Thank God! Till now no one has asked me the cost of one kg financial planning fees in India or one square foot of reviews. Financial Planning is at a nascent stage in India; hence fee discussion is very common in a preliminary call. I have also seen few surveys done by financial bloggers – on “how much should financial planners charge?” & numbers can frighten any serious planner. So, I decided to discuss this here – hope this will be helpful to clients as well as fellow financial planners.

Financial Plan vs Financial Planning

People feel that financial planning is about writing a financial plan when actually the financial plan is just the beginning of financial planning. An excellent analogy for this can be the difference between a wedding and a marriage. A wedding is an event, but a marriage is a lifelong journey. So the financial plan is just like a wedding which is just the beginning of your second innings. The major challenges start after that. So for most planners, financial planning is about building long-term relationships rather than having a one-time event of plan creation.

We, planners, keep saying that a financial plan is a blueprint or roadmap for the client’s financial life. I believe it is more of a reference document for planners and not clients. You will be surprised to know that there are many planners, who collect the data, prepare the plan and keep that plan with themselves, as they take the responsibility of bringing financial happiness to their client’s life. Here in this post, we are talking about financial planning, not financial plans.

Check Benefits of Financial Planning

Is there a standard processor model for financial planning?

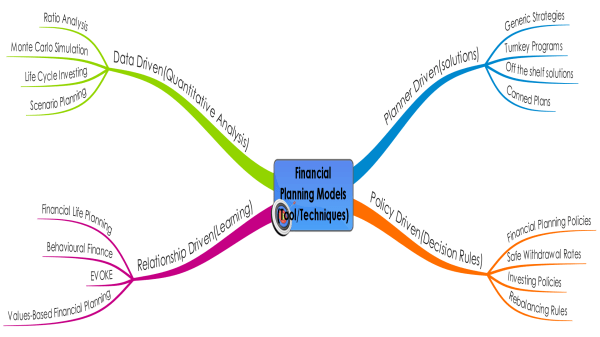

You have to understand that financial planning is not a commodity or product so there can be no standardization. However, you will find that every planner talks about the same things like retirement, investment, insurance, etc., or risk profiling, data collection, asset allocation, etc. the basic components of a plan are the same. Just like Tata Nano or an Audi Q7 will have the same components like tires, seats, steering wheel & will use the same fuel. But they are still very different cars and will serve different categories of people in different ways.

I think this clarifies that there can be several models of the same product (even if you don’t want to compare financial planning as service/advice – just imagine two lawyers, Harish Salve {he charges Rs 30 Lakh per day} with the lawyer you recently met or 2 doctors in your city – hope you got the point). I would like to share a couple of common financial planning models and tools/techniques

This list is not an exhaustive list as there will be many other models in various permutations and combinations. Even if we consider just these models, each one of them has a different set of engagement by planners and clients. There will be different processes and outcomes for all models. There will be requirements of time, systems, processes, and tools. So it is not right to compare two planners based solely on fees.

How (can) planners arrive at a logical fee structure?

Planners are in the profession of advice but the scarcest resource they have is time and the most valuable thing they have is wisdom. So either they can charge for their time or wisdom or a combination of both. This is something every planner will have to decide. The price should reflect the value that you are offering to the client. If the client is able to see the value proposition, he will find it easier to be able to pay. Clients should also keep in mind that a planner is also a business owner. He is charging for taking care of your financial future. He needs to be compensated well to keep his business viable. Adequate compensation will ensure quality people enter the profession and stay in it. If the profession does not pay well, all the good people will move out to alternate professions. The clients may end up with sub-standard advisors who might not be good for their financial health.

