LIC has a tradition of launching a single premium plan in the last quarter of financial year and it has kept it going. Amid the sea changes made by IRDA on traditional products from 1st January 2014, LIC has launched the first product – LIC Single Premium Endowment Plan, in compliance with these changes. The main reason of coming out with such a product in the last quarter of financial year can be attributed to the tax benefit which most salaried individuals seek to avoid high deduction from their income in these months. Due to this aspect, even the business of Life Insurance companies increase manifold and LIC too have always garnered a heavy collection with its single premium product.

But considering the change in the tax provision in Budget 2012 and the alternatives available to investors, is LIC Single Premium Endowment Plan or any other single premium product worth investing now? Let’s find out through this brief review-

Features of LIC Single Premium Endowment Plan

General: The new plan is a single premium endowment plan and so the premium has to be paid only once. On completing the required term the policyholder receives the maturity amount. Anyone from age 90 days to 65 yrs can invest in the product which means it can be bought for children/grandchildren too. It’s a participating non-linked savings cum protection plan so the policy will accrue bonus during the term. The benefit, which will include sum assured and bonuses declared, will be paid either on maturity or on death of the policyholder. The minimum term policy can be bought is for 10 years and the maximum term of the policy is 25 years. However, the maximum age of maturity is kept at 75 years which means a person with age of 65 years cannot buy the policy for more than 15 years.

Sum Assured: The minimum sum assured in LIC Single Premium Endowment Plan has been kept at Rs 50000 while there is no limit for maximum amount and it has to be in multiple of Rs 5000 only. As per IRDA new regulations, the sum assured in all traditional products has to be min 10 times of annual premium if less than 45 years of age and minimum 7 times if age of life assured is more than 45 years for all policy term greater than 10 years.

Read – LIC Jeevan Akshay – Pension Plan

Maturity/Death Benefit in LIC New Single Premium Endowment Plan

On Maturity, LIC will pay the sum assured along with the bonus accrued during the term of the product. The bonus declared in LIC Single Premium Endowment Plan policy will be simple reversionary bonus plus final addition bonus, if any.

The policy will pay death benefit differently at two instances:- If the death of the policyholder is after the risk commencement then sum assured along with accrued bonuses will be paid. But if the death occurs before the risk commencement then only the single premium paid to the company will be returned without any interest.

(In case the age at entry of Life Assured is less than 8 years, risk will commence either 2 years from the DOC OR policy anniversary after completion of 8 years of age whichever is earlier, for others risk shall commence immediately).

Surrender Charges of LIC Single Premium Endowment Plan: Since the policy is launched in 2014, it has to abide by IRDA new regulations. Hence the surrender charges in this product are in line with it. In first year 70% of the basic premium will be paid while any time after 1st year 90% of the premium paid will be paid as surrender benefit.

Read – LIC Wealth Plus Highest NAV Plan

Other Features

A loan can be availed from LIC which will be a defined % of surrender value. This option starts from 2nd year onwards and the loan value is higher in case the remaining policy term is lower. So for a term of 21 year and above if the loan is taken after completing 15 years, LIC can give upto 90% of surrender value.

The Return-IRR of LIC Single Premium Endowment Plan

Yes, this is the most important factor now to evaluate the product, especially after so many changes in life insurance from 1st January, 2014. Now all insurance companies has to show illustration on two assumptions – 4% and 8% investment return. One factor which all investors have to take in consideration is that this is return is on your investment amount i.e. net premium you paid after deducting the charges.

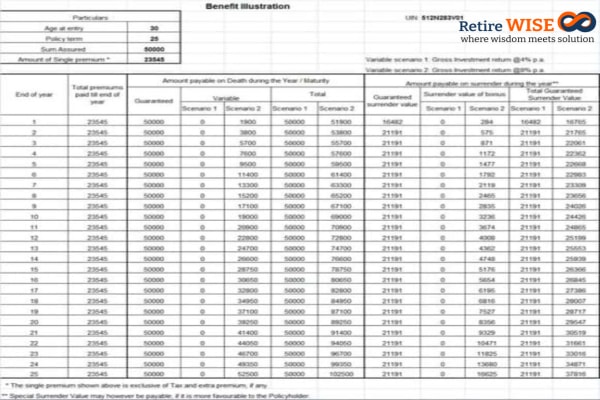

LIC Single Premium Endowment Plan – Illustration

I have assumed the figures based on LIC new Single Premium Endowment Plan benefit illustration at its website for a 30 year old. The policy term is taken as 25 years.

