NPS or the National Pension Scheme was launched in India on May 1, 2009. It is a scheme which enhances social security in our country and its aim is to provide social security after retirement.

Before the launch, in India, we had a Defined Benefit Plan. As the name suggests one would get a certain pension fixed for the whole of his life. This means the post-retirement proceeds were fixed and if there is a shortfall in this corpus, the Government would make good.

The NPS is a Defined Contribution Plan, where the returns would not be fixed. But now NPS is a defined contribution plan so that you will only get what you have contributed & return that fund manager generated on it.

Read – What is Gratuity

In his election speech in 1935, Franklin Delano Roosevelt said: “it is the more obligation to honor the right of the citizen to live with dignity even in the retired life”. When it comes to a pension or social security, our eyes turn to the Government.

In India also, the charm of being a government servant is the Pension that you get in your retirement years. So to reduce the burden on its expenses the NPS was introduced by the exchequer. Around 8-10 Crore investors are estimated to be eligible to join this scheme.

Regulator

Pension Fund Regulatory and Development Authority (PFRDA) is the regulator for the NPS. PFRDA was established by the Government of India on 23 August 2003 to promote old age income security by establishing, developing and regulating pension funds.

Must Read – LIC Jeevan Akshay VI

Applicability

All new entrants to Central Government services (other than Armed Forces) after Jan 1, 2004, would compulsorily join this scheme. All Indian citizens, including NRI, aged 18 to 60 can voluntary join the scheme. The exit age will be 60 years.

Contribution Requirements

A minimum contribution of Rs. 1000 Would be compulsory per year to keep the account active. There is no maximum limit on your NPS Tier 1 contribution but you can avail tax benefits of Rs. 200000 only. The minimum initial contribution to the NPS Tier 1 account is Rs. 500.

Structure & Investment Categories

Under NPS, each subscriber would be allotted a unique 16 digit Permanent Retirement Account Number (PRAN). This number would be portable. The records of transactions and investors would be maintained by a central record-keeping agency (CRA). At present, NSDL is the CRA and in the future, the number of CRA would be increased. The subscriber has an option to invest with seven Pension Fund Managers (PFM). He also has the option to choose any one or multiple PFM to manage his contribution. these PFM will have 4 Kinds of funds categorized as A for Alternative, E for Equity fund, G for fund investing in Government Securities and C for Fixed income securities other than Government Securities.

NPS Auto Choice – investors who don’t want to get into selecting how much to invest in which category can go for Auto Choice. It means that based on your age your money will be distributed in various categories. If you are young more exposure to equities – as your age will increase & risk capacity will come down automatically system will reduce exposure to equity & increase in Debt.

Must Read – Saving’s not enough Invest Your Money

Subscription types

To apply for the National pension scheme India, there are two types of accounts:

Non – Withdrawable account: The Tire 1 account is the basic NPS account that is non -withdrawable till retirement on in the case of the death of the subscriber. In this type of account, the total corpus at the retirement age is split, whereby a minimum of 40 percent of the final corpus has to be compulsorily used to buy an annuity while the subscriber is free to withdraw the remaining 60 percent as a lump sum or in installments.

Withdraw-able Account: A tier 2 account is available to only who is an existing subscriber of the tier 1 account. The unique selling point of the tier 2 account is that money contributed into this account can be freely withdrawn as and when the subscriber wishes except for the minimum balance that needs to be maintained at the end of each financial year.

Investment Charges

The NPS levies an investment charge of .01% of the asset under management. Initial charges of account opening would be around Rs 350. These charges are bound to come once the investor base increases.

Must Read: The 3 Stages of Retirement

Tax on NPS

The contribution under the Tier I account would be Rs. 150000 under the Sec 80C and Rs. 50000 under 80CCD(1b) of the Income Tax.

This is a positive step for investors as a higher amount can be deducted to compute taxable income. If you are in the higher tax bracket, you should consider investing as the outgoing tax amount can be reduced.

NPS manages to win EEE(exempt – exempt – exempt but not 100%) system that means at the time of maturity 60% of the accumulated corpus can be withdrawn as a lump sum(tax-free) and the remaining 40% needs to go into the purchase of an annuity plan. The annuity income that you earn from the plan will be taxable at the income tax slab rate of your income.

Must Check – Penny wise consumer – Pound foolish Investor

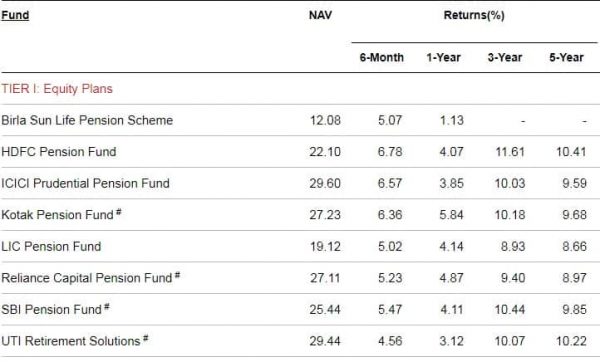

The Pension Fund Managers

At present, there are eight PFMs. These are UTI, Birla Sunlife, SBI, LIC, Kotak, Reliance Capital, HDFC and ICICI Prudential.

The returns are not guaranteed and as per your fund selection and performance of the Fund Manager. Below are some historical performances as of 13th July 2019.

Also, Read 8 Facts About Retirement Planning you May not have known

How can I apply for the NPS?

The NPS scheme is offered through 23 point-of – Acceptance or POS. The major are SEBI and its 7 associated banks, ICICI Bank, IDBI Bank, OBC, Allahabad Bank, CAMS, etc. Not all the branches of these POS offer the information and services for NPS. You can check the website of the particular POS or call their toll-free number to get information about the availability of this scheme. Also a word of caution: Few cases have been registered, where investor approached for NPS but was offered ULIP as the retirement solution product. Please read the offer document of NPS to get the finest details.

Should I Invest in NPS Now?

I am still not fully convinced with the idea of the compulsory 40% annuity as it’s a very complex thing & very limited options are present in India. Hopefully, 10-15 years from now when people who first enrolled for NPS start entering their retirement age – annuity will be a big market & better choices are available for retirees.

Halfheartedly I will suggest that people who are in the higher tax bracket can consider investing Rs 50000 every year in the National Pension Scheme.

If you have any questions on NPS India – feel free to add them in the comment section.

in Indian Stock Markets")

Is this a very good scheme for professionals and if i want to invest in this and i want to calculate how much i should invest to get 15000 as my pension is there any formula? can u share it with us.

Thanks and Regards,

swati shevade

@ Swati

It’s very early to say that ‘it’s a very good Scheme’ – now & then there are lot’s of changes in the investment world & especially in NPS. Ya but it’s expense ratio is very low.

Regarding the calculation part your question is incomplete(for how many years you need this income, do you want to consider impact of inflation etc).

If you have any specific question mark a mail to [email protected]

Dear Sir,

My PRAN No is 110051752086. I am retiring on 28.02.2013. Please let me know how can I get my pension and other benefits after retirement.

Shrwan Kumar Pathak

Dear sir my contrubution is monthly Rs1372 im govt employee myretirement date is 31-6-2030 how pension i should get.

Feel good and confident about nps.

Dear sir my contribution is monthly Rs.3752. I am govt. employee and my retirement date is 31-03-2034.How much pension I should get.

Sir my name is amareshsavadatti iam also govt employee since2007 backlog amount is nil & deduction for nps scheme is1373 how much pension& lumsum amount i will get at the end of retirement my retirement date is 31-6-2030

i want to know how to change fund managers

Sir,

I have been appointed under State Govt. of Assam in the year 2008 at the age of 29. My retirement will be in the year 2039. My contribution towards NPS is Rs. 3200/-pm including empoyers share. Now, let me know wkat will be my pension pm after my retirement.

With regards

Raktimava Dey

Dist. Hailakandi, Assam

(m) 9435095519

I want to join nps scheme. Plz tell me if govt would contribute 1000 rs. Every year in the account

minimum pension under nps and gratuity for central govt employee

Sir i have resigned my post and i did one year completed and my question is how to withdraw my nps deducted amount……plz rply me sir..

@Pankaj,did u get your amount?

Pankaj same issue with me

I also resigned after working for 1 year in union bank..

How did you collect your nos amount.

