LIC has its unique way of wishing “happy new year” by launching new products. This time LIC has come up with 2 new products – A Unit Linked Product (ulip) “LIC Flexi Plus” and a traditional pension policy “New Jeevan Nidhi”. Timing of Launch of the policies is also due to sharp business sense among LIC management as they understand Indian Psyche very well. They know that come what may we‘ll start looking for tax saving options in the months of January February only and If the new product is launched by LIC then people will definitely give it a consideration and deserving attention. Through in this article I have reviewed LIC Flexi Plus and try to figure out how this is different from other options available for investors.

LIC Flexi Plus – Summary

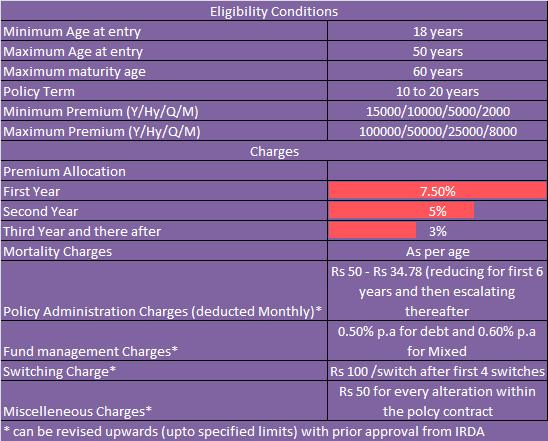

It is a normal Unit linked plan launched as per the new ULIP guidelines by IRDA. It has very less charges as compared to ULIP’s previous versions. The minimum premium paying period is 5 years. The Premium payment after deducting the allocation charges gets invested in a selected investment option and you will get the fund value on maturity or surrender (applicable after 5 years). Fund value totally depends on the performance of the investment option and will be calculated as No. of units available on surrender/maturity after deducting all expenses, multiplied by NAV. If you discontinue the premium payment before 5 years than the fund value in the year of discontinuance will be transferred to a discontinued fund after deducting the discontinuation charges. This fund will earn you saving bank account interest rate of State bank of India. As LIC Flexi Plus is a Unit Linked Insurance plan, so it has some insurance features too. It offers sum assured as 10 times annual premium or 105% of total premiums paid whichever is higher. Please note that it is mandatory to have 10 times of Sum assured on your premium payment to get section 80C tax benefit.

LIC Flexi Plus – Key benefits

LIC Flexi Plus – Discontinuation Charges

| Where the policy is discontinued during the policy year | Discontinuance charges for the policies having annualized premium up to Rs. 25,000/- | Discontinuance charges for the policies having annualized premium above Rs. 25,000/- |

| 1 | Lower of 15% * (AP or FV) subject to a maximum of Rs. 2500/- | Lower of 6% * (AP or FV) subject to maximum of Rs. 6000/- |

| 2 | Lower of 7.5% * (AP or FV) subject to a maximum of Rs. 1750/- | Lower of 4% * (AP or FV) subject to maximum of Rs. 4000/- |

| 3 | Lower of 5% * (AP or FV) subject to a maximum of Rs. 1250/- | Lower of 3% * (AP or FV) subject to maximum of Rs. 3000/- |

| 4 | Lower of 3% * (AP or FV) subject to a maximum of Rs. 750/- | Lower of 2% * (AP or FV) subject to maximum of Rs. 2000/- |

| 5 and onwards | NIL | NIL |

Also please note that discontinued fund will be charged with 0.5% p.a of Fund management Charges

LIC Flexi Plus – Investment Funds

| Fund Type | Investment in Government / Government Guaranteed Securities / Corporate Debt | Short-term investments such as money market instruments | Investment in Listed Equity Shares | Details and objective of the fund for risk /return |

| Debt Fund Mixed Fund | Not less than 60%Not less than 45% | Not more than 40%Not more than 40% | NilNot less than 15% & Not more than 25% |

Low riskSteady Income –Lower to Medium risk |

Should you invest in LIC Flexi Plus ULIP?

The decision is purely financial and I would like to leave this with you, with the following thoughts.

- What if after 2 years you feel that none of the investment fund is performing as per expectation? Or you would not be able to pay further for personal reasons then would you be comfortable enough in leaving the fund in discontinuation fund earning you saving bank a/c return?

- Debt investments perform differently in rising, falling and stable interest rate scenario. There are other debt instruments for short/medium/long term horizon available, which are more actively managed and have potential to deliver much better returns and having flexibility to switch as and when required.

- Even if you chose “Mixed fund” option for parking of funds (15%-25% equity exposure) in LIC Flexi Plus, would it be wise to invest with a 10-20 years horizon?

- Even though there is some sort of government backing to LIC but government interference has its own negative factors.

- I have presumed that readers of TFL are adequately insured and are convinced on buying term insurance… and if this is the case then would it be wise to pay more mortality charges.