Defining an appropriate fee is both a subjective and objective exercise. It is complicated but let us try to put some numbers to arrive at some fee structure. Let us take few assumptions before starting:

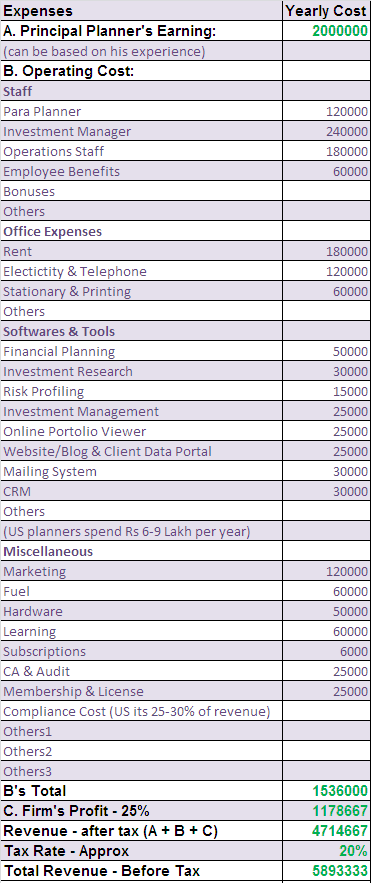

- We are talking about a boutique financial planning firm, which is the most common setup across the globe. Normally you will find 3-5 staff members in these firms. They will be – Principal Planner (normal owner of the firm) who is your advisor, the paraplanner who creates the plan (data collection & entry), the investment manager who does product research and/or keeps portfolios updated, and operations/compliance/systems executive.

- Usually, such firms handle about 100 families or a maximum of 150 families if they are super-efficient or working on limited deliverables.

We are trying to arrive at a fee/revenue per client on a simple cost basis.

There are three main components of overall cost:

Principal Planner’s Earning: He is the entrepreneur who started the practice; he is the person who is responsible for the client’s goals, the firm’s goals, and staff member’s goals. But what about his own goals and family responsibility? How he will be rewarded for the time he is giving, the wisdom he brings, and the risk he has taken? Passion for personal finance is what brings him here and decent earnings will be needed to keep him here.

Operating Cost: This includes everything from office rent, software, hardware, communication, staff salaries, continuous education cost, marketing, client events, compliance, audit cost, and a lot of other things. A firm needs to spend on these to service clients in the best possible manner.

Firm’s Profit: You must be thinking, why is this required when the owner is taking salary or profits? Each business or profession has its ups and downs. Similarly, even financial planning firms will have different phases including some multiyear rough phases, especially since it is a relatively new profession in India. If the firm does not retain some profit, is it a bad sign both for clients and for the practice? You must have heard of many financial advisors have moved to other jobs/businesses in the last few years. The biggest reason for this is that they never saved for a rainy day. Normally for running a healthy practice minimum profits that any firm should retain is 25-30%.

You may have noticed I have not considered tax implications anywhere. But a planner would have to pay service tax, income tax for the firm/company, and also on his own income as an individual.

Minimum Revenue Required – Calculator

Yearly Revenue Per Client based on Revenue/Fee Required & Number of Clients

Are these our firm’s numbers? No, our numbers are even higher. But these are based on my experience and interaction with a lot of other planners.

Few Important Points:

- Numbers can significantly vary from firm to firm.

- Numbers are not inflation-proof – so the number will increase in the future.

- Most of the financial planners across the globe are Fee-Based, so some part of the revenue will come from product advisory.

- Some financial advisors may charge less initially, in expectation to grow with clients.

- Few readers may feel this is unaffordable & they may be right. (we discussed this earlier – also check comment section)

- These charges may look small if you open your ULIP illustrations & check what you have paid in the last couple of years. So planners & advisors can save you from big mistakes. I will also share a post on how planners add value to your finance & life but it will not talk about the best returns.

Download calculator – You can change the numbers & arrive at minimum fees/earnings that a financial planner should earn/charge. (Though you can’t put a limit on what should he earn, but still if you want to play with the numbers you can)

Do you think if your planner/advisor is not earning that money, he will continue his practice or he will serve you right, and if yes, for how long. He may do something else, which will help him to achieve his goals but what about clients. Will you work, if you are not rightly compensated for your job? Feel free to share your views in the comment section.