Pls tell me

sir,i am a NGO from maharashtra,latur.please provide all nps schme details for govt.employs NPS account.

sir i am gov.employee i want to know that after retirement all the 100% accumulated amt that i can withdraw together or not or before retirement any rules that i can withdrawl money in running service pls sir inform me this information

Good evening sir,I had join delhi police in 3/7/2006.After that I resigned my job on 25/3/2011. Now I want to withdrawal my money.please sir tell me how should I withdrawal my money from pran(nps)

Can you clarify whether the annuity ( not the accumulation phase) in a NPS is also proposed to be tax free ?

Currently the NPS has only the accumulation phase. An annnuity has to be purchased from one of the insurance companies, who are offering immediate annuity ( not defered annuity).

@ Sunil

“… annuity schemes will also be subject to EEE method of tax treatment.” Point 3.1 of discussion paper says this. (but still it’s a discussion paper)

They have not mentioned deffered or immediate annuity. We feel same tax treatment will be applicable for both.

PFRDA site has given following information about death of PRAN holder.

the amount can be disbursed as pension to SPOUSE of PRAN holder.

but what about corpus left after death of spouse.

will that be given to family members especially children as lump sum or on a monthly pension format?

@Prasad

Will be given back to legal hires as lumpsum. Only in case of some annuity schemes amount is ceased.

One lesser known fact about NPS.

For Govt employees the equity component in Tier I is fixed at 15%. No change is possible at present!

Pattu, Thanks for sharing this.

hello.

i m a govt employee and under NPS scheme govt is deducting Rs 1823 from my basic salary. can u pls tell me how much Govt will contribute against this deduction.

Yes. As your employer, the Government will match your contribution and transfer this amount also to your Tier-I account in your name.

I’m a private sector employee. My date of birth is 12/5/1985.

I want to avail NPS. I want the scheme or plan for myself.

I want to contribute Rs 3000 per month, then how much I would get as pension when I’ll attain the age 60?

and is there any difference between tier i & tier ii plans in terms of rates.

can i increase the amount later.

sir,i want change my contact no. from nps form bcoz my mobile lost and now i have new no. i want to send new mobile number to NPS-CRA office so that i can get all infomation which CRA SEND EVERY MONTH.

sweety g

for any correction (like mobile no,email id etc,) aap S2 form fill kar sakte hai

I’m a private sector employee. My date of birth is 12/5/1985.

I want to avail NPS. I want the scheme or plan for myself.

I want to contribute Rs 3000 per month, then how much I would get as pension when I’ll attain the age 60?

and is there any difference between tier i & tier ii plans in terms of rates.

can i increase the amount later.

I am a govt. employ. My NPS is deducted Rs. 1214/- per month from my salary. please let me know the what amount will I receive at the time of my retirement.

@Abhay

Can you tell us your age?

sir

i want to know my recent balance,means what is the total ammounts are added in my account

my age is 26.and the deduction is rs-1214/pm

Sir,

My PRAN No. is 110070010792 I forget my pasward & my a/c is locked. Pl. send me new pasward…

Thank..

I HAVE the same problem plz guide me.

Dear sir, good evening

I am going to resign from present organisation and i will join new organisation .i am already member of NPS but after joining in new organization . i want to start new NPS account without information of previous account.sir is it possible ?sir give suggestion about this as soon as possible .sir also give me personal contact number please..

Dear sir, good evening

Dear Sir,

I worked for central goverment as senir technical assistant and now want to switch to central bank of india as agriculture officer. .I have not informed of my previous employment where i was subjected to NPS. Though i have all my release letters. I want to join CBI without mentioning about previous employee details is it possible to do that, as i am already subjected to NPS. I am joining at a bank due to personal reasons. Please Help if you feel appropriate.

Do u get answer to this problem , if yes please do reply

HI, just read your comment..I am facing the same problem ..Did you get any solution ?

Did you get the answer?? I am also facing the same problem….

Same problem here. Did you get any answer? Plz reply

sir my orange no is 110031065935 I forgot my password and also my account has been lockedlocked.pleaseplease send me new password thanks.

sir my name is shashikala.m.s,I am also government employee since 2007,backlog amount is 1171 & deduction for nps scheme is 2080.I am tier 1 account holder.how much amount I will get at the end of retirement. which one is beneficial either tier-1or tier-2.how to change for tier-2 scheme,weather we can contribute certain amount to tier-1 as well as tier-2.please inform me.

I forgot my password plz send newpassword to my email address

I’m a private sector employee. My date of birth is 29/06/1977.

First of all can I avail the NPS?

If yes, suppose I will contribute Rs 2000 per month, then how much I would get as pension when I’ll attain the age 60?

Also will I get some lumpsum amount along with the pension?

Will I have an option to take a lumpsum amount or only pension or both?

What would be the lumpsum amount?

Can the account transferable from branch to branch? for example I opened the account at Hauzkhas, Can I transfer to Chandinichowk?

What are to documents required to open a NPS account?

First of all can I avail the NPS?

> Yes you Can

If yes, suppose I will contribute Rs 2000 per month, then how much I would get as pension when I’ll attain the age 60?

>NPS is a defined contribution plan and the returns are linked to markets and also the asset allocation chosen by you. Last year category average returns of the pension fund managers was in the 19.5% & top performer UTI gave return of 24.6% in same period. But this is just one year performance when equity markets have given good returns. Assuming a CAGR of 10% your contribution of Rs 2000 pm would be able to accumulate Rs 33 Lakh in 27 years. After accumulation you need to purchase annuities, if we assume that you buy fixed annuity for 15 years which pays you approximate 6% Return – you will get Rs 28000 pm.

Also will I get some lumpsum amount along with the pension?

Will I have an option to take a lumpsum amount or only pension or both?

What would be the lumpsum amount?

>Please read the “subscription types” in above article.

Can the account transferable from branch to branch? for example I opened the account at Hauzkhas, Can I transfer to Chandinichowk?

>Yes

What are to documents required to open a NPS account?

For More details Visit http://www.pfrda.org.in/

my date of birth 15.05.1966.Having govt employee .Contribution p.m.is 3000/-.how much pension will i received at 60.plz reply

Hi Sukhwinder

I am assuming that Govt is also contributing the same amount – means total contribution of Rs 6000 PM.

In 16 year @ 10% CAGR you can accumulate approximately Rs 26 Lakh. After that you have to purchase annuity. I am assuming you will purchase 15 years fixed annuity & annuity rate at that time will be 6% – You may get monthly pension of Rs 22000.

i am central govt employee( railway) they are deducting 3700/- for NPS subscription, means 7400/- total, including govt matching fund, my date of birth is 11.06.1978 & date of entry into service is may 2008, at the entry level my NPS subscription was 2000/- (Total 4000/- including matching fund. how much pension may be expected after my retirement.

Dear Sir, I have following queries:

1. Till what age can the person get pension from the age of 60?

2. The corpur left after the death of the holder ,say at 80, will that be given to the nominee?

3. Till now what and where can we come to know about the performance of the NPS? Like, Equity option what is the NAV till date?

4. Why is this scheme not popular as others? Other than Government One…

Thanks in advance.

Hi Darshan

Please find the inline reply:

1. Till what age can the person get pension from the age of 60?

> It depends on the type of annuity you choose – there are 6-7 type of annuities. If you choose ‘annuity for life’ you can get it upto your death.

2. The corpur left after the death of the holder ,say at 80, will that be given to the nominee?

>Again, it depends on the annuity choice, If you choose “Annuity for life with return of purchase price on death of the annuitant” your nominees will get that amount.

3. Till now what and where can we come to know about the performance of the NPS? Like, Equity option what is the NAV till date?

>NPS is a defined contribution plan and the returns are linked to markets and also the asset allocation chosen by you. Last year category average returns of the pension fund managers was in the 19.5% & top performer UTI gave return of 24.6% in same period. But this is just one year performance when equity markets have given good returns. (Right now there is no sngle source where you can compare the performance or check NAV)

4. Why is this scheme not popular as others? Other than Government One…

> Firstly there are still few loopholes in the product, Secondly it doesn’t pay anything to advisor 🙂

let me know how far NPS is better than old Pension procedure. shall i get gratuity/Commutation etc in NPS

Please inform me on tax status for tier II account.

The amount you will withdraw before maturity will be taxable.

I’m a private sector employee. My date of birth is 08/08/1965.

Iam contributing Rs 15000 per quarter ,( Rs.10000 for tier1 and Rs. 5000 for tier2) then how much I would get as pension when I’ll attain the age 60?

