that they need not be shared. But with the present uncertainty and growing living in relationships, how much to be shared? Even your lines say “at some level”. Parity in goal setting or road map can be a point of family dispute. Then how much and at what point?

Rama

Why to blame the partner? Let the “E” “go”. The partner who loads the burden of earning / savings will take that. The other should give peace of mind.

It’s really knowledgeable.

May we get some guidance sector fund to be invested during the coming year.

Regards

Vishnu

Dear Hemant

Wish you a happy new year 2013.

You explanation is so good, even a person who taking wrong decesion on fianance will think twice before proceeding whether to go ahead or not. It is real very nice and I have told many of my friends to go through your advice.

I request give you advice on insurance policy for housing loans and children plans

Thanks

padmaja

Hello Hemant,

It has been little over a couple of months, I have been going through your articles. I must say that these are really very practical and inspiring ones (yes, you get inspired to follow/create a well-planned financial path !). I will surely take the first step of my ‘financial-planning’ this year, though I realise that it’s little late for me at this point of life.

Keep spreading the good-wisdom and keep things simple yet so effective for your followers.

A very happy new year to you and your team.

Regards,

Prashant

Hi Prashant,

Motivation is what gets you started; Habit is what keeps you going 🙂

Thanks Hemant.

I will take care of my ‘motivation’…… and you/your articles will take care of my ‘habit’ 🙂

But I will prefer other way round.

Dear Hemant,

can you send me personality development and leadership building

jeppi

Thanks a lot for such a nice sharing.

swarna kalash new gold scheme offer by surat diamond and reliance monthy pay 12000 first and 2000 monthly for 3 to 10 years and get gold coin after that, pls inform this scheme is good or not

Nice article

Amazing post Hemant …

Really like it.. dil se

Comments are closed.