Image courtesy of adamr at FreeDigitalPhotos.net

Dear Hemant

I think I missed the bus — as always!!.

Any how thanks for your reply and an educative video on Retirement Plannig.

I was about ask you but first I thought let me learn what a FP needs to know from me as it involves disclosing lot of financial information which could be difficult to share. —Though I have none!!!!

Let me educate my self first on process of FP and then will get in touch

Concept well explained. India is a broker driven market and we are talking of charging professional fees in a market where still rebating is common- Insurance agents still pass on a part of their income to the investor by paying the first years premium, hoping to recover much more from the earnings on future premium. While fee based consulting has started, I feel we are still a long way from this being implemented full swing. The investors are price sensitive and many of them would rather deal with a less competent and less qualified agent who gives them doorstep service without charging, rather than employ the services of professional planners who charge a fee for their services.

Very well-written and well researched article. This is plain truth, hard facts. No escape from this. If planners are charging less, they are surely not planning their finances and are following a non-sustainable model. And if they are charging more, they will have to cut down sooner or later.

Thanks Hemant for writting article on such topic.

You explained the financial planners costing structure in very crisp & simple way.

It helps clients like us to understand how our fees are getting utilised & what all different kind of activities that financial planner needs to do to keep his firm up & running.

Thanks Hemant for the informative article…

However, a few aspects that I feel need to be factored in are:-

A A Family Doctor charges us on case to case basis on consultation charges, A CA on the other hand esp for salaried employees charges a fixed amount for filing the annual ITR & during the course of the year is accessible for advise on Tax saving matters.

B. If my monthly investible surplus is say X, then what percentage of the annual Investment is being charged as fees would be of paramount importance. Esp since there is a limit to how much growth would be assured (Not guaranteed).

C A Financial Planner should NOT charge for merely providing a Financial Plan. Because, a plan needs to be followed up & worked upon over the years. Unless supported over the years, it would be a “wedding” & NOT a “marriage”.

Good Article…. Sharing the Saying of it on FB.

“I don’t work for money … but i don’t work without money” – Financial Planner

Hi Hemant,

Thanks for touching the most sensitive topic in Financial Planner and Client relationship. Hope people take note of this and respect the obvious benefits they can get from adopting the Financial Planning process.

Hello,

This is an excellent piece,kudos for putting your heart out for everybody.

I somehow feel that the sustainable model for Financial advisor is not about becoming a bigger brands but rather it is keeping you clients limited so that the ovrheads remain very low may be we call call them micro planners, so to me ideal situation which will be sustainable is 50 good clients per planner, this keeps the costs as well as the Fees down to reasonable limits….

Thanks Hemant for the informative

article…

Is there any certification for financial planners in India . How can we differentiate between a qualified and a non qualified financial planner.

CFP is the answer of your Que.

I am planning to have a financial planner – only for equity market advise and investment – and I wonder if his fee structure is justified.

His fees is 10% of (Opening NAV + Closing NAV + capital infusion + capital withdrawal ) /2.

So 10% of an average of opening, closing, infusion and withdrawal.

Added to this is a ‘management fee’ of 0.25% of the portfolio value at year end payable annually.

Is all this the normal fee chargable by FAs? His fees are not based only on the capital appreciation but it seems like he is extracting a part of my invested capital as his fee. Is this right?

Are there any other methods used to compute fees CHARGABLE by FAs?

Any advise would be greatly appreciated.

Thanks for informative blog. I am considering a planner and good to have stumbled on this blog.

In India I have observed that people are willing to pay a fee to a CA only if they are getting a refund. The mindset is very primitive, like a barter system.

Moreover, once they’ve paid you for filing their income tax return, they don’t consider it necessary to pay you for taking advise on how they can plan their taxes, what investments they should make, etc. Also people who are family members dictate terms, “I should get refund of my whole TDS”.

If refund gets delayed ” you must have taken my refund”.

Overall it is a thankless job.

Agree Ritcha

Comments are closed.