- With the reduction of charges some may argue that ULIPs have now become cost efficient than Mutual funds in the long term, which is true to some extent. Personally I have always found the structure of ULIP very attractive. But on the other side I want investments to be flexible enough, on which cost effective, immediate and comfortable action can be taken as and when required and ULIP does not give me that flexibility. I mean I can go with index funds, now days there’s option of direct plan, direct stocks, Bonds, Fds or whatever investment instruments suits my risk appetite, goals, tax profile etc.

Many people are of the view that Financial Planners are against ULIPs but this is not true. We are not against or in favour of any product but it actually become difficult for us to map the goals of clients to such non flexible and costly products (though for few years). Anyone who’s having their basic financial planning, investments and goals intact can do anything with the surplus he’s left with if any. But it’s always advisable even to use that surplus with caution to factor in the uncertainty risk in financial plan.

Review of LIC Flexi Plus is done by Manikaran Singal, CERTIFIED FINANCIAL PLANNERCM – the views expressed herein are the author’s personal views.

If you have any query related to LIC Flexi Plus or any other insurance product – feel free to add in comment section.

Hemant, thanks for giving me opportunity to be on TFL. It really nice to be here.

While writing this review i actually felt the positiveness came from reduction in allocation and surrender charges of ULIP. But still this non flexible structure keeps me away from such products. I feel that IRDA should again look and make these products more flexible and open for investors and should avoid hiding behind the statement that ” Insurance products are difficult to sell”. When such products are pitched as investment options than it should be comparable to them only and not to insurance products.

Thanks Manikaran for contributing this post. Its good to see that expense ratios are coming down – but I don’t like 2 things about using insurance as investment – first thing that you mentioned in your points “what if funds are not performing” & second the compensation structure “if agent sold you some policy & if he don’t advice/service your policy in future, he is not going to loose anything”.

I will appreciate if you reply to queries of TFL Readers.

Yes hemant i totally endorse your views. That’s why i say that If these products are going to be pitched as investment options IRDA should also fix some level of service quality on such things. These days there’s option to change broker in case of MFs but in case of insurances there’s no such provision.

I would be happy to answer TFL readers queries.

Dear Manikaran, Thanks for the review, But in flexi plus there is an added benefit which should be highlighted, in the event of death of the policy holder, 1. Sum assured is paid to the nominee, 2. Future premiums are waived 3. Future premiums to be paid will be credited in the policy holder account as per the prevailing NAV and on maturity will again pass to the nominee. This is a novel feature, Secondly Pension Plus the first ULIP launched by LIC after the september 2010 new ULIP guidelines in volatile market with same investment options. the current NAV of Debt fund is 12.11. I think in long run DEBT fund and LIC investments will surely give good returns to customers.

Yes Sunil you are right. I forgot to mention the death benefit. Thanks for pointing out. I agree that this is a novel feature but you also have to agree with me that more the benefits more will be the cost. The inbuilt waiver of premium and other riders will surely in turn increase the cost which will effect the returns negatively. I think this is why i don’t believe in mixing insurance with investments. The more the insurance benefits the more will be the cost and thus less returns on Investments.

I agree with you on NAV also, but NAV does not mean returns. Also we can’t say that fund will keep on performing like this. We understand that these days there’s good potential of return on debt side and due to market factors i am seeing that any investment which is into debt is giving good return these days. The same way as any investment in equity was giving good returns in 2006-07. This means that the returns are due to market factors and not due to good fund management.

My issue is with the structure of product…as i wrote in the article ” what if it stops performing later”. I have no issues in people buying life insurance for death benefits..infact every insurance policy looks good looking at death benefit. But one has to look from various other angles when one is buying insurance policy from investment perspective.

If look at the charges with respect to Mutual funds here we are paying more than mutual fund brokerage charges. (Premium allocationc hage, FMV, AC, mortality etc) which will eat away your units and when compared to LIC’s ULIPS in the past most of them are not done well in the market and finally even if you invest upto 10 years finally ending up with getting principal only which we have seen recently after getting the ulips matured. Other than sec 80C benefits we can’t gain anything more from Ulips and Mutual funds stands better position if we look at long term or short term.

Money Plus Flexi Plus

Allocation charges 26.5% 7.5%

Admn charges Rs 60 pm Rs 50 pm

Fund Management 1.5% 0.6%

5,000 to 75,000 26.50% 5.00% 2.50%

Dear Anatha Krishnan, I totally agree with you on the charges that Mutual funds are cheaper than ULIP, but as you mentioned regarding the old ULIP of LIC, yes in some plans what you said was correct, that the customer is getting the principal after 4 or 5 years especially under plan called Money Plus, as you said one of the reason was charges,

But if we consider LIC old ULIP like Bima Plus launched in 2001 and the evergreen product Future plus launched in 2005 the returns are enormous, Future plus was the product which really started the boom of ULIP’S in LIC. After the intervention of IRDA from sep 1 2010, the charges of ULIP has come down drastically including, charges, commission FMC etc. Just a comparison with Old ULIP.