Will I get some lumpsum amount along with the pension?

Do I have an option to take a lumpsum amount or only pension or both?

What would be the lumpsum amount for tier 2?

Hi Praveen,

In Tier 2 money contributed into this account can be freely withdrawn as and when the subscriber wishes except for minimum balance that needs to be maintained at the end of each financial year.

If we assume a rate of 10% in next 15 years – your accumulated sum at retirement will be 20.4 Lakh. Out of this 6.8 will be in Tier 2.

If we take one more assumption that you will withdraw full amount from Tier 2 as lumpsum you can still expect a monthly pension of Rs 11500 for 15 years.

Dear Hemant

Thanks for your reply can you guide me where I can take a printout to submit my employer for TAX REBATE under this NPS INVESTMENT otherwise TDS will be duducated from my salary for the amount which invested by me on NPS.

Hi Praveen,

You can take statement from POS.

Dear Hemant

Thanks for reply , but i can’t understand the meaning of POS kindly explain

Praveen

POS is point of sales 🙂

Dear Hemant

Thanks for reply , In my case who is POS as I live in New Delhi and all transcation is done by South Indian Bank who is decalred in NPS list , Is South Indian bank is POS.

Ya South India Bank is your POS – they will give you the statement.

what amount is deducted in nps(new pension scheme)?

Hi Amit

If you are govt employee & joined service after 2006 your pension fund is actually contributed in this scheme.

If you are a private employee or business man – you have to decide your contribution.

Do we have to buy annuity from nps corpus?

Yes Pramod

NPS is a accumulation scheme – you have to separately buy annuity at the end of the period.

Hemant one more question

How to calculation of nps amount from salary ?

I am not able to understand this question but you should contact your accounts department.

its 10% your BASIC +D.A.

Can nris join new pension scheme india?

Yes they can.

Can we contribute less than 10% in nps tier-i ?

I am not sure what do you mean by this 🙁

answer is no!!!!

Thanks Ram.

She haven’t mentioned govt employee 🙁

no

@ Seema

No, You con`t contribute less then 10% of salary

What are the documents required for nps ?

Just proof of id & address proof.

How much one can earn according to new pension scheme in india?

Hi Manish

Returns are market liked & not fixed – 10% can be expected in the long term.

How to buy nps or easiest way to buy NPS? 🙂

Reach your nearest POS & start contributing.

Where we can apply for nps tier ii ?

For this first you need to have tier 1 account.

NPS can be opened at any POS – check the list in article.

I am a govt employee contributing Rs. 2000 +2000(govt)per month to nps. My age is 30.How much pension i will get on retirement if i don’t withdraw anything on retirement. How much i will get if i withdraw 60% of my amount on retirement.

I am a central govt employee contributing Rs. 2500 +2500(govt)per month to nps. My age is 35.How much pension i will get on retirement if i don’t withdraw anything on retirement. How much i will get if i withdraw 60% of my amount on retirement.

Hi Pratik

If we assume 10% return in NPS & 6% return in Annuity(15 years fixed annuity)

NPS corpus will be Rs 90000 after 30 years.

You may get a pension of Rs 76000 at that time.(which will be equal to today’s Rs 13000)

If you withdraw 60% of the corpus – pension will be 30000.

Hemant

I want to open an NPS account and I reached few banks like sbi & uti but they are saying that they don’t know about this scheme. How can I find out who is selling NPS. These days I am following your guidlines for every investment 🙂

Hi Sapan,

Thanks for showing confidence in us & following our guidelines. NPS is offered though 23 point-of – Acceptance or POS. The major are SBI and its 7 associated bank, ICICI bank , IDBI Bank, OBC, Allahbad Bank, CAMC etc. Not all the branches of these POS offer the information and services for NPS. You can check the website of the particular POS or call their toll free number (State Bank of India 1800 112211 & Axis Bank 1800 233 5577) to get information about of this availability of this scheme. We already have written

Also a word of caution: Few cases have been registered, where investor approached for NPS but was offered ULIP as the retirement solution product.

hi sapan…Where are you located..you can also contact IDBI Bank one of the POS on toll free nos 1800 200 1947. I work as Assistant MAnager in IDBI bank located at Jaipur.

If you are in jaipur, you may contact me on 0141-5106400.

Thanks

Garima Kotawala

Hi,

Do I need to stick to the same POS for carrying out my NPS transactions? So can I open NPS account with say Axis bank and then, due to change in residence, carry out subsequent transactions with say SBI (that is closer to my new place) ?

Hi Avinash

You can change POS, there is a small fees of Rs 20. You should call on tollfree no of AXIS 1800 233 5577 & get the details.

as u know govt employee have to contribute 10% of their BASIC +DA and same amount is being contributed by GOVT in nps.meanwhile thier DA is on an average increasd by 10% twice evey year.my own contribution is 3000/month.my basic at present is 20000 and DA is 45% of my basic.age is 30.what wud be corpus and pension amount keeping the fact in mind that the amount has to be increased every half yearly from both sides [employee and govt].

Hi Ram,

Thanks for solving queries of other readers.

Normally for a govt employee salary increases by 5-6% every year(Including changes after recommendations of pay commissions)

Assumptions I have taken for your calculation:

1 9% return on NPS & 6% on annuity that you will purchase after retirement.

2 5% increase in income every year (similar increase in NPS Contribution)

3 Retirement Age 62 & Life Expectancy 75

Your corpus at your retirement will be Rs 2.39 Crore – this will give you monthly income of Rs 5.20 Lakh every month for 13 years. (Rs 5.20 Lakh will be equal to Rs 80 thousand of today if we consider inflation of 6%)

Keep visiting 🙂

I would like to know taxable amount for my tier 2 account.

What % of tax is payable on gains if i withdraw

1. after 1 year

2. within 1 year

Do I have to pay any tax on gains as on 31st march on increase in Value even if I dont withdraw.

Thanks

@Amit

There will be no tax.

I am in private service and aged 49 yrs. Do you advise me joining NPS at this age? How is better option vis a vis pension ULIPs?

Regards

venkat

Hi Venkat,

At your age I will not suggest you entering NPS as there are still many loopholes that should be filled. Don’t go for pension ULIP – they are pathetic products.

Considering 10 year time in retirement – You should make your portfolio through Mutual Funds & PPF(It’s a 15 year product but still it makes sense to open it).

“The total corpus of NPS is 7,000 crore, whereas collections from the unorganised sector under the scheme is only 40 crore.”

Hi Hemant

I am a government employee in Western railway under medical department in Mumbai . My NPS is deducted Rs.1052 per month from my salary please let me know the what amount which i receive at the time of my retirement.my birth date is 23 November 1982.Thank you.

Hi Jitendra,

That will be close to Rs 60000 per month if you consider taking a fixed 15 years annuity.

Hi Hemant,

I am a private company’s employee.

I want to open a NPS from State Bank of India is this scheme available in this bank, if not then from which bank?

My Age is 26 years DOB: 08/10/1984.

I want to open with minimum of RS 1000.

How much amount i will receive when I attend the age of 60?

Will i show it for tax deduction?

Hi Deepak

SBI & it’s all associates are POS for NPS.

NPS comes under 80 C so your investments can be used to take the benifit.

If we assume a rate of 10% your accumulation will be Rs 34 Lakh.

How many years i should pay the premium. I want to know in terms of dd/mm/yyyy

Hi Hemant

My birth Date 27/04/1983

Hemant,

I am a state government employee and is into NPS. I has received PRAN(just a 12 digit number and nothing else). What I wish to know is will I get a PRAN Card, a I-PIN and a T-PIN. Where will I get the statement of transaction. (People in government NPS cell are not so co-operative and I cannot go to them asking for these things.) Guide me

Hi Chandan,

The PRAN is the primary number for identifying and operating the NPS account. Once the account is opened, CRA (Central Record keeping Agency) mail a “Welcome Kit” which contains the PRAN card and the complete information provided by you in the registration form.

You receive a T-PIN for accessing the account through call Centre and a I-PIN for accessing your account on CRA website. If you havn’t received your I-PIN and T-PIN, contact CRA. For more information you can visit (www.cra-nsdl.com/www.npscra.nsdl.co.in)

You can access your transaction statement and other details either through call Center or by logging on the website.

I think this will be helpful.

How to invest in New Pension Scheme 2011. Please provide details regarding the same.

NPS 2010 or 2011 is one and same scheme.

I am working in Indian Air Force and going to retire after tw0 year.