| Premium Invested (Rs.) | Bonus (Rs.) | Maturity Amount (Rs.) | IRR |

| 23545 | 52500 | 102500 | 6% |

The IRR of the product comes to 6% at 8% investment return shown by the company. Since there is no bonus illustrated at 4% return assumption, no IRR is calculated.

Alternatives of LIC Single Premium Endowment Plan

First let’s see what alternatives you have for this product if you want to invest one time:

- ELSS– Equity linked Savings scheme are market linked product and so it will not be wise to compare the net return of these two. But if investing for such a long period won’t ELSS be a more lucrative option considering thelower cost of investment and the returns it can generate.

- PPF– A PPF is also a long term investment and can be continued for 15 years. If you have one going then considering the higher rate of return and tax free status, it will be more lucrative to invest your contribution in PPF to avail the tax benefit and fetch higher returns.

- Tax saving FDs – not at all bad if we compare with LIC Single Premium Endowment Plan

Argument in favor of LIC Single Premium Endowment Plan 🙁

While I was looking at arguments in favor of the product I found the following three more common but interestingly they fails:

1. Family Protection– The first argument is the protection it gives to you for your family. But if you analyze your insurance need, the requirement is generally into lakhs or crore. The premium you will have to pay in this policy for such a cover will be way beyond your means. A term plan is far cheaper means to avail a higher protection. For e.g.to buy a cover of Rs 50 lakh for a 30 year old person, the premium in this product will run into lakhs while in a term insurance it will be range between Rs6000- Rs 10000 p.a. So it’s difficult to avail any high insurance coverage here.

2. Investment– I have shown clearly that the investment return will be way below what you can generate from other instruments. Although earlier death can produce higher IRR but then you make investment for wealth creation in your life and not for early death benefit.

3. Tax Benefit– The product will come under section 80C & Sec 10(10D). As per budget provision of 2012 the premium paid towards insurance policy will qualify for tax benefit only when the SA in a respective year is at least 10 times of the premium paid. If it doesn’t happen then even the maturity amount will not be tax free under sec 10(10D). The biggest losers in this provision are single premium policies which are not able to meet this criteria. If we look at the illustration alone, then this criteria is not met. Even the sample premium rates given by LIC at its website do not benefit either. If this is the case then you will loose any tax benefit on this product.

Thus, while analyzing on various parameters the single premium product launched by LIC does not fulfill either of the requirement- Protection and Investment. Hence, It’s good to avoid. The basic of financial planning says “keep investment and insurance separate’. Choose a term plan if you really want to buy high protection for your family but only after a detail analysis and weigh the investment options for long term instead of building your wealth from a combo product.

Review of LIC New Single Premium Endowment Plan is done by Jitendra PS Solanki, he is CERTIFIED FINANCIAL PLANNERCM and SEBI Registered Investment Adviser

Have you invested in any single premium plans? Were you aware of the tax provision of 2012? Have someone pushed traditional polices to you in last 2 months? Share your view in comment section & if this article makes sense share with your friends…

Sir i got two policies from Lic in july 2013….one policy is jeevan nidhi pension plan of Rs 1000000 (ten lakhs) and onother is endowment plan of Rs(500000) five lakhs. So tell me the benefits of these two different policies….i cant understand these benefits properly….. and how much i will receive the pension after my retirement…

Plz reply sir

this plan is not good

Hi Wasim,

In an endowment plan you pay the premium till the term and on maturity Sum Assured along with bonuses declared during the term will be paid to you. Sum Assured you would be knowing and bonuses will be declared every year based on the investment performance. So Bonuses is not assured.

On other hand Jeevan Nidhi is a pension plan where you will pay the premium for a term (called as vesting age) and post then you have an option of receiving the payout in the form of pension.The amount of pension depends on the corpus you are able to accumulate on the basis of bonuses declared in the policy.

