Equity Linked Saving Schemes popularly known as ELSS funds are still struggling in the Indian market to establish themselves. Many investors, who are afraid of the equity market, choose life insurance or Provident fund to save tax. These products are few decades old and are very popular among Taxpayers. However, due to increase in the inflation and lower returns, these products are losing their market share. Investors are now looking for those products which offer growth in the long term and helps in wealth creation. ELSS is one such product which offers both, but due to the risk/Volatility associated with the product, people hesitate to invest in it.

I am firm believer that “confusion is the first stage of solution” –

so let me try to confuse you through this post 🙂

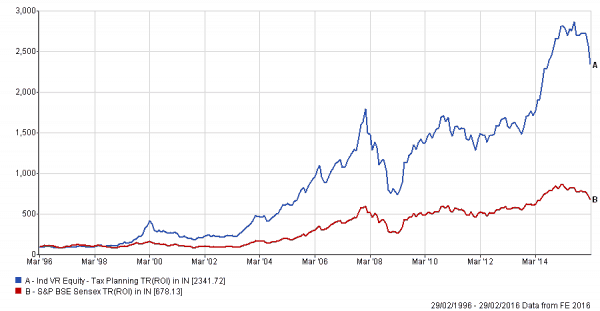

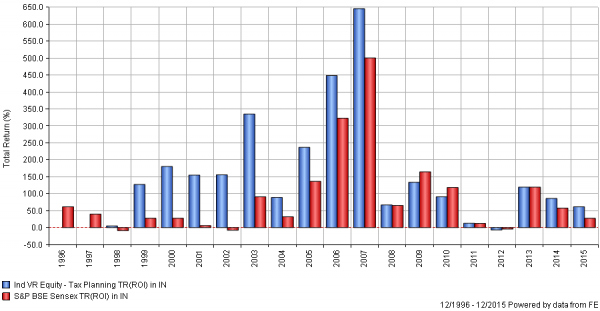

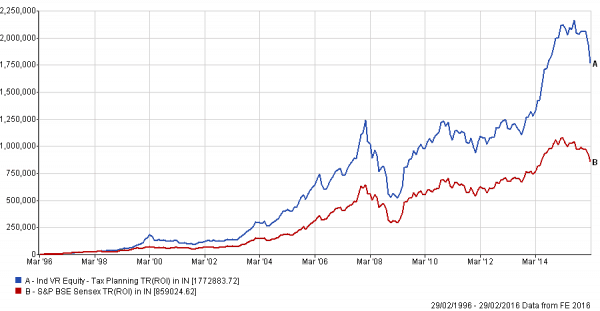

Chart – ELSS performance – 23 times or 2300% in 20 years

Few question before investing in ELSS

For a longer duration, any product which generates returns over and above inflation is good for investor and in the category of tax saving instruments, ELSS funds are best in the lot till date. But are these funds always good for an investor? Does this fund suits every category of investor? Are these funds successful in generating good returns in the short term? Have you ever thought about these questions while investing or just invested because you need to save tax? Let us today try to focus on above questions and find out which category of investors should avoid these funds and also in which situation one should stay away from ELSS funds.

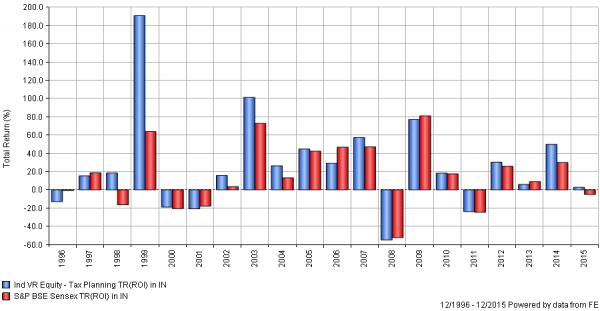

ELSS 1 Year performance – rolling return

Rolling returns display returns in overlapping cycles of any specific frequency – going back as far as the data we have available. The goal is to show you the frequency and magnitude of an investment’s good and bad performance periods.

Must Read – Best Tax Saving Option ELSS Vs PPF

Think Before you invest in ELSS funds

Post Retirement

All those investors who are senior citizens or retired and are looking for the investment schemes should try and avoid ELSS funds as tax saving tool. Post retirement is a phase where one should look out for those schemes which offer both liquidity and tax saving with fixed returns. ELSS fund comes with 3 years of lock in and is highly risky if you don’t understand volatility. Also, as there is no guarantee on returns, there are often chances that investor may lose the part of its capital. [we suggest even in retirement people would have decent exposure to open-ended diversified equity mutual funds based on risk profile & requirement – but after understanding risk associated with that]