Can I open a NPS account?

Thanks…

Hi SGT M Kumar,

NPS is an accumulations scheme – you should avoid it at this stage of life.

My suggestion is go for Balanced Mutual Funds.

Minimum contribution in NPS is Rs. 6000.00 per annum.

i want to know that it is within every year (from date of acount opening to next year) or in every financial year.

Hi Vivek,

From opening of your account.

I am a State Govt. Employee.I received my PRAN kit one month ago. But i don’t know what percent i deduct from my salary. I am in account section, in which process the deducted amount send. please notify me & tell me can i deduct a percent of i wish to the new pension system.

I am a State Govt. Employee.I received my PRAN kit one month ago. But i don’t know what percent i deduct from my salary. I am in account section, in which process the deducted amount send. please notify me & tell me can i deduct a percent of i wish to the new pension system.

Reply

Hi Rekha & Parvat

In case of government employee 10% of the employee’s salary(basic+DA+DP) will be transferred into NPS account. Govt.(employer) will also contribute the similar amount.

Dear Sir,

I am a govt employee and am not sure for staying here for long. My grade pay is 5400 and Basic is 15600. DA is currently 107% making total income Rs.43430.

What minimum deduction can I avail to my PRAN a/c under NPS so that when I leave, I bear minimum loss(as withdrawing more than 20% from PRAN a/c is not allowed before 60 years of age).

i too have the same question.. plz any one can answer?

i want to invest 12000 per year. my age is 33 years.

after sixty years age how much pension will i get and upto what period? or tell me about principal amount.

Hi Jagdish,

At the end of this article there is a calculator that you can use to find accumulated amount.

https://www.retirewise.in/2011/02/systematic-investment-plan-mutual-fund-sip-best.html

I have joined IIT Roorkee on 13.10.10 at the age of 56 plus. In IIT pension is available for old employees but new entrants are allowed to join NPS. Since I am more than 55 years, am I entitled for coverage under NPS.

Hi Vijay,

NPS is defined contribution scheme & Max entry age is 60 – so I think you should be entitled to it.(contact your accounts department)

Hi,I am 39 year old my question is

A) what percentage is to be invested equity and debt?

B) which is best performing fund manager?

Hi Sunil,

By rule of thumb you can still invest 60% in equities – but if this is your first investment in equity don’t invest more that 30-40%.

Hi Hemanth,

I was planning to open an NPS account and start contributing. And while I was reading about NPS, in one of the responses above, you say there are loopholes in NPS. That makes me a bit nervous. What are the loopholes? Are you talking about any serious loopholes?

Hi Subramanya,

Few of them:

The debt instruments that the NPS buys are not indexed. So literally the fund manager can buy anything – the risk is on the unit holder.

Limit on govt emp equity participation.

They are not that big & may be solved with time. You can invest some money in NPS. (10%-15% of your savings for retirement)

please provide me the detail of pension plan

Hi Parag,

Which pension plan you are talking about.

i am working in SBI, My date of birth is 12/06/1984 and retirement is 30/06/2044.

I have contributed about 2200 monthly in NPS.Still I have not received any PRAN NO.

My Question is

1)How could i got my PRAN No;

2) approx what amount I can withdraw(in lump sum) at the time of retirement

3)If I died at the age of 58 what type of benefit I will received.

4)If opted for pension at the time of retirement what amount I will get per month.

Regard

Anrit Banerjee

Asst Manager

State Bank of india

Sir,

I am a govt. servant and contributing about 1800/- p.m. My date of brith is 17/12/1978. What will be the amount will I get at the time retirment i.e. after the age of 60? How much i will get if i withdraw 60% of amount on retirement?

I am a Central Govt. employee. I joined to my service on 04/09/2010. From october, 2010 salary a sum of Rs. 1475/- is deducting by my employer. My date of birth is 31/08/1974. How much amount I can got after my retirement and also how much pension I can got per month after 60 years. Please clarify. My mobile no is

980000000. Kolkata.Hi Shantanu,

Never leave your number at public forums.

My income per month is Rs. 25000/- approx. I want to invest Rs. 7000/- to Rs. 10000/- per month upto retirement age for my benefit. Please let me know the best secured investment idea for best return. Besides this I want to invest another Rs. 1000/- to Rs. 2000/- in every year due to getting DA / increment. Waiting for your comments.

Santanu Mukherjee

Howrah/Kolkata

Hi Shantanu,

In short term preserving capital is safety & in long term preserving purchasing power. You should make a combo of PPF & Mutual Fund SIP.

Hi!

My Basis is Rs.13350/- + Grade Pay of Rs.4800/- and DA of Rs.9256/- what will be my NPS contribution. I’ve applied for pran in Feb 2011 with my employer but no deduction as of yet upto MAR 2011 was done, no Ack is recieved yet, so now the questions are i) What will be my contribution amount? ii) when the account will get activated will the deduction be retrospective in nature (i.e from Feb 2011) or prospective in nature?

Thanx

I am working as assistant professor & presently drawing ugc scale of pay’. we are not clear about the nps scheme applicable to us.Pls kindly advise on this.

Hi Hemant,

I joined CRPF on 28.08.06 and 10% of my salry was deducted for DCPS.I have resigned the job on 5.09.2009. Then what is the status of my amount, will not I be refunded the amont, please let me know

I am a housewife( an indian citizen) who is not employed. Can I apply for this New Pension Scheme?

You may but why you want to do it. When you don’t earn you should not invest.

HI Sir

My Father is a Sales Man and at age of 55 year

now it will be benite for him to considered NPS and if yes than what amouny he will invest at each month .

and you tell that annuity will be done after complition of monthlly payment. what is it

Hi,

I think he should not opt for NPS rather then he should go for Monthly income scheme which will offer him 8%payable monthly.

Gud eve. sir,

i m employees of Kribhco and non-affilated-Union representative too. kribhco had a govt.pension scheme of yrs-1995, which allows very mini. amount as pension. Here we (with management) r in work out to adopt new pesion scheme for our employees(2200 employees), and we want at least half salary (of last month of service,) as pension. we also agreed to contribute and make a handsome-fund for new pension schme. so here we need ur advise for expected scheme. plz advise us regarding which option we can adopted?

in my case my birthdate: Aug-1972, and my basic: Rs. 24000/- as on today.

Hi,

In a Year you need to contribute Rs.6000 only and that you can do by investing 500 monthly.

In this there are three assets class which a person can opt for i.e. equity,fixed income securities other than government securities & government securities.

One can invest 50 % of total contribution into equity or up to 100 % into fixed income or government securities.

I am a central govt employee. I wanted to know whether the govt. contribution to my NPS account adds to my Gross Income and if yes whether I can show this govt. contribution to my saving limit of 1 lakh for tax benefit in addition to my own contribution to NPS.

As of now the govt contribution forms part of y(our) taxable income. This financial year onwards this cannot be used for tax deduction.

See this:

Employer contribution towards NPS goes out of sec 80C

If your employer was contributing towards NPS , his contribution was eligible under 80C , but with this budget while it will still get tax deductions , it would come out of 80C , which means that some space will be left under 80C for people whose employer was contributing in NPS . The person can now invest more in sec 80C because of this .

If the DTC kicks next year the situation will change again. If I am not wrong the govt contribution will not be part of taxable income

Dear Sir,I was a public sector employee in India but now resigned and working abroad.My dob is 08.12.1968.Since I left govt job, I am not entitled for pension.Would you suggest me to join NPS?or any other schemes like LIC pension plans, is it good?suppose I want to have amonthly pension of 40-50,000 after I retire @60 yrs of age, how much should I pay monthly for the above schemes?As an NRI should I pay tax?

how i find out total amountinpran card.

how i get the total amount deposit information.

Hi Hemant,

My age is 28 years and i am a private sector employee and i am not married.Iwant to invest 20,000 per year for a period 20+ years (long term investment ). Which investment you suggest PPF or NPS ? and Why?This investment should also considered for TAX saving. (For your information i have done investment in ELSS funds too..so looking for less risk )

Thanks,

Anand

Thanks,

Anand

Hi,

As you have told that your age is 28 and you want to invest 20000 yearly for long term i.e. is 20 yrs i will suggest you to invest in mutual funds through SIP which will give you return around (10-15)%. which is more than NPS & PPF.

At your age you should take high risk which will earn you high return,

If you are investing then long term mutual funds in equity are exempt from tax.