The only issue with these traditional policies is the net return which is far lower than comparable long term instruments.

I hope this answer your query.

Sir, i cant understand your answer…my lic agent told me that you will receive Rs 1400000 on the endowment plan after maturity of the policy (after 25 years)….and on the jivan nidhi pension plan you will receive rs 23300 pension per month after retirement (after 34 years)… sir tell me this information is correct or incorrection….

Endowment plan policy amount is Rs 500000. and

Pension plan policy amount is Rs 1000000..

Plz rply the answer

Hi Wasim,

Can you illustrate the premium for both these policies?

Premium is quarterly both the policies total premium is Rs 12000 …

Hemantji,

Happy new year, You did a proper postmortem of said product. You being a financial planner your views are Ok. Being a LIC agent I will put my views, Single premium advantages.1. Grandfather can pay single premiums for their grand childrens, 2. Those who don’t have regular income and now they have ready amount they can choose this product for long term.3. Loan and surrender facilities are there. instead of 8% you indicated 6% returns ,Common man don’t play high risk investment products they see security. Very few people monitor their money in other financial instrument for long term, Not necessary their financial adviser always with them for guidance LIC ‘s track record shows their maturity amount or survival checks always dispatch in advance, now a days NEFT facility available. Most important LIC proves a trustworthy organaisation. Person to person our opinions are differ. Have a nice day sir.

Dear Vinod Joshi,

You are obsolutely right, your views and Hemant’s view are entirely different. You are thinking from an agent point of view on how to get someone committed to a policy irrespective of wheter it really benifits them or not?

Whereas Hemant here was explaining about how to choose a right policy with the right benifit and purpose in the long term.

For your kind information, most ELSS and Tax saving FD’s can also be invested one time and you will most likely double your investment in 6 -8 years of time.

Very comprehensive review & most importantly, clearly states whether this should be pursued or not, no ambiguity there!

Thanks Pankaj

It’s unfortunate if anybody considers insurance as saving/investment. You must consider as insurance as pure/term insurance. If IRR is 6% and inflation is 8% to 9%, just consider the devalation of money.

Thats clearly visible that single premium policy offered by LIC is not going to benefit customer either way. The major reason for buying insurance policy in last quarter of the year is basically is to avail tax benefit u/s 80C which this policy does not fulfil beacuse of S.A premium ratio. In single premium LIC plan, the customer needs to be aware of the tax implications or he might be mis sold on this front. It is not wise decision to buy this policy only because of returns that are also not very lucrative.

Is is better to purchase a regular premium insurance plan which will suffice the tax benefit need not only for current year but in future years also. Since the sum assure is 10 times of premium paid on high end, the returns are also high in long term as bonuses are declare as a percentage of sum assured. Also for young employed or recently married people this is the best instrument to inculcate good regular saving habit. Regular premium life insurance plan develops a habit of force investment cause you are bound to invest every year if you did it for first the year..

Computation of adequate risk cover is very necessary in current era due to various factors arising because of changing lifestyles. Methods of insurance cover calculation are available with qualified insurance agents. I say qualified because those agents helps the customers to buy the insurance plan by doing their need analysis and establish a long term client – agent relationship unlike many other who only knows how to sell and hardly show their faces after sale.

Dear Alankar,

Traditional insurance plans- regular or single premium fails to provide either of the dual benefit they claim i.e. insurance and investment. A more wiser approach is to look at insurance and investment seperately.

I am 33 years now and a having 3.3 yrs daughter. Invested in two different LIC policies and recently taken term plan, need your inputs whether to continue on the same or any change.

LICs:

1) The Money Back Policy – 20 years, premium 31,437/yearly, SA 5L, taken 04/10/2006

2) Jeevan Kishore (on my daughter’s name)- 19 years, premium 25,239/yearly, SA 5.2L, taken 23/11/2011

Term Policy: Aviva iLife – 35 Years, premium 5,590, SA 60L, taken 02/12/2011

Akbari,

Money back policies are the costliest among traditional plans and their returns are below inflation. Jeevan Kishore too is a traditional plan and so the returns will be lower. You should look at other investing options such as PPF and Mutual Funds for meeting your child goals.