Money Plus Flexi Plus

Allocation charges 26.5% 7.5%

Admn charges Rs 60 pm Rs 50 pm

Fund Management 1.5% 0.6%

All investment managers and customers are considering ULIP on pre Irda regulation period, now its really good time for customers to park funds in ULIP it became more attractive, since the commission is reduced drastically the sales has come down, Being in this industry for some time i strongly suggest New ULIPS in the market is really good to invest for long term.

The greatest USP of ULIP is the switching factor which Mutual fund doesn’t have.

Dear Hemantji,

Wish you happy new year 2013. I am a regular reader of your post. Some extend I don’t agree with Mr Manikaran about what he says. This is my opinion…Investment & Insurance are two different things. The job what LIC Of India is doing in Indian Insurance market is fantastic. Why ULIP with insurance is JINDAGI KE SATH BHI -JINDAGI KE BAD BHI. tell me or correct me First 5 yrs locking period means regular habit of paying premium and if the PPT is 10 /20 yrs and the policy holder survives he will get maturity amount is tax free . In case death occurs before PPT.. nominee will get Sum Insurance +. Any one situation…. no risk. Addition to this I sense that the author is anti LIC.

Vinod ji…i don’t get you. On one side you are saying that you don’t agree with me and on the other you are endorsing my statement that “Insurance and investments are two different things”. I am not anti LIC infact i also agree with you that LIC is doing a fantastic job in Indian insurance market. The reach which LIC has in india and the confidence it has gained in the mind of people is really commendable. But it was also because there was very less information flow and competition earlier.I just wanted people to think on some points before getting into any product which comes with a mix of insurance and investment.

I believe you don’t need a product to be disciplined …its all in mind and once you have developed that mindset then there would not be any problem. Before investing in any product one should be having a holistic view on his finances and do a proper financial management keeping in mind one’s current and future requirements. Do proper risk management and keep investments flexible. If i am an indisciplined investor, no 5 years lock in can make me invest for the full tenure and if i am disciplined ..then i can go with any product

another reason why indians had blind faith in LIC in the past:

till 90’s, GDP of india was around 3%, with matching inflation.

so LIC’s CAGR of 4-6% was sufficient to comfortably beat inflation.

am I correct?

Hi Hemant,

This article is very usefull and eye opening to many as many Tax saver would be planning to invit now and they fall to the trap of this kindly of policy.

I personally wish to thank you and Manikaran for this good knowledgable article.

Sujith Kumar

Thanks Sujith for liking the article. I appreciate it.

hhello, Mr Manikaran, I want to take this insurance policy, enroll 30K+ for 12 to 15 year what would return I get, u expect means that whats the benefits is this a better a Investment plan or insurance ??

Dear Manikaran Singal,

Which point you consider when you write your views for LIC flexiplus? Why you are compare this product with Mutual Fund? Can you tell me why Mutual Funds segment goes down day by day? Just because of views given by you non insurance person very much highlighted more & more about mutual fund and Indian person belive on advisor like you? Who has not have idea about Investment Pattern of LIC of India. Mutual fund market also stable before CFP come in Investment Market, but when CFPs are come in Investment Market, Investment market are start collepsed. What ever you study, study material design by Western Market and not according to Indian Market. Layman can’t understand Western Market Formula, they under stand simple language rather than complicated Formulas. So when write any thing about any insurance product, 1st think from layman view angle and than write your views. CFP means Completely Failed Products of Investment Institute Market. Any Insurance Company design their product with consider layman expectation. Sorry for my view in very hard language. But because of i am layman person who understand requirement of layman person and hence offer only simple products only rather than complicated investment formulas.

Let me answer you one by one.

Q) Which point you consider when you write your views for LIC flexiplus?

A) Customer’s benefit point of view.

Q)Why you are compare this product with Mutual Fund?

A) Because this is an investment product.

Q) Can you tell me why Mutual Funds segment goes down day by day?

A) I don’t think its going down day by day. But yes many Mutual funds agent are entering into insurance market just because here they can earn more upfront commission. take the example of banks…they are happy selling insurance policies.

may i request you to provide me and readers with the “Investment pattern of LIC”. What i know about the investment pattern is that its a puppet in the hand of government…and government use this institution for funding there own requirements, making so called disinvestment process a success…

I don’t understand that linkage of Investments markets with CFP. CFP is just a certification, it doesn’t make you a good practitioner . also if someone is a good practitioner he may not be a CFP. Moreover CFP curriculum is as per indian scenario only. I encourage you to go through the study material first.

I also endorse simple products which a layman can understand better, that’s why i advise to keep insurance and investments separate. Tell me being a layman, which one is simple to chose – PPF or endowment policy?

Nice article

Hi Mani,

Thanks for the educating articles. I have taken Max Amsure Secured Return Builder Plan (ULIP) from Max Life Insurance since 2009. I am paying annual premium of Rs. 50000/- in increasing pattern. This is the 5th premium I am about to pay and I started having doubt on performance of the Company and the ULIP per se. Pl advice me, what would be the best course of action; to stop or continue with this. And what do I do to know my present fund value

Comments are closed.