If one goes other post without proper chanel then another pran no. Will be issue or not. If his ppan no already exist before.

Hi,

No it wont be issued

If one have pran no and he left his job for higher salery without taking noc,can issue a new pran no. For his. Give me clear information about is please.

Dear sir, If one have pran no and he left his job for higher salery without taking noc,can issue a new pran no. For his. Give me clear information about is please.

Hi,Mani

No he cant issue a new PRAN No.

He can use the same even if u changes job or location.

Hi Tinks,

I filled pran form in my earlier job which I left before completing 6 months. so no deduction. but I dont know that the number was generated or not? It’s been 2yrs,no info related to this I am having. I joined new job without Noc. I shud give undertaking dat I havenot filled the form ever earlier?

i m employees of Kribhco and non-affilated-Union representative too. kribhco had a govt.pension scheme of yrs-1995, which allows very mini. amount as pension. Here we (with management) r in work out to adopt new pesion scheme for our employees(2200 employees), and we want at least half salary (of last month of service,) as pension. we also agreed to contribute and make a handsome-fund for new pension schme. so here we need ur advise for expected scheme. plz advise us regarding which option we can adopted?

in my case my birthdate: Aug-1972, and my basic: Rs. 24000/- as on today.

Dear Sir,

Greetings of the Day !!

I want to open a account in NPS. My DOB is 11/01/1976. We have some query regarding New Pension Scheme. I would be very obliged if you help me in this regard. My query is.

If I can’t afford to maintain my NPS account than what will happen ?

How can I close this account ?

If we exit before age at 60 in that situation when pension will be start ?

How many minimum years compulsory to maintain this account ?

I want to contribute through ECS facility. If I want to put additional contribution than how can we do it ?

How can I benefited from “Swablamban Scheme”. I want to contribute 1000/- monthly. If I increased this amount later than what will happen ? Government ceased my “Swablamban “ benefit and charge penalty on me ? To take benefit in “Swablamban Scheme” we shouldn’t increase our contribution ?

IF I contribute 1000/- monthly and age at 60 we withdrawal 60% of our corpus than how much pension I will get ?

I know you are very friendly about this. So I hope you will certainly help me. Your revert via mail would be awaited.

Hi,

If you cant’ afford maintaining your NPS Account then you have to bear a penalty of Rs.100 per year of default & will need to pay the minimum amount to reactive the account.

If subscriber exits before 60 years of age, he/she has to invest 80% of accumulated saving to purchase a life annuity from IRDA regulate life insurer. The remaining 20% may be withdrawn as lump sum. On exit after age 60 years from the pension system, the subscriber would be required to invest at least 40% of pension wealth to purchase an annuity.

Sir,

i have.a.pran.card,can.i.open.second.pran.card…please.tell.me.for.my.future….urgent

No you cant opt.

I am group d stap.in.railway.can.i.do.tecnical.course.through.proper.chanel.

My age is 28 years and i am a private sector employee

Hi,

Looking at the NPS, I found that instead of investing in it one can go for a balanced fund from MF houses ( 60 – 80% equity 40-10% debt) and can get returns that are equivalent to NPS. The catch with NPS is that at maturity i.e. 60 yrs of age, we have to compulsory invest 40 % in annuity plans, which gives only around 6% returns. If one wants to withdraw before 60 yrs of age he is liable to invest 80% in annuity and gets only 20%. Then we get only 6% return on out 80% amount.

To avoid all this headache just invest in some balanced fund and get the freedom of withdrawing at anytime. Then put this in any post office scheme of bank FD and get returns 8% or higher.

Hi Hemant, can you please elobrate on the “annuitisation of pension wealth” in this para and also what exact it means.

“The exit from the Swavalamban Scheme would be on the same terms and conditions on which exit from Tier-I account of NPS is permitted, that is, exit at age 60 with 40% minimum annuitisation of pension wealth and exit before age 60 with 80% minimum annuitisation of pension wealth. However, the exit would be subject to the overriding condition that the amount of pension wealth to be annuitised should be sufficient to yield a minimum amount of Rs. 1,000 per month. If the annuitised pension wealth does not yield an amount of Rs. 1,000 per month, the percentage of pension wealth to be annuitised would be increased so that the pension amount becomes Rs. 1,000 per month, failing which the entire pension wealth would be subject to annuitisation. This minimum pension ceiling may be revised from time to time.”

I suggest to write something on this scheme so that, our forum memebers can help the ppl(Friends and relatives) who work in Unorganised sector. im doing the same

Thanks in Advance.

Hi Vijay,

New Pension Scheme is a defined contribution scheme that provides investment solutions for retirement needs.You will be offered two accounts -Tier I and Tier II.Its mandatory to have Tier I account,it will require minimum contribution of 6000 every year,single contribution being 500.Tier II account is an optional account which is likely to start after 6months which will allow partial withdrawal.

It works as you turn 60, you need to invest at least 40% of the corpus in an annuity plan offered by an insurance company.In that case you can withdraw 60% of the corpus tax free or remain invested.You can withdraw earlier too,but in that case you would need to annutise 80% of the corpus.

sir i have worked as government servent in Madhya pradesh from 19/011/2005 to 30/05/2010. but i have not get my contribution which had been deducted from my salary per month ( new pension scheme ) from my department. give me suggession how i receive my New Pension scheme contribution amount.

Hi Hemant;

I am a software engineer in a MNC.My date of birth is25_11-1983.Is it a good idea to open a NPS account?If so what is the suitable amount I can invest p.m to have descent amount as pension when I attain the age of 60?If Nps is not good enough what other avenues you suggest?Kindly oblige me.

With regards.

Which bank is having enquiry counter or web site to help me to open the account.Where we have to go or approach to open the account? Who will help us?

I’m a private sector employee-JVC with Delhi Govt. My date of birth is 10/06/1965.

How much I should contribute per quarter ,( How much for tier1 and How much for tier2) then how much I would get as pension when I’ll attain the age 60?

Will I get some lumpsum amount along with the pension?

Do I have an option to take a lumpsum amount or only pension or both?

What would be the lumpsum amount for tier 2?

Reply

I’m a private sector employee working as GM with JVC of Delhi Govt. My date of birth is 01/04/1965.

How much should I Contribute per quarter ,( How much for tier1 and How much for tier2) then how much I would get as pension when I’ll attain the age 60?

Will I get some lumpsum amount along with the pension?

Do I have an option to take a lumpsum amount or only pension or both?

What would be the lumpsum amount for tier 2?

What is mode of Payment to be made as premium & which Insurance co!

Also, I am professional as Engineer , If I continue my job after retirement, shall I get my pension!!

Is it home service!!

Since now 14 years are left for my retirement age i.e. 60

Reply

Hi Vikrant,

A minimum contribution of Rs 6000 would be compulsory per year. Minimum amount per contribution is Rs 500 and a minimum of 4 contribution in a year for each subscriber account is required.

The Tire 1 account is the basic NPS account that is non -withdrawable till retirement on in the case of death of the subscriber. In this type of account, the total corpus at the retirement age is split, whereby a minimum of 40 percent of the final corpus has to be compulsorily used to buy an annuity while the subscriber is free to withdraw the remaining 60 percent as a lum sum or in installments.

Withdraw-able Account: A tier 2 account is available to only who are existing subscriber of the tier 1 account. The unique selling point of the tier 2 account is that money contributed into this account can be freely withdrawn as and when the subscriber wishes except for minimum balance that needs to be maintained at the end of each financial year.

The payment mode is monthly and its limit is upto 6000 only in a year.

The scheme is offered though 23 point-of – Acceptance or POS. The major are SEBI and its 7 associated bank, ICICI bank ,IDBI Bank, OBC, Allahbad Bank CAMC etc. Not all the branches of these POS offer the information and services for NPS. You can check the website of the particular POS or call their toll free number to get information about of this availability of this scheme.

If subscriber exits before 60 years of age, he/she has to invest 80% of accumulated saving to purchase a life annuity from IRDA regulate life insurer. The remaining 20% may be withdrawn as lump sum. On exit after age 60 years from the pension system, the subscriber would be required to invest at least 40% of pension wealth to purchase an annuity. In case of Government employees, the annuity should provide for pension for the lifetime of the employee and his dependent parents and his spouse at the time of retirement. If subscriber does not exit the system at or before 70 years, account would be closed with the benefits transferred to subscriber in lump sum. If a subscriber dies, the nominee has the option to receive the entire pension wealth as a lump sum.