Sir plz reply the answer of my question .

One quick query on surrender value of old policies (pre-2014). Would the new surrender value norms apply to those old policies or it is applicable only for new policies issued from 2014?

Venkateswaran,

The new rules applies to policies bought after January 1st, 2014.

Surrender Value affects the costing of the policy. The previous policies were designed as per regulations. The customer purchases a policy seeing the benefts offered to him at the time of purchase i.e. value of his money. Now it is difficult to offer higher surrender value in same cost (premium). So no change in previous contracts. New surrender value clause is applicable for new policies.

I am NRI from gulf, we all are covered by an insurance from the company that covers even critical illness like heart attack or long term disability. However, when we return to India after retirement, no one will offer insurance cover at 60 above to cover critical illness or long term disability.

I request you to suggest an insurance plan that we can take it at any age or say before 50 continue paying the premium just to have this cover.

or just let me know if any good insurance policy for the cover of critical illness for the full family of say 4 members- husband and wife and 2 kids.

thanks for your consideration in advance.

Hemant, Asusual one more useful document from you. I have recommended your posts to many of my friends. They are also so happy with me that I have referred a correct path for financial planning and guidance.

Can you share your views on Jeevan Anand Policy bit clearly. I am 27 years old and I have taken 4 years back. I am seeing mixed views on this policy and want to get a clear picture on this.

Amar

Jeevan Anand policy main attraction was accidental insurance and term insurance (50%) even after the maturity of the policy. But it is a traditional plan and so maturity amount you receive is based on the bonus declared in the policy, which is not assured and based on the performance of investments which is majorly into debt.

Dear Solanki,

Jeevan Anand’s risk cover even after maturity is 100% of Sum Assured and not 50% as mentioned.

Dear Somasundaram,

Corrected. In previous version of Jeevan Anand Additional SA was payable on death after the term of the policy.

Sir, Can u suggest whether i-Guarantee plans launched by some insurance co. are good to go as it contains insurance as well as return.

Dear SSRao,

I have not evaluated this product yet so cannot comment. Will be doing it soon.

Thank you, Hemant !

You have nicely summarized the pros and cons of the system as a whole ! Congrats !

It is well suited for the risk-averse , conservative seniors !!

Hi Devadoss,

Even the risk averse, conservative seniors will find other alternatives more appropriate. 🙂

Dear Hemant,

Firstly correct your article as you seem to be in a hurry to be the first on to criticize.

In new Jeevan Anand entry age is 9 months and not 90 months. Secondly, you seem to be a great economist who compares everything w.r.t IRR.

Actually there is a term called as pay off. A person has to accept a certain lesser return when he needs advantage of Insurance.

What if a person dies say after 3 yrs after paying 3 premiums. The returns which his family will get returns which are more than any of your suggested ideas.

PPF should not be compare to Insurance. These are completely two different aspects.

PPF is for tax saving and long term savings. Insurance is for Protection, Savings and some decent returns.

Please do not misguide people. You have knowledge and that is great, But please use it for right purpose.

Hi Vicky,

Let me answer your query:

1. First, the product is single premium endowment the details of which is available on LIC website. At no instance Jeevan Anand is mentioned apart from queries of readers.

2. The second and most important is the benefits you have highlighted and I will be elaborating on the same. You have Illustrated two benefits of buying insurance plan:

a. Protection- Here most of us do a mistake when we do not evaluate our actual need of family protection. Put simply we do not know what will be the actual amount required by our family to sustain living if we are not there. I am sure if we do , the amount will be much high because we are trying to replace the income we will generate for our family till our retirement. Why? because that may be the only source for them to manage their expenses and repay liabilities which i may leave for them. So which insurance can give me such a high protection within the savings ability I have.You will also agree that premium in a policy like above or even Jeevan Anand will be out of reach. In my view a term insurance fulfill this requirement of giving a high protection right from the first day of buying it.So if death takes place in three years after taking the insurance, my family get more than decent amount to sustain.

b. Savings- I invest my savings not for dying tomorrow but to accumulate wealth for the goals i want to achieve. So i need investment where I don’t have to pay cost for any other objective and it can give me the returns to reach my destination. I don’t see it happening in traditional insurance plans.

c. Decent Returns- The definition has to be corrected because we have to earn real returns i.e. returns which can beat inflation. If my expenses are increasing by 6% will I be satisfied with 6% in 25 years time or even 10 years time considering i will be at the same position where i have begun. I think one has to answer this question first and then decide on the product.