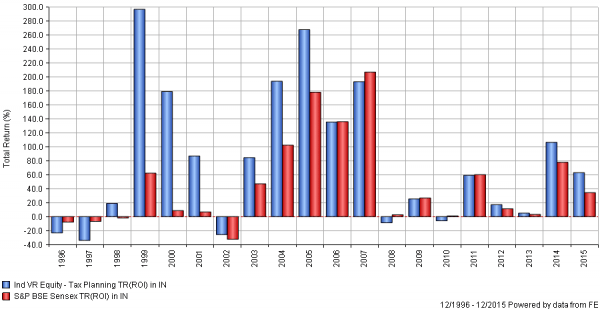

ELSS 3 Year performance – rolling return

Investor’s Risk profile is conservative

If an investor’s risk profile is moderately conservative then he/she should not invest in ELSS funds, as these are highly volatile and does not guarantee returns. The conservative investor always looks for growth with security and a slight decline in portfolio makes them worried. So, they should look at other tax saving products which are less volatile and should ignore ELSS funds. [we may also suggest that if you are conservative investor & literally hate equity & volatility – this year add some amount in ELSS]

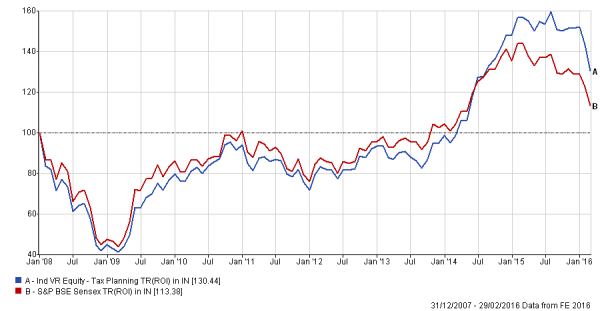

Rs 100 invested in Jan 2008

Investment horizon is less than 5 years

If an investor has a goal which is of less than 5 years then he/she should ignore ELSS funds as a part of equity investments. These funds have a multi-cap portfolio which invest aggressively into small and mid-cap and thus bears high risk. Ideally for a period of 5 years for equity one should only consider large cap fund which are less volatile than ELSS funds. [saying 5 years for equity funds doesn’t mean that it will not be negative if you hold for 5 years]

ELSS 5 Year performance – rolling return

Investing at the end of Financial Year

Most of the time people look for tax saving products only during last quarter of the financial year. It is the time when they (Employees) are forced to submit their investment details and thus in a hurry they invest in ELSS in lumpsum. Ideally, this is the wrong way to invest in ELSS. One should always plan their tax related investment in advance and invest through SIP mode in ELSS to get the benefit of rupee cost averaging. [it’s not about performance but discipline]

Saving Frequency: Monthly ● SIP Amount: 1000.00

Total Investment: Rs 2.41 Lakh ● Current Value: Rs 17.7 Lakh

What should you do?

To conclude, investors should avoid ELSS funds if they are looking for short term and are not comfortable with equities. However, one should also keep in mind that ELSS funds are not at all bad. In fact, ELSS is the best tax saving option available in India but only for those who are looking for long term and have the capacity to digest volatility. And for rest National Saving Certificates or Tax-free FD or PPF would be better as these are less risky (without considering inflation) and offer fixed interest. [if your income is less must invest some portion in ELSS for tax saving]

Let me share not a single client of our’s use ELSS for tax saving – in most of the cases 80 C is exhausted in EPF, home loan & term insurance premium. So, how do you invest in ELSS funds? Do you agree with the above points or have some other views? And if you are confused – add that in the comment section.

")

How to become your client

Dear Indranil,

You can leave your contact details on this link

https://www.retirewise.in/services/financial-planning-services

As usual a well researched and thought provoking article. I have only one issue. It is absolutely poor advice to do a SIP in ELSS funds. Each installment gets locked in for three years and hence it makes no sense. I have always used the lumpsum route and believe me the results have been outstanding.

That’s true Japesh but when we talk about equity we are talking about 5-10 or life-long investments. Lockin should not be an issue & if it is even any lumpsum that you invest on any date will be locked for 3 years.

u r absolutely right

We the indians are genetically wired with HERD MENTALITY.We must think individually for every decision in our life rather than going for COPY PASTE approach.ELSS is not the right investment all the times.

Agree Rajnikanth & this is not limited to ELSS. One should look at his requirement & then consider any investment.

I am retd person. Last 3 years I am fully utilising 1.5 lacs limit in investing ELSS e.g HDFC long term equity fund under direct dividend payout. In fact 1999-2000 onwards I subscribe to sundarm Elss where I had recd hefty dividends.However in 2006-07 when I smelled Lehman collapse/sub prime issue in advance I withdraw the same & kept in another folio. It is not bad to invest Elss. Only u have to keep track-ultimately it’s your hard earned money. For this exercise u r the ONLY person who can keep the watch on your investment & nobody else.

Thanks

Shrikant

Hi Shrikant,

You were lucky to withdraw in 2006-07 – good to hear about your conviction in equities.