I am a central govt. employee. In present 2500/- per month deduct from my salary and 2500/- contribute from govt.(total 5000/-)per months deduct in my NPS.At present total 160000/- in my NPS account. I retired in April 2033. What is lump sum amount that i got in 2033, when i retired. What is minimum % return from NPS.

I want to know whether govt /employer contribution to NPS should be included in the gross salary for Income tax calculation .

Hi Amit,

yes contribution from Govt/employer to NPS will be included in your gross salary.

I want to know whether govt /employer contribution to NPS should be included in the gross salary for Income tax calculation .

reply from tinks

yes contribution from Govt/employer to NPS will be included in your gross salary.

According to me it will be injustice done on personnel working in government sector as in Public sctor undertaking or Private Sector it is EPF which is not considered in the gross salary for Income tax calculation.This NPS is forced on central government so this can be regared as double standards

My contribution to NPS is 49000 and government contribution is 49000 so total is 98000 the limit to have detuction is 1 lac so where i will be able to save the money

As NPS is EET this means money withdrawn after 60 yrs will taxed

So in this way i will be paying tax two times on the same money is this seem to be illlogical

So pls clarify my doubts

dear sir, i am a govt employee, contributing 2700/- +2700/-(from govt side)every month in nps tier-1 account. my age is now 34 years. how much pension shall i get after retirement? 6-7 type of annuities you have told explain me please.

Sir,

I joined in this Company (Oil PSU) in 1984. Goint to retire in March 2014. My Company offered me to join in NPS in Tire I . What will will be suitable for me ? What will be the return after retirement. My contribution say about 72000/- per annum. What will be the CAGR ? Which type of annuity I choose ? What will be tax implication ? In which class I should invest my corpus ? What lumpsum amount I will get ? Please reply me immediately.

Regards.

I want to know my account detail.whenever we check your website but there is no any proper link for account balance.please send me alink and instruction on my e mail id.

Where is my reply ?

I REQUEST TO KNOW AT WHAT AMOUNT OF CONTRIBUTION BY ME BEING DELHI GOVT JVC EMPLOYEE (NO CONTRIBUTION FROM DELHI GOVET) I CAN GET RS 25000/-PER MONTH AS PENSION AFTER 60 YEARS I.E. AFTER 14 YEARS.

How much time this Rs 25000/-per month will continue!!

Shall I get Life Cover for some amount and what will be max

I’m a private sector employee working as GM with JVC of Delhi Govt. My date of birth is 01/04/1965.

How much should I Contribute per quarter within 14 yaers ,( How much for tier1 and How much for tier2) so that I shall get min of Rs 25000/-per month as pension after attainment of 60 years of AGE. Will I get some lumpsum amount along with the pension?

Do I have an option to take a lumpsum amount or only pension or both?

What is mode of Payment to be made as premium & which Insurance co!

Also, I am professional as Engineer , If I continue my job after retirement, shall I get my pension!!

Is it home service!!

Hi sir,

i m a govt servant having benefits of old Pension scheme.

I want to know-

i. can i register my self in new pension scheme while continuing with old pension scheme;

ii. what will be the contribution of Govt. if i make a contribution of Rs. 1000/-pm;

iii. can my spouse a house wife can also be registered under NPS, what would be the contribution of govt if she makes a contribution of Rs. 1000/-

Hi,

I am having NPS, with pran number as well. I want to now that how will i get pin number so that i can see all details of my PF online.

Thanks,

Amol.

PIN is sent to your residence by post. If you have not received it yet you may call NPS call center.

I work in private college and am covered under EPF scheme. My DOB is 15/12/1967. The contribution to EPF is minimum by me as well as my employer (as per the maximum salary of 6500/- though salary is much more than this.). I calculated that with this I may get a pension of about 3808/- pm (max.) after my retirement at 60 yrs.

I want to open an NPS account also as individual citizen. Is it permitted as I am already covered by EPF scheme? If yes, then how much should I contribute towards Tier I & II to get a helthy pension assuming a realistic return.

Thanx in advance.

Hi! I am a central govt. employee. In NPS, at present I have Rs. 6.0L and say Rs. 5400 PM is deducted and 5400 PM is contributed by Govt. Now if I retire on Dec 31, 2030, what will be my final accumulation if there is say 6% increase in salary per year, average 9-10% return from NPS and what would be my pension per month if I deposit 100% in annuity considering 9% inflation rate and say 6% return from annuity. Can you provide some formula with change in salary contribution? Thanks and regards, Abhijit

Dear Sir,

I am a J&K state govt. employee and my basic salary is Rs.13580/- and gross salary is Rs.24000/-. If the department deducts my 10% salary and the same amount deposited by state govt. under NPS, how much amount and pension i will got after subscription of 18 years, please advice me.

Thanking You,

HARJINDER SINGH

my date of birth is 7-7-1971; i m emplyoed in Govt sector since jan 2005 contributing a varible sum i.e., 10% of my basic and DA, which was RS. 1127 in Feb, 2005 and now, in Nov,2011, it is Rs. 3,145, equal sum is contributed by the Govt.

what pension i will get at the age of 58 years.

Hi Sharad,

I am really sorry but it is a time consuming process to calculate these figures. My suggestion is you should go through old comments to get some idea.

Dear sir,

I’m a govt. employee, my DOB is 20/03/1983, Rs 3100 is dedecting from my salarly pm, how much will I get at the time of retirement in cash & what will be my monthly pension?

I work in private college and am covered under EPF scheme. My DOB is 15/12/1967. The contribution to EPF is minimum by me as well as my employer (as per the maximum salary of 6500/- though salary is much more than this.). I calculated that with this I may get a pension of about 3808/- pm (max.) after my retirement at 60 yrs.

I want to open an NPS account also as individual citizen. Is it permitted as I am already covered by EPF scheme? If yes, then how much should I contribute towards Tier I & II to get a helthy pension assuming a realistic return.

Thanx in advance.

Hi Alok,

Yes you can open NPS account – as such there is no restriction. Contribution Amount should depend on your goals – use calculator available on this post

https://www.retirewise.in/2011/04/franklin-templeton-family-solutions.html

Dear Sir,

I would liek to invest 10k everymonth in NPS. I am 33 years old.

Wat would be the amount that i would be getting after i am 60 years.

After i withdraw the 60% of the accumulated amount after , would the rest of 40% be paid as pension?

Hi Nitin,

Remaining 40% will be used to purchase annuity – which can give you some amount.

Dear Mr Hemant

(1). I am working in Central govt and my TIER-I contribution is 2200 and 2200 by govt. Now i have to fill income tax return, so should i deduct the total amount i.e 4400 from my salary or i can deduct only 2200 from salary for income tax rebate.

(2). What will be my Gross salary for income tax return that include my contribution and Govt contribution also under TIER-I.

(2). How i can subscribe for TIER-II. What will be the procedure for that.

Hi Sandeep,

According to earlier tax rules employee & employer contribution was part of 80 CCD – however, the aggregate deduction under Section 80C, 80CCC and 80CCD is fixed at Rs.1 lakh. Plus contribution made by the employer in New pension scheme should also be included in the Total income of NPS subscriber as far as calculation of income tax is concerned. But from this financial year employers contribution in NPS is totally exempted from tax so employee contribution can be used for sec 80 ccd & employer contribution is deducted from gross taxable income. This is something similar to home loan principal comes under section 80 C & home loan interest deducted from gross income.

You need an active Tier1 account to open a Tier 2 account. You can transfer money from Tier 2 to Tier 1 as well. Talk to your accounts department or check pfrda website.

mera pran ka a\c block ho gaya he.ab ise kholne ke liye mujhe kisase milna hoga.

Talk to your Point of Sales.

benefits of life annuity with return of purchase price and without return of purchase price and its meaning

Hi Siddiqui,

You purchase annuities with some lump-sum amount(purchase price) & there are almost 7-8 types of annuities (paying methods) – you have mentioned 2 of them

Return of purchase price – where annuities are given for certain period or till death & then lump-sum amount is returned back.

Without Return of Purchase Price – where annuities will be given till death & lump-sum(purchase price) will not be returned.

PS: I will try to write an article on this.

Hi sir i’m the govt employ. my cps deduction is rs 1456/- per month in my basic pay til two years & my D.O.B is 24-08-1987.howm纮

Hi Divakar,

I am not sure what you want to ask.