All the points discussed above are different aspect of our planning and so need to be planned differently. We are no economist but simply evaluating products to see which requirement they can meet.

I hope this will clear any doubts you have on the analysis which is done.

I hope thsi

Dear Mr.Vicky,

Mr. Hemant is absulutely right. He said take term plan for insurance coverage and for investment purpose you have to select other options.

Swapnil

On line Term plan is best for protection. Several reputed groups as well as comparisons are available for private insurance companies. More reputed like SBI Life, HDFC Life, ICICI Pru Life etcIt is low cost due to bypassing middleman (agent). Still you wish to stick to LIC then you can take a LIC Term Plan.

Before taking Term Assurance First review Claim Settlement Ratio.

LIC has rejected only 1.12% of total claims whereas Private Companies have rejected 7.85% of Claims.

HI Ravindra,

In my opinion for Term policy, we should belive the standard product or company. Since its a long term purpose..! Is it now the LIC term Plan is available in market after 1st Jan 2014..?

Regards

Raj Sekhar A

Hi

Apologies for asking this question in a wrong section. But I couldnt find the answer when I searched on your website.

Question:

I am a NRI residing abroad since 6 years and plan to take up the citizenship there.

Am I eligibile to buy any life term insurance plans in India? I am 32 yrs male and plan to take the longest available term plan

( I have one plan in my current country of residence, but I want to buy one in India as well keeping in mind that I will return back in next few years)

Thank you.

Hi Sjn,

Yes, NRIs can take avail a term insurance in India.

dear sir,

my friend resides in USA wants to transfer his pension fund to india to QROPS. Is it possible. If possible what is the procedure. explain

HI ,

thanu here ,my age is 30 , need for pension plan 25 years long term nearly 25,000 quarterly (Without insurances ) can you please advice which plan is best to go ahead for good returns ,please give scenario with sum assured +bonus .. as a common man its bit of confusing around where to put money , would feel happy if you answered..please give chart table without insurances cover

sir i m 58 years old i want to buy this plan 500000 so plz tell me what the sum assured covered and for how much time and maturity time how much amount i will received

What is the benefits of two accidental LIC policy for one man

Can a man get the benifits of two accidental lic policy

Dear Sir,

I need a clarification for the below:

Rs.30 Lakhs was paid as Jeevan Rekha in 2005 and Rs.50 in 2006 as single premium plan. Now It has been pre matured in January 2015 and got Rs.33 and Rs.55 Lakhs where LIC has deducted TDS @2% on total amounts. Pls advice what will be taxable amount. When it has invested the amount was paid after Taxed Income.

I want to know if i invest 1 lac for lic single plan for 10 year & on maturity i get 190000 then it cums under long term capital gain or what

Dear Mitesh,

If the sum assured on single premium policy is 1.25 times the premium amount, then the maturity amount will be taxable.

Sir, I want to know.. Which is better, single premium endowment plan or FD, amount 12lacs for 10years. Does the mature value of endowment plan is taxable

Dear Renu,

Never mix your investment with insurance. Insurance is for financial security of family in case of something misshapen.As you want to invest for 10 years you should consider Mutual fund equity funds. This will give you better return than FD in long term.

Dear Sir,

I have purchase just LIC Single Premium Endowment Plan @ 50000/- for ten years. pl tell me what is the maturity amount or interest rate after 10 years. (Age 40 yrs)

pl reply.

Regards,

Dinesh Kumar

Dear Mr Dinesh,

We can not calculate the exact maturity amount.

Don’t expect more than 4-5% P.A return from endowment plan.

my registration no & member ID is-2768618, I have money trouble and family problem pl cancellation my membership & earliest possible and amount return pl.

Hi Bipin,

I can understand your concern but you have to talk to your agent for this.

Comments are closed.