I invest in PPF & ELSS ( 1.5lacs each) before 5th of April every year in lumpsum. I use ELSS as a Savings for LongTem Growth ..though Iam a Senior Citizen.

Great Dr MCS that you understand role of equity in long-term growth, please try to share your experience with young doctors who have no clue about this.

Thanks for the article on ELSS. There is another BIG (yes, really BIG) reason why a person invests in ELSS schemes. Of the 100’s of MF’schemes many schemes require one time investment of Rs.5000.00 followed by SIP of Rs.1000.00. Possibly ELSS schemes are the only ones which allow SIP with Rs.500.00 (Rupees Five hundred) without any First time lump sum investment. The Great Indian Middle class, sure will choose this route, for investing in MF’s at the minimum cost, though may not be for tax savings. Rs.500.00 seems small just like RD for them.

Hi Hemant

I am surprised to know that many senior citizens are investing in ELSS. I agree 100% with the points mentioned by you. I do not invest in ELSS. Personally I feel that most senior citizens have some health issues and it is difficult to predict how long they are going to live. If a senior citizen is healthy and is living an active life then he can perhaps consider investing in ELSS but if he has some health issues then he should stay away from ELSS.

Senior Citizenship starts from 60 & not every one is going to die at 60. I propose to die at around 85 God Willing ! I have a clear cut agenda to invest in ELSS & Equity Funds & I also actively trade in Equities & have been fairly successful in multiplying my assets. I will have Equities predominantly in my portfolio for some time to come. With falling interest rates, if Seniors bank on Debt instruments, they are doomed. Yes, one has to be cautious not give into gambling instinct. BTW no body can predict how long one is going to live. Even youngsters are dying everyday

I’m a government employee, started investing in ICICI Tax saver fund as lump sum in 2010 & got good return. Started sip in Reliance tax plan growth for Rs. 2000 in 2014. I think SIP is better to average the volatility of the equity markets. And if you have a 5 to 10 years or more time frame, then it becomes best tax saving cum investment option. Hemant sir, thanks for your good article.

Hi Hemant,

If we have stayed in ELSS for more then 6 years say HDFC TAX saver.Now looking to switch to other MF fund as current HDFC fund has given 9% returns only in 6 years. How to switch because on redeem I will get lump sum amount and I want to reinvest through SIP. In this case its like starting from scratch again to feel the power of compounding.If invested through lump sum,then risk comes ? please suggest

Dear Fergi,

It is not possible to invest in other fund house without redeeming.

Thank you for the insight on ELSS. I have a doubt that only two mutual funds are allowed to invest under ELSS or can we invest on more funds for tax savings??? Please help me on this.

With regards

Prasad

Hi,

I am 26 year old professional,i want to invest 10,000 per month through SIP in ELSS.

Could you please suggest some ELSS where i should invest.

I am expecting good returns and ready to bear risk. i want to invest for long term say 5-10 yrs.

sir,.

thanks for the trustworthy information provided . I would like to know , why and how to invest in elss if the portion in the 80C is already achieved. if there is no point in investing elss, what is the other option in mutual fund sector?

Hi Hemant,

Need some information.I plan to invest 1.5 lakhs in PPF and same amount Elss schemes from Axis, SBI and HDFC (3 year lock in period )So for Assessment year 2018-19 my investments under 80cc will come out to be 3 lakhs .

Please let me know if in this case the interest I earn from Elss for the period 2017-18 will be taxable or not.

Please reply.

Thanks

Hi,

I am 30 years. I earn 40-50 k per month. This year I made a lumpsum investment in 4-5 ELSS funds for tax saving. But I am planning to do SIP as well. Should I do it in ELSS or equity? Please suggest me the investment plan for a better future.

Hi Sharvan,

Consider 1 or max 2 funds

Hi,

Can you name them so that I can check their return percentage and performance over a period. Thanks in advance.

please suggest me any 2 best diversified elss fund to invest in december 2017 in 50:50 ratio for long term 15-20 years for retirement. I am 37 years now. I want to invest 80k in two diversified elss funds without any overlapping. I also want to invest around 30k in ppf also. whether it will be good. please suggest.

Hi,

I want to invest in an ELSS fund and would like to know about specific conditions for income tax exemptions via ELSS. How much of the investment would be tax exempt? For example, if I invest Rs. 60000 in the current financial year, would the entire amount fall under 80C exemption? Also, will the income be valid in case of exemptions above Rs. 12 Lacs?

My name is Anita earning Rs 1 lac a month. I had invested in PPF and SSA( 1.5 lac each) from last 3 years and LIC (50 K per year). Also I taken 4-5 SIP ( totally 10K per month in all SIPs). Now I am willing to invest in any long term SIP(ELSS). Please help me in investing in some good ELSS through SIP only.

Comments are closed.