Hi Hemant,

I am a private sector employee. My age is 33 years. This month I have opened NPS account with Auto choice and SBI as PFM. I have started depositing 3000 per month to my NPS account.

Q1. after attaining 60 years of age will I receive money as lump sum amount or I will get monthly pension.

Q2. As per guidelines, after after attaining 60 years of age, 40% of our withdrawn amount should be used to purchase annuity? what does this mean?

Q2. How much pension amount per month will I get for next 15 years after 60 years of my age?

Thanks in advance

Tilak

refer to queiries of 64 and 65

that is nearly the same Q

Dear Hemanth,

Please inform me on tax status for Tier I and tier II account.

If its taxable would still be a worth investment.

Dear Hemant,

Is the follwoing statement true

”

Update: As per new notification by Finance ministry, under Direct Tax Code (DTC), NPS will also come under EEE and withdrawal will also be non-taxable from 2011. So New Pension Scheme could become the best long-term savings option.”

Sir,

I am state govt. employee. my contribution is Rs. 2323 and govt. side contribution is Rs 2323 in tier I and how much i will get pention after 60% lumpsum amount withdrawan.

The amount contribution in tier II is income tax free or not under section 80 C.

Hi ajit,

I will like to answer 2nd part of the question the contribution under Tier II is tax free upto 1 Lakh.

Sir,iam govt employee my date of birth is 15/07/1977. my salary deduction is under nps Rs1800 per month. My retire ment is in2035.how much amount gain after retire ment.?i shall invest 15years how much amount gain per month?

Sir,iam Raj. govt employee(teacher) my date of birth is 14/07/1977. my salary deduction is under nps Rs2095 per month. My retire ment is in2035.how much amount gain after retire ment.?i shall invest 15years how much amount gain per month?my joining date is 15.03.2005

REPLY

i want to know my a/c view? how to see my a/c view on computer to which process?

my big problem.in my pran from available bank a/c no is wrong? than what will i do please reply me.my self vikram kumar from patna,bihar.right now i m employee in bihar police.

Hi Vikashsuman

You can view your account in computer only if you have opened the account with the bank in which you have online account as well .

You need to tell this to PFRDA about the bank account & do provide with the correct bank account details.

Sir,iam Raj. govt employee(teacher) my date of birth is 14/07/1977. my salary deduction is under nps Rs2095 per month. My retire ment is in2037.how much amount gain after retire ment.?i shall invest 15years how much amount gain per month?my joining date is 15.03.2005

dear sir,

I have worked as an associate professor since2007 to2011 in Govt. Autonomous Astang Ayurvedic College Indore M.P. I did not get the reapplied pran kit till today.But the employer was deducting contribution every month. I have resigned from the above said institution on29Jan.2011. I have joined Rajasthan Ayurveda university Jodhpur on 31 .1.2011 and I got new pran no. in Rajasthan. Hence I want to withdraw the amount from N.P.S.scheme of M.P. Kindly, advice me the procedure for withdrawal .

sir

my pran kit has not received yet although registeration is made in month of july’11.

plz provide me the knowledge of its becoming so late.

Thanks

Hi Deepak,

You can contact in mumbai office or in mysore office.

Sir i am central govt employee and i have a pran no. But if i left my present department without proper channel or noc and join other govt deptt so nsdl issue me new pran no. Or not please give me the best way.thanku

I am also facing the Same problem..I am central Government employee form March 2010 and 10% is being contributed for NPS recently I received PRAN number but not received PRAN card…Now I am moving to other Central Government Department not in proper channel ie., without applying NOC .Now I resigned first job and Joined in another Department Now my query is 1) Can I withdraw the amount contributed to NPS in my first job??

2) Can I continue with the old PRAN number or I have to take new PRAN in the second department?? ( I havent applied through Properchannel)

3)Do i face any problem in future If I continue with the PRAN number received in first department??? Please reply me

I’ve same prblm & same queries.

my problem is same give me suggetion

I am a service holder in deptt of posts since january 2010. presently my deduction towards NPS is Rs 1700 per month. My date of birth is 01/03/1989 then how much I would get as pension at age 60? Will it gives me in lumpsum or monthly? I also want to open a tier2 account. Pls tel me about its benifits.

I am a govt employee contributing Rs. 1700 +1700(govt)per month to nps. My age is 24.How much pension i will get on retirement if i don’t withdraw anything on retirement. How much i will get if i withdraw 60% of my amount on retirement

Sir,

Whether State Govt employees can claim Sec 80 deduction in respect of contribution to NPS ?

Dear Sir,

My date of Birth is January 1963, after 16 years of service in the Army retired with pensinary benefits on 2000. Now I have joined the Cabinet Secreatiet on November 2011. Please suggest me whether I will go for New Defined Contribution Pension Scheme, or should take option for retirement benefits based on combined military and civil services in terms of Govt. of India decision No (1) below Rule 19 and Rule 54(13-a) of CCS(Pension) Rules 1972. Sir, suggestion for the above may also be sent to my E Mail address is

tapan0000000Sir,

I have joined in central govt service on 1st Nov 2007 with a pay scale of 5200-20200+2800. My retirement date is on 30 Nov 2014. As per NPS how much pension shall I get on retirement ?

I could not open my ID, on opening it wants 8 characters pass word but I have not the same what can I do?

sir I got my number by my e-mail & mobile with 110051806521 on 22/09/2011. but i have not received my PRAN KIT.I ask nodal office.but they reply not received PRAN KIT .what i do?

I am working in private trust hospital. My date of birth is 30th May 1967. I am investing more than 1 lacks per anum in LIC and PPF. I am paying tax more than 1 lacks per anum. Should i join NPS?

I am working in private compan. last six month back i have opened NPS Tier-I

account. I want to check my balacne status. ( i have PRAN number) How can i check through Internet.

sir.

I am contributing rs.3000 pm. and my date of birth is 04/05/1979. what amount i will get as pension at 57.

Hi Hemant

I have a question about the functioning and return from NPS

I have an NPS account since Dec 2010. I have invested over 2.5 lakhs in past 18 months in my account through SBI PFM. All I have seen so far in has been the fluctuations in NAV.

I am unable to understand how my money has grown in these months with SBI-PFM. If I were to invest the same amount in FD I would at least received some return, but through SBI-PFM I have not seen any returns so far.

NPS website say the following:

“The return under NPS is market driven. Hence, there is no guaranteed/defined amount of return. The returns generated through investments are accumulated and is not distributed as dividend or bonus.”

My concern here is that I have not seen any returns in any form since I opened this account. Market driven returns should still mean that there will be some returns (less or high) depending on how market performs.

Secondly as mentioned on the NPS website, “returns generated on investment are accumulated and not distributed”. I want to know how they are accumulated, how do I know how much is accumulated for me, and where can I check this.

I am not able to find any of these information and guidance so far on these issue on your or NPS website.

I was wondering if you or anyone could give me some information in this regard on how my money grows in NPS.

Thanks

Regards

My age is 36 yeras now. I need a pension of minimum 25ooo after my retirement. Can I get that through NPS. How much I need to invest per month to get 25000 per month starting from age 61?

Please let me know

I am working in MNC (It is a pvt ltd). Our employer is ready to contribute 10% of basic into NPS but some employees are not accepting to keep net monthly pay low(take home). Their version is they want to get more in-hand salary as their tax bracket is in 10%. Is it possible that company designs salary as flexible. Where some people can opt for NPS for one fiscal year and some people are not opting for it.

Example: Two employees X and Y have same CTC and get net monthly pay same. After NPS contribution employer is paying Mr X a salary (Previous salary – 10% of basic) and Mr Y is getting same salary (Previous salary).

Is it feasible in our organization?

my contribution in nps is 1795/- & i am 28 year old then what will be my accumulation at the age of retirement.

Hi Hemant,

Iwant to know what POP-SP (Point of Presence Service Provider) is . Actually my I-PIN is blocked and i want to obtain a new one. The form says that the “form for re-issue of I-Pin” is to be submitted at the POP-SP. Now, i cannot find out what this one thing is.

Please help.

Priya

Hi Priya,

It is the intermediary like ICICI bank or CAMS.

Thanks Hemant.

In my case, how do i get to know which is the one?i mean will my office be knowing it?

Hi Priya,

Ask your accounts or HR department.

Hi Hemant,

One more query….If working in an office,then do we have to proceed through DDO or can we approach POP-SP directly?

dear hemant

I am working at a private firm,salary 19,000pm.how much should i contribute to earn 50,000 pm as pension after 30 years?

my pan 2008108500100135 and pran 110030613891. Total balance of my account is not knowm till date.I am 54 yeards old worked as LDC nodal office till 2008. After that I have merged to Govt Service and started to NPS.what our position

my pan 2008108500100135 and pran 110030613891. Total balance of my account is not knowm till date. Have please?

hi i am working as a teacher,i won’t be getting any pension from the gov,so i want to invest for my pension.i would be comfortable saving Rs4000 per month,my birth date is 15aug1985,how much pension do you think i can get? i want the pension for life.

Hi I am state govt empolyee, and my DOB is 15/01/1979 and just receive PRAN application form to submit.

Please help me to decide the best scheme for me.

Dear Sir

My MOM is doing business, for pension plan , she wants to invest, her age is 44 right now, she is willing to invest 700 p.m. . Can anybody calculate and tell me what amount of return she will get permonth as a pension in her old age.

Ranjan Sarangi

Son

I’m a private sector employee. My date of birth is 10/06/1965.

Do you advise me joining NPS at this age as I will retire in 2024?

If yes then Ican contribute @max Rs 8000 per quarter up to 2024( Rs.5000 for tier1 and Rs. 3000 for tier2) then how much I would get as pension when I’ll attain the age 60 i.e. in year 2026 assuming CAGR of 10%?

Will I get some lumpsum amount along with the pension?

What would be the lumpsum amount for tier 2?

What minimum balance that needs to be maintained at the end of each financial year in tier 2 ?

i am employee of state government.date of joining may 2011.

i would like to contribute more amount in new pension scheme (in addtion to 10% of regular deduction).

is it possible?

in what way it is possible?

I am an employee of corporation bank now we are opting for NPS

i one query right know i m working wid govt bank what will happen to my contribution and banks contribution when i switch to some other private company which is having no pension plan only having pf then my pf will be transferred or not …..

Hi Rahul,

As you mentioned as your present arrangement is defined contribution (my contribution and banks contribution) – this can be shifted to new employer’s.

I m looking for the actual formulae with required input clearly defined.This will enable us calculate the probable amount one will get at 60 yrs of age.Regarding making a contribution towards NPS we understand we need not contribute anything.We work in a Maharatna Energy PSU and contribution towards NPS will be made by employer only.It will be a great help if u provide the right formulae.thanks

Sir, I am a State Government employee form august 2010 and 10% is being contributed for NPS recently I received PRAN number & PRAN card…Now I am moving to other Central Government Department not in proper channel ie., without applying NOC .At Present I resigned first job and Joined in another Department Now my query is 1) Can I withdraw the amount contributed to NPS in my first job??

2) Can I continue with the old PRAN number or I have to take new PRAN in the second department?? ( I havent applied through Properchannel)

3)Do i face any problem in future If I continue with the PRAN number received in first department??? Please reply me

PRASAD

REPLY

Hi, I am self employed female at the age of 36 years. I have few queries regarding NPS tier II account if possible, please clarify

Can we invest any amount or we have to provide them the fixed value like for month i deposit 3000 and in another month i deposit 10,000 is it viable in this scheme or not ?

What is annuitisation of pension wealth please elaborate in simple language. say if the total amount on maturity is 20 lacs then how much amount I can withdraw ?

If I wish to withdraw money after 5 years from tier II account in which i have submitted @5,000 p.m. then what would be approximate value of this amount after five years and what percentage i can withdraw

Regards

Hema

I AM WORKING IN VIZAG STEEL PLANT. AGE- 52 (Date of birth -11-02-1960) please suggest a good pension plan

I am teacher in KVS . My date of birth is 28 december 1958. After retirement at the age of 60 years how much amount will i get? And How much monthly pension will I get . My monthly subscription is Rs. 2663/ from my salary and is being paid from KVS. At present as on 31 jan 2012 amount is Rs 302298/- Thanks

I have changed my job and suppose i want to continue my contribution is it possible ?

suppose i have put up 2 years of service in other organisation can i restart it with giving whole amount at a time?

if suppose my lemployer directly subscribe to nps and my contribution goes t0 my account without any correction is it necessary to change the new employer details?

if i want to withdraw the whole amount can I ?

as my age is 40 years is it good for me to join or it is compulsory ?

I was in central governmetn job and I had resigned after that I joined the state govt. job but o contribution hav been deducted since last two is it possible for us to deposit the whole arrears at a time?

for operating old pran no which is blocked what I shal have to do?

the above commets may be replied please as it is very necessary for me

i am govt employee..i am now paying Rs 4000 /monthly(excluding employer contribution) as a NPS. my date of birth is 30/07/1984.what would be my lump sum and pension at exit of my service.please answer to my mail too.

Thanks

In pran kit my ddo code is wrong

My pran kit go to wrong ddo

what I do now

D/Sir, If a subscriber contribute Rs.100/-per month from age 35years ,then how many amount of pension per month he/she will get from age of 60yr.

And annual report of the account(pran) can he/she get!

i am primary school teacher. govt emloye. my basic is 7275. When i am appointed at that time my age is 22years.How much amount i will get at retairment and what are other facilities i will get

My mother has not received pension for the past 3 months. it gets credited in Bank of India on a monthly basis. Also Bank is not replying on the issue.

Please give a written complaint to the branch manager and retain a copy for your records. If you don’t get a reply within 15 working days, write to the senior manager [if the post exist] or write to the regional manager. You should get a reply within 15-20 working days.

In case you don’t get any response from regional manager, you can approach banking ombudsman with all the evidence of approaching bank manager and regional manager. Also, save and attach any responses from the bank on this matter.

It is slow process so be patient and persistent, you will find a solution.

D/Sir

i contribute Rs,889 p/m same as govt. contribute. My date of Birth is 15.11.1961.Contribute started from Nov’2009.How much i will get pension after withdrawal of 60%.

Dear Sir/Madam,

I want to know the Monthly pension policies available in India.

How much money to be spent for getting monthly pension around 20000per month. Is there any policies available.Please suggest me.

Rambabu.K

dear hemant; I joined s ervice in august 2004 im a gIovt employee since then then I come under npese sche me.n can I take so money as advanc

i am a govt. employee and have been deducting for NPS since june 2011 but yet to apply for PRAN. Will my past deductions added in my future deduction when i got a PRAN?

Sir,

I recieved my pran no. and ppn no. now pls guide me how I can check my bal in my account

Sir, I joined CENTRAL GOVT. Service on 15 Dec, 2004. Due to personal problem, I resigned on 16 Aug , 2007 from Central Govt. duties. During this tenure of service I contributed from my salary as contributory fund under New pension Scheme. Now, since I resigned from service, How can I get that fund ? What to do ? Is there any order exists for this ?

dear sir,

pls tell me my penssion money in my a/c. no is-

110081000000.pls give a details.thanks

hello sir,

i am central govt employee joined in sep 2006 under nps… my nps deduction was started from dec,2007.. i m in loss of management share..since from my joining.and through out year same deduction is made from our clearks… now what to do..

please guide me… regarding the period from sep2006-nov 2007,, what to do…

thanks and regards

samta

Hi..i am working in Canara Bank. Around 2363 amount is deducted towards NPS each month.My DOB is 17/04/1989. Can you tell me how much will i get as pension after 60.Also can you provide us the method of calculation.

hello sir,

i am a government employee and contribute Rs 2850 p/m to nps my d.o.b. Is 13/05/1990. What would be my lumpsum pension after my retirement

sir

i want to know that if i change the job.after that my balance amt rtnd or not.

definitely

1. sir,i am govt employee i want to know that if i leave my job after 10 years and that time my tier-1 amount (myself contribution+govt contribution) is approx 8 lacs,what will i get that time? please tell me in details (in precentage and amount also)

1. sir,i am govt employee i want to know that if i leave my job after 10 years and that time my tier-1 amount (myself contribution+govt contribution) is approx 8 lacs,what will i get that time? please tell me in details (in precentage and amount also) 2.in swamy handbook i read that after attaning of 60 yrs of age (retirement age) employee receives 60% of the wealth and 40%of the wealth will be given to IRDA regulated agency and it will provide pension. pls tell me the ratio of 60 and 40 is on both contribution or only govt contribution. i request you to tell me over my phone for my better understanding. my no is 09716585620. thank you

regarding to 2nd comment i will retire in 57 years of age (because i am member of paramilitary force).how it will applicable on me.